Key Insights

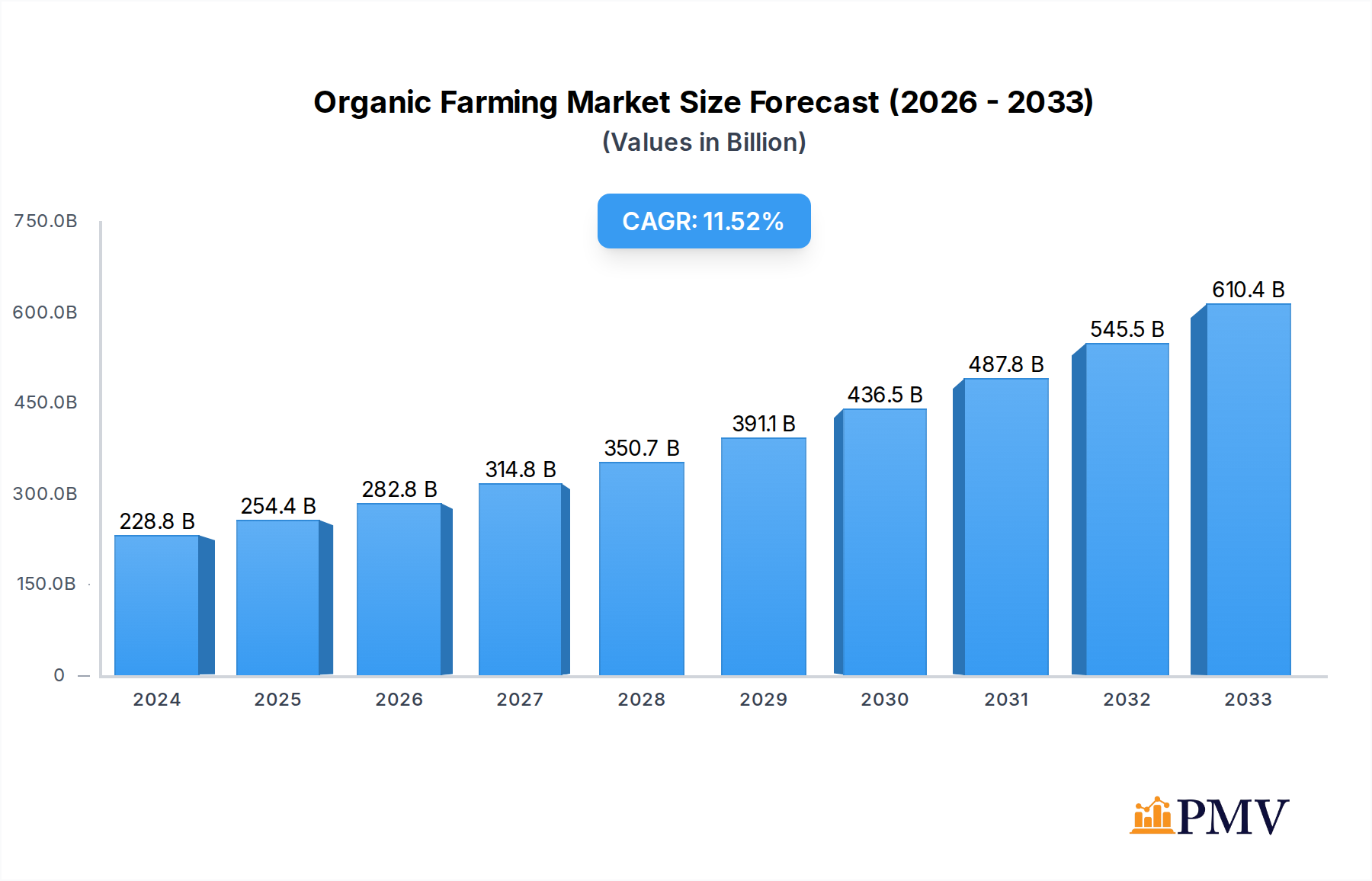

The global Organic Farming market is experiencing robust growth, projected to reach USD 228.84 billion in 2024, with an impressive Compound Annual Growth Rate (CAGR) of 11.18% extending through 2033. This expansion is primarily fueled by a growing consumer awareness regarding the health benefits of organic produce and a heightened concern for environmental sustainability. The increasing demand for pesticide-free and chemical-free food products is a significant driver, pushing both agricultural companies and organic farms to adopt and scale up their organic operations. Furthermore, government initiatives and subsidies supporting organic agriculture are playing a crucial role in fostering market development. The market is broadly segmented into Pure Organic Farming and Integrated Organic Farming, with both segments witnessing substantial uptake as stakeholders recognize the long-term viability and ecological advantages of these practices.

