Key Insights

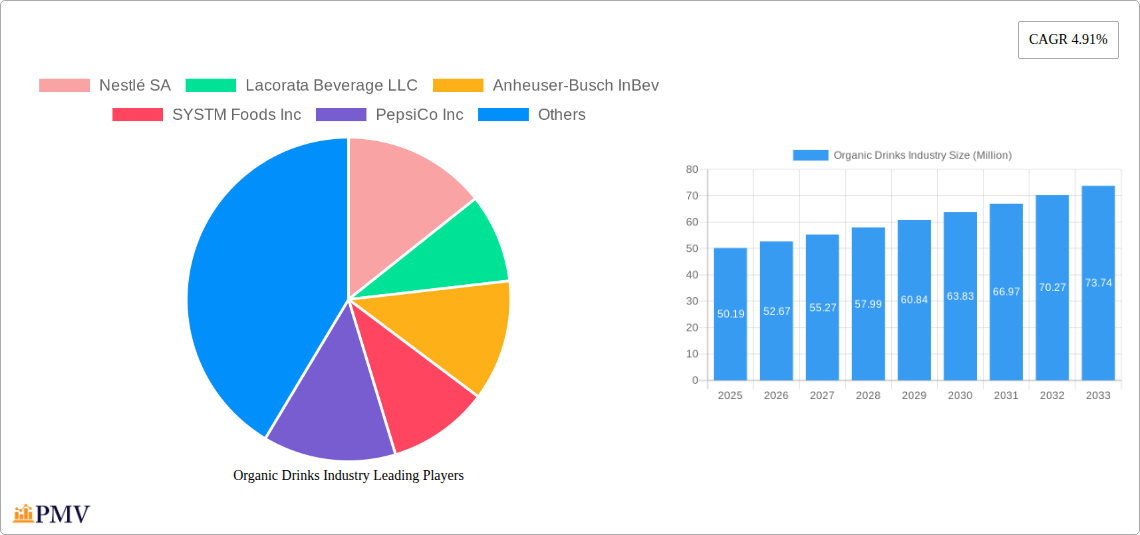

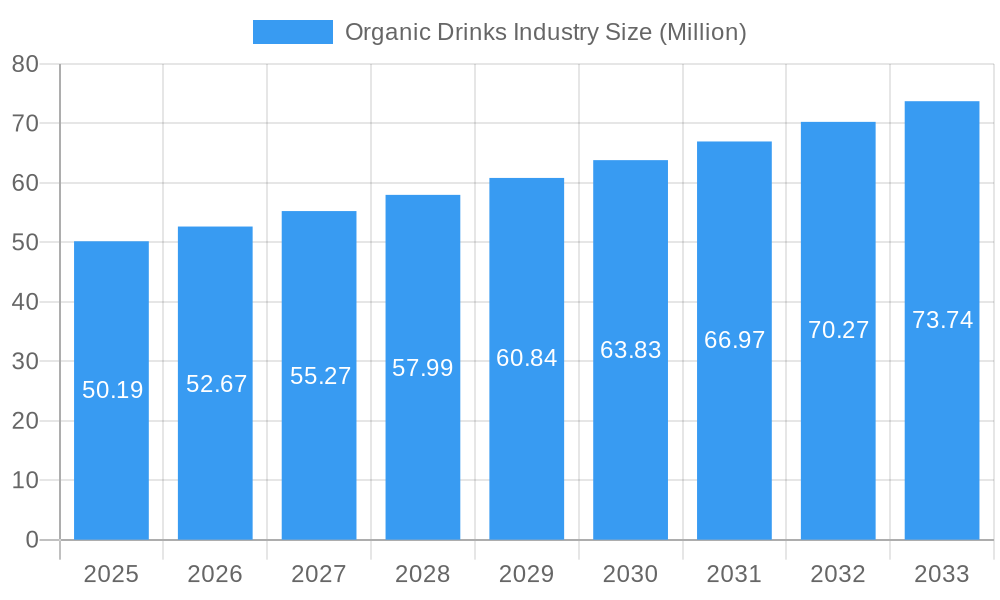

The global Organic Drinks Industry is poised for significant expansion, with a current market size estimated at $50.19 Million and projected to grow at a robust Compound Annual Growth Rate (CAGR) of 4.91% during the forecast period of 2025-2033. This growth trajectory is propelled by a confluence of increasingly health-conscious consumers seeking natural and sustainable beverage options, a rising awareness of the detrimental effects of synthetic additives and pesticides in conventional drinks, and a growing preference for ethically sourced and environmentally friendly products. The demand for organic beverages is further amplified by evolving consumer lifestyles and a desire for premium, higher-quality products that align with wellness goals. Key drivers include a widening distribution network, increasing availability through both traditional and online retail channels, and innovative product development catering to diverse taste preferences within both alcoholic and non-alcoholic segments.

Organic Drinks Industry Market Size (In Million)

The market is characterized by a dynamic segmentation across product types and distribution channels. Within the Alcoholic segment, wine, beer, and spirits are experiencing substantial growth as consumers seek organic alternatives. Similarly, the Non-alcoholic segment, encompassing fruit and vegetable juices, dairy alternatives, and coffee and tea, is witnessing increased demand driven by functional health benefits and clean-label appeal. Supermarkets/hypermarkets and online retailers are emerging as dominant distribution channels, offering broad accessibility and convenience. However, the industry faces certain restraints, including potentially higher production costs leading to premium pricing, limited availability of certified organic ingredients in some regions, and consumer skepticism regarding the true benefits or authenticity of "organic" claims. Despite these challenges, the overarching trend towards healthier living and sustainable consumption patterns ensures a promising future for the organic drinks market.

Organic Drinks Industry Company Market Share