Organic Farming Market Size (In Billion)

The market's upward trajectory is further bolstered by emerging trends such as the adoption of advanced technologies like precision farming and IoT in organic cultivation, enhancing efficiency and yield. The increasing popularity of organic food products across a wider demographic, including millennials and Gen Z, is creating new avenues for market expansion. However, certain challenges, such as the higher initial investment costs for transitioning to organic farming and the need for specialized knowledge and resources, need to be addressed to sustain this growth momentum. Key players like Monsanto, KiuShi, Blue Yonder, Vero-Bio, and Bunge are actively investing in research and development, expanding their product portfolios, and forging strategic partnerships to capture market share. The regional landscape indicates strong performance across North America and Europe, with Asia Pacific emerging as a high-growth region due to rapid urbanization and increasing disposable incomes.

Organic Farming Company Market Share

Organic Farming Market Analysis: Comprehensive Insights & Future Outlook (2019–2033)

This comprehensive report delves into the global organic farming market, providing in-depth analysis of current trends, future projections, and key industry dynamics. Covering a study period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this report offers actionable intelligence for stakeholders in the sustainable agriculture, organic food production, and eco-friendly farming sectors. Discover critical market drivers, emerging innovations, and the competitive landscape shaped by industry leaders like Monsanto, KiuShi, Blue Yonder, Vero-Bio, Sikkim, Amalgamated Plantations, Bunge, DowDuPont, and Eden Foods. Understand the nuances of pure organic farming versus integrated organic farming and their respective market penetration.

Organic Farming Market Structure & Competitive Dynamics

The global organic farming market exhibits a moderately consolidated structure, characterized by the presence of both large multinational corporations and a significant number of niche players specializing in organic crop production and organic livestock farming. Innovation ecosystems are burgeoning, driven by advancements in precision agriculture for organic systems, biopesticides and biofertilizers, and organic seed technologies. Regulatory frameworks play a pivotal role, with stringent certification processes and government incentives shaping market entry and expansion. While direct product substitutes are limited due to the inherent nature of organic production, conventional farming practices represent a broad competitive alternative. End-user trends are increasingly favoring healthier food options, environmentally conscious consumption, and traceable supply chains, directly impacting demand for organic produce. Mergers and acquisitions (M&A) activities are expected to continue, with projected deal values in the billions of dollars as companies seek to expand their organic portfolios and market reach. For instance, anticipated M&A activities in the next forecast period are estimated to reach approximately \$XX billion. The market share of key players is dynamic, with some established agricultural giants actively investing in their organic divisions.

Organic Farming Industry Trends & Insights

The organic farming industry is poised for robust growth, projected to experience a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025–2033). This significant expansion is fueled by a confluence of factors, including escalating consumer awareness regarding the health benefits of organic foods and growing concerns about the environmental impact of conventional agricultural practices. The demand for pesticide-free produce and non-GMO ingredients is a primary market penetration driver, particularly in developed economies, with market penetration in these regions estimated to reach over XX% by 2030. Technological disruptions are also reshaping the sector. The adoption of smart farming technologies, including IoT-enabled sensors for soil health monitoring, AI-powered pest detection, and drone-based application of organic inputs, is enhancing efficiency and yields in organic farms. Blockchain technology is gaining traction for ensuring supply chain transparency and traceability, a crucial factor for consumer trust in organic products. Shifts in consumer preferences towards plant-based diets and locally sourced food further bolster the organic market. Furthermore, government initiatives, subsidies, and evolving agricultural policies supporting sustainable farming methods are creating a more conducive environment for organic producers. The competitive dynamics are characterized by increasing R&D investments by established players and the emergence of innovative startups focused on specialized organic solutions. The organic food market size is anticipated to reach \$XX billion by 2033.

Dominant Markets & Segments in Organic Farming

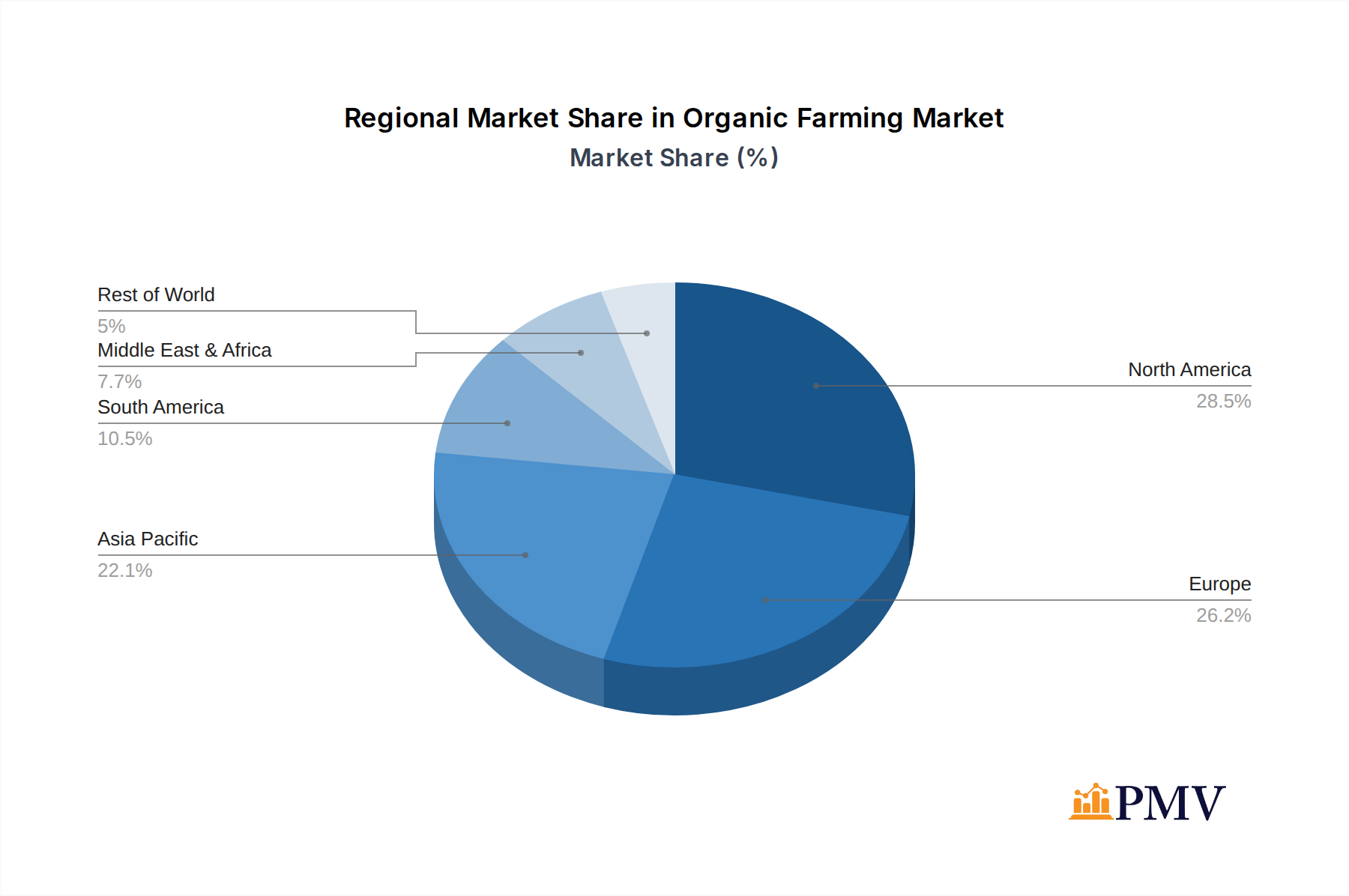

The organic farming market is witnessing significant dominance across various regions and segments. Europe currently stands as a leading region, driven by strong consumer demand for organic products and supportive government policies promoting eco-friendly agriculture. Within Europe, countries like Germany, France, and the UK are at the forefront of organic adoption. In terms of application, Agricultural Companies represent a significant segment, actively investing in and expanding their organic product lines, often through dedicated divisions or acquisitions. The Organic Farms segment itself is experiencing substantial growth as more farmers transition to organic practices.