Dive deep into the burgeoning organic drinks industry with this exhaustive market research report. Spanning the historical period of 2019–2024 and projecting through the forecast period of 2025–2033, with the base year and estimated year set at 2025, this report provides unparalleled insights into the global organic beverage market. Discover the market structure, intricate competitive dynamics, prevailing industry trends, dominant regions, innovative product developments, and strategic outlook. This analysis is crucial for stakeholders seeking to capitalize on the growing demand for healthy beverages, sustainable food products, and ethical consumption. With a projected market size expected to reach [Specific Predicted Market Value in Million] by 2033, understanding the forces shaping this sector is paramount.

Organic Drinks Industry Market Structure & Competitive Dynamics

The organic drinks industry exhibits a dynamic market structure characterized by increasing fragmentation and growing competition. While dominant players continue to command significant market share, innovation from emerging brands is reshaping the landscape. The innovation ecosystem thrives on the confluence of health-conscious consumer demands and advancements in sustainable sourcing and production. Regulatory frameworks play a crucial role, with evolving standards for organic certification and labeling influencing market entry and product development. The threat of product substitutes, though present, is mitigated by the premium perceived value and distinct benefits associated with organic offerings. End-user trends consistently favor products aligning with health, wellness, and environmental consciousness. Mergers and acquisitions (M&A) activities are a significant indicator of market consolidation and strategic expansion, with reported M&A deal values in the organic drinks market reaching [Specific Predicted M&A Deal Value in Million] during the study period. Key players like Nestlé SA, Anheuser-Busch InBev, and PepsiCo Inc. are actively participating in M&A to strengthen their portfolios.

- Market Concentration: Moderate to High, with a blend of large multinational corporations and specialized organic brands.

- Innovation Ecosystems: Driven by startups and established companies focusing on clean labels, functional ingredients, and novel flavor profiles.

- Regulatory Frameworks: Strict organic certification processes and evolving labeling laws necessitate compliance and transparency.

- Product Substitutes: While conventional beverages exist, the premium and health-focused positioning of organic drinks creates a distinct market segment.

- End-User Trends: Growing preference for plant-based alternatives, reduced sugar content, and ethically sourced ingredients.

- M&A Activities: Strategic acquisitions to expand product lines, geographic reach, and market share.

Organic Drinks Industry Industry Trends & Insights

The organic drinks industry is witnessing robust growth, driven by a confluence of powerful market growth drivers. The increasing global awareness of health and wellness is a primary catalyst, prompting consumers to seek natural beverages and chemical-free drinks free from synthetic pesticides and fertilizers. This translates into a significant surge in demand for organic juices, organic coffee, organic tea, and organic dairy alternatives. Technological disruptions, particularly in sustainable sourcing, processing, and packaging, are further enhancing the appeal and accessibility of organic beverages. For instance, advancements in fermentation technologies are enabling the development of novel organic functional beverages. Consumer preferences are increasingly leaning towards transparency, ethical sourcing, and environmentally friendly practices, which the organic segment inherently embodies. The competitive dynamics are intensifying, with established food and beverage giants investing heavily in their organic portfolios and new entrants disrupting the market with innovative offerings. The market penetration of organic drinks is steadily rising across developed and emerging economies, indicating a fundamental shift in consumer purchasing habits. The CAGR for the organic drinks market is projected to be [Specific Predicted CAGR]% during the forecast period, underscoring its significant expansion potential. The growing popularity of organic beer, organic wine, and organic spirits further diversifies the market, catering to evolving adult beverage preferences.

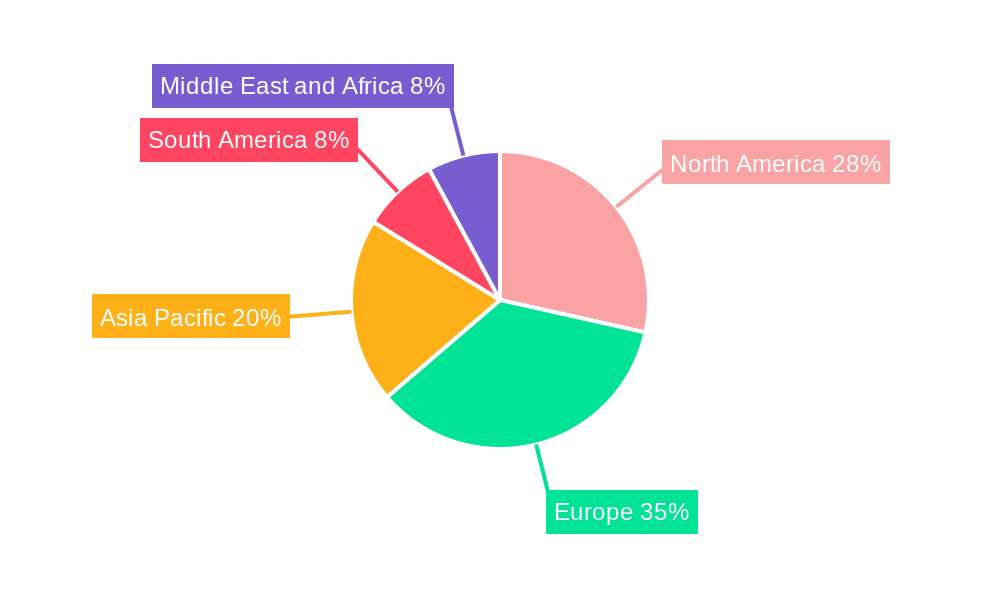

Dominant Markets & Segments in Organic Drinks Industry

The organic drinks industry is currently dominated by the Non-alcoholic segment, which is further propelled by the substantial growth of Fruit and Vegetable Juices and Dairy alternatives. The burgeoning health consciousness among consumers globally has made these categories frontrunners, with North America and Europe leading in terms of market share. The demand for organic dairy is particularly strong, fueled by the increasing adoption of plant-based diets and the availability of a wide array of organic milk, yogurt, and cheese alternatives.

In terms of distribution channels, Supermarkets/Hypermarkets continue to be the dominant channel, offering convenience and a wide selection to a broad consumer base. However, the rapid expansion of Online Retailers presents a significant growth opportunity, especially for niche and specialty organic brands. This channel offers enhanced reach and caters to the increasing preference for home delivery and curated shopping experiences.

The Alcoholic segment, while smaller in overall volume, is experiencing impressive growth, particularly within Organic Beer and Organic Wine. This trend is attributed to a growing consumer base that values premium quality, artisanal production, and a perceived healthier profile in alcoholic beverages.

- Leading Region: North America, driven by established organic markets and strong consumer demand for healthy products.

- Dominant Product Type Segment: Non-alcoholic beverages, with Fruit and Vegetable Juices and Dairy (including plant-based alternatives) leading the charge.

- Key Drivers for Fruit & Vegetable Juices: Growing awareness of vitamin and nutrient intake, demand for clean-label products, and innovative flavor combinations.

- Key Drivers for Organic Dairy: Rise of veganism and flexitarianism, concerns about conventional dairy farming practices, and wider product availability.

- Dominant Distribution Channel: Supermarkets/Hypermarkets, providing accessibility and a broad product assortment.

- Key Drivers for Supermarkets/Hypermarkets: One-stop shopping convenience, strategic placement of organic sections, and promotional activities.

- Emerging Distribution Channel: Online Retailers, offering convenience, wider selection, and direct-to-consumer models.

- Key Drivers for Online Retailers: Increasing e-commerce penetration, demand for niche products, and personalized shopping experiences.

- Growth Driver in Alcoholic Segment: Increasing consumer interest in craft beverages and a desire for "cleaner" alcohol options.

Organic Drinks Industry Product Innovations

Product innovation in the organic drinks industry is a key differentiator. Companies are focusing on developing novel formulations that cater to evolving consumer needs for health, taste, and convenience. Examples include the introduction of organic ready-to-drink (RTD) beverages, such as organic coffees and infused waters, which offer on-the-go solutions. Functional benefits, such as added probiotics, adaptogens, and vitamins, are increasingly being integrated into organic beverages, enhancing their appeal. Competitive advantages are being gained through unique flavor profiles, sustainable packaging solutions, and transparent ingredient sourcing. The trend towards plant-based organic dairy alternatives continues to drive innovation in this segment, with new bases and functional additives emerging. The organic alcoholic beverages sector is also seeing innovation with the development of organic hard seltzers and organic craft beers featuring unique botanical infusions.

Report Segmentation & Scope

This report segments the organic drinks industry comprehensively across key categories to provide granular insights. The Product Type segmentation encompasses both Alcoholic (Wine, Beer, Spirits, Other Alcoholic Beverages) and Non-alcoholic (Fruit and Vegetable Juices, Dairy, Coffee and Tea, Other Non-alcoholic Beverages) beverages. The Distribution Channel segmentation includes Supermarkets/Hypermarkets, Convenience Stores, Specialist Retailers, Online Retailers, and Other Distribution Channels. Each segment is analyzed for its market size, projected growth rates, and competitive landscape. For example, the Fruit and Vegetable Juices segment is anticipated to witness a market size of [Specific Predicted Segment Market Size in Million] by 2033, with a projected CAGR of [Specific Predicted Segment CAGR]%. The Online Retailers channel is expected to grow at a CAGR of [Specific Predicted Channel CAGR]%, indicating a significant shift in purchasing behavior.

- Product Type:

- Alcoholic: Wine, Beer, Spirits, Other Alcoholic Beverages.

- Non-alcoholic: Fruit and Vegetable Juices, Dairy, Coffee and Tea, Other Non-alcoholic Beverages.

- Distribution Channel:

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retailers

- Other Distribution Channels

Key Drivers of Organic Drinks Industry Growth

The organic drinks industry is propelled by several interconnected growth drivers. Growing consumer awareness regarding the health benefits of consuming organic products, free from synthetic pesticides and genetically modified organisms (GMOs), is a primary factor. This is further amplified by increasing concerns about environmental sustainability and ethical sourcing practices, which organic certifications often guarantee. Government initiatives promoting organic farming and labeling standards also play a crucial role in market expansion. Technological advancements in organic ingredient cultivation and processing techniques contribute to greater efficiency and product diversity. The rising disposable income in emerging economies also enables a larger segment of the population to opt for premium organic products.

- Consumer Health Consciousness: Demand for natural, chemical-free beverages.

- Environmental Sustainability Concerns: Preference for products with a lower ecological footprint.

- Government Support and Regulations: Favorable policies promoting organic agriculture and fair trade.

- Technological Advancements: Improved organic farming methods and processing technologies.

- Economic Growth and Disposable Income: Increased purchasing power for premium organic goods.

Challenges in the Organic Drinks Industry Sector

Despite its robust growth trajectory, the organic drinks industry faces several challenges. The higher cost of organic ingredients and production processes often leads to premium pricing, which can be a barrier for price-sensitive consumers. Stringent organic certification processes can be time-consuming and costly for smaller producers, impacting market entry. Supply chain complexities, including the sourcing of certified organic raw materials and ensuring their integrity throughout the distribution network, can pose significant hurdles. Intense competition from both established conventional beverage brands and other organic players requires continuous innovation and effective marketing strategies. Furthermore, maintaining consistent quality and availability of organic ingredients can be subject to seasonal variations and climate-related impacts.

- Premium Pricing: Higher production costs translate to higher retail prices.

- Certification Costs and Complexity: Bureaucratic hurdles for obtaining and maintaining organic certifications.

- Supply Chain Vulnerabilities: Ensuring the availability and integrity of organic raw materials.

- Intense Market Competition: Differentiating organic brands in a crowded marketplace.

- Ingredient Availability and Seasonality: Reliance on natural agricultural cycles.

Leading Players in the Organic Drinks Industry Market

- Nestlé SA

- Lacorata Beverage LLC

- Anheuser-Busch InBev

- SYSTM Foods Inc

- PepsiCo Inc

- Whitewave Foods Company

- James White Drinks

- Bison Organic Beer

- Danone SA

- Organic Valley

- PS Organic LLC

- Drake's Organic Spirits LLC

Key Developments in Organic Drinks Industry Sector

- June 2022: Systm Foods acquired Chameleon Organic Coffee from Nestlé USA, enhancing its ready-to-drink organic coffee portfolio.

- March 2022: Graasi Barley Water launched a new line of ready-to-drink (RTD) organic waters, expanding options in the non-alcoholic functional beverage space.

- March 2022: Anheuser-Busch InBev introduced a new line of hard seltzers infused with coconut water under its Michelob Ultra brand, catering to the growing RTD alcoholic beverage market.

Strategic Organic Drinks Industry Market Outlook

The strategic outlook for the organic drinks industry remains exceptionally positive. Growth accelerators include the continuous expansion of health and wellness trends, coupled with an increasing consumer demand for ethically produced and environmentally sustainable products. The rising preference for plant-based diets will continue to fuel the demand for organic dairy alternatives and other plant-derived beverages. Strategic opportunities lie in the development of functional organic beverages that offer specific health benefits, such as enhanced immunity or digestive health. The expansion into emerging markets, where organic consumption is gaining traction, presents a significant untapped potential. Furthermore, innovations in sustainable packaging and efficient supply chain management will be critical for long-term success. The organic drinks market is poised for sustained growth, driven by conscious consumerism and a commitment to healthier living.

Organic Drinks Industry Segmentation

-

1. Product Type

-

1.1. Alcoholic

- 1.1.1. Wine

- 1.1.2. Beer

- 1.1.3. Spirits

- 1.1.4. Other Alcoholic Beverages

-

1.2. Non-alcoholic

- 1.2.1. Fruit and Vegetable Juices

- 1.2.2. Dairy

- 1.2.3. Coffee and Tea

- 1.2.4. Other Non-alcoholic Beverages

-

1.1. Alcoholic

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Convenience Stores

- 2.3. Specialist Retailers

- 2.4. Online Retailers

- 2.5. Other Distribution Channels

Organic Drinks Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. France

- 2.5. Italy

- 2.6. Russia

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Organic Drinks Industry Regional Market Share

Geographic Coverage of Organic Drinks Industry

Organic Drinks Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.91% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Alcoholic

- 5.1.1.1. Wine

- 5.1.1.2. Beer

- 5.1.1.3. Spirits

- 5.1.1.4. Other Alcoholic Beverages

- 5.1.2. Non-alcoholic