Key drivers for this dominance include:

- Economic Policies: Extensive subsidies, tax incentives, and stringent regulations prohibiting synthetic inputs in many European nations.

- Infrastructure: Well-developed supply chains and distribution networks for organic produce, coupled with robust organic certification bodies.

- Consumer Awareness: High levels of public awareness regarding health and environmental benefits, leading to sustained demand.

- Technological Advancements: Increased adoption of organic-specific technologies that enhance productivity.

Analyzing the Type segmentation, Pure Organic Farming continues to hold a substantial market share due to its adherence to strict organic standards. However, Integrated Organic Farming is demonstrating rapid growth. This approach, which combines organic principles with other sustainable practices, offers flexibility and potentially higher yields, appealing to a broader range of agricultural operations. The market penetration of Integrated Organic Farming is expected to accelerate as farmers seek to balance organic integrity with economic viability. Growth projections for the Pure Organic Farming segment are estimated at XX% CAGR, while Integrated Organic Farming is projected to grow at a CAGR of XX%. The market size of the Organic Farms segment is projected to reach \$XX billion by 2033.

Organic Farming Product Innovations

Product innovation in organic farming is primarily focused on enhancing crop yields, improving pest and disease management, and increasing nutrient efficiency without the use of synthetic inputs. Developments include the creation of advanced biofertilizers derived from microbial communities, novel biopesticides offering targeted pest control with minimal environmental impact, and organic seed varieties with enhanced resilience to local conditions and diseases. These innovations aim to bridge the yield gap often associated with organic cultivation, making sustainable agriculture more economically competitive. Furthermore, the development of specialized organic soil amendments and composting technologies are improving soil health and fertility, crucial for long-term organic productivity. The competitive advantage lies in developing products that are not only effective but also cost-efficient and easily adaptable by organic farmers.

Report Segmentation & Scope

This report segments the global organic farming market by Application and Type.

Application:

- Agricultural Companies: This segment encompasses large-scale agricultural corporations, seed manufacturers, and input suppliers that are increasingly integrating organic solutions into their operations. Projections indicate a market size of \$XX billion by 2033, with a CAGR of XX%.

- Organic Farms: This segment represents dedicated organic farms of varying sizes, which are the primary adopters and beneficiaries of organic farming practices. This segment is expected to reach \$XX billion by 2033, with a CAGR of XX%.

Type:

- Pure Organic Farming: Characterized by strict adherence to established organic standards, this segment is projected to reach \$XX billion by 2033, with a CAGR of XX%.

- Integrated Organic Farming: This segment combines organic principles with other sustainable farming techniques, offering a more adaptable approach. It is expected to grow to \$XX billion by 2033, with a CAGR of XX%.

Key Drivers of Organic Farming Growth

Several key drivers are propelling the organic farming market forward. Technologically, the development and adoption of precision agriculture tools, biotechnology for organic inputs, and soil health monitoring systems are enhancing efficiency and sustainability. Economically, increasing consumer demand for healthy and sustainable food options, coupled with rising disposable incomes in emerging markets, is creating a substantial market pull. Government support in the form of subsidies for organic certification, favorable agricultural policies, and public procurement of organic products also plays a crucial role. For instance, widespread adoption of organic food labeling regulations across major economies has increased consumer confidence.

Challenges in the Organic Farming Sector

Despite the growth, the organic farming sector faces significant challenges. Regulatory hurdles, including complex and costly organic certification processes, can deter new entrants. Supply chain issues, such as limited availability of certified organic seeds and inputs and logistical complexities in distributing perishable organic produce, often lead to higher costs. Competitive pressures from conventional agriculture, which benefits from economies of scale and established infrastructure, also pose a challenge. Furthermore, the perceived higher cost of organic produce and the need for specialized knowledge among farmers can act as restraints. The global organic food market share is still growing, but these barriers need to be addressed for widespread adoption.

Leading Players in the Organic Farming Market

- Monsanto

- KiuShi

- Blue Yonder

- Vero-Bio

- Sikkim

- Amalgamated Plantations

- Bunge

- DowDuPont

- Eden Foods

Key Developments in Organic Farming Sector

- 2023 (Q4): Launch of a new bio-stimulant range by Vero-Bio, designed to enhance nutrient uptake in organic crops, contributing to higher yields.

- 2024 (Q1): Sikkim Organic Mission announces expanded outreach programs to train farmers in advanced organic pest management techniques, fostering wider adoption of pure organic farming.

- 2024 (Q2): Blue Yonder collaborates with agricultural cooperatives to implement AI-driven supply chain optimization for organic produce, reducing waste and improving delivery efficiency.

- 2024 (Q3): Amalgamated Plantations invests heavily in research for climate-resilient organic farming practices, focusing on drought-tolerant crop varieties.

- 2024 (Q4): DowDuPont introduces a novel organic herbicide with enhanced biodegradability, addressing environmental concerns in integrated organic farming.

Strategic Organic Farming Market Outlook

The strategic outlook for the organic farming market is highly promising, driven by increasing consumer demand for healthy, sustainable, and ethically produced food. Growth accelerators include further technological integration, such as advanced genomic analysis for organic crop breeding and AI-powered decision support systems for organic farmers. The expansion of organic markets into developing economies and the growing trend of corporate social responsibility leading to increased investment in eco-friendly agriculture present significant opportunities. Strategic opportunities lie in developing innovative organic food processing technologies, expanding organic product portfolios, and building robust, transparent organic supply chains that can cater to the evolving needs of consumers and regulatory bodies. The market is expected to witness continued M&A activity as companies seek to consolidate their position in this burgeoning sector.

Organic Farming Segmentation

-

1. Application

- 1.1. Agricultural Companies

- 1.2. Organic Farms

-

2. Type

- 2.1. Pure Organic Farming

- 2.2. Integrated Organic Farming

Organic Farming Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Organic Farming Regional Market Share

Geographic Coverage of Organic Farming

Organic Farming REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Organic Farming Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Agricultural Companies

- 5.1.2. Organic Farms

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Pure Organic Farming

- 5.2.2. Integrated Organic Farming

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Organic Farming Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Agricultural Companies

- 6.1.2. Organic Farms

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Pure Organic Farming

- 6.2.2. Integrated Organic Farming

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Organic Farming Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Agricultural Companies

- 7.1.2. Organic Farms

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Pure Organic Farming

- 7.2.2. Integrated Organic Farming

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Organic Farming Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Agricultural Companies

- 8.1.2. Organic Farms

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Pure Organic Farming

- 8.2.2. Integrated Organic Farming

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Organic Farming Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Agricultural Companies

- 9.1.2. Organic Farms

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Pure Organic Farming

- 9.2.2. Integrated Organic Farming

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Organic Farming Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Agricultural Companies

- 10.1.2. Organic Farms

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Pure Organic Farming

- 10.2.2. Integrated Organic Farming

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Monsanto

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KiuShi

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Blue Yonder

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Vero-Bio

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sikkim

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Amalgamated Plantations

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bunge

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 DowDuPont

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Eden Foods

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Monsanto

List of Figures

- Figure 1: Global Organic Farming Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Organic Farming Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Organic Farming Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Organic Farming Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Organic Farming Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Organic Farming Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Organic Farming Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Organic Farming Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Organic Farming Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Organic Farming Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Organic Farming Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Organic Farming Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Organic Farming Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Organic Farming Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Organic Farming Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Organic Farming Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Organic Farming Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Organic Farming Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Organic Farming Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Organic Farming Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Organic Farming Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Organic Farming Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Organic Farming Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Organic Farming Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Organic Farming Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Organic Farming Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Organic Farming Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Organic Farming Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Organic Farming Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Organic Farming Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Organic Farming Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Organic Farming Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Organic Farming Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Organic Farming Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Organic Farming Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Organic Farming Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Organic Farming Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Organic Farming Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Organic Farming Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Organic Farming Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Organic Farming?

The projected CAGR is approximately 11.18%.

2. Which companies are prominent players in the Organic Farming?

Key companies in the market include Monsanto, KiuShi, Blue Yonder, Vero-Bio, Sikkim, Amalgamated Plantations, Bunge, DowDuPont, Eden Foods.

3. What are the main segments of the Organic Farming?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Organic Farming," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Organic Farming report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Organic Farming?

To stay informed about further developments, trends, and reports in the Organic Farming, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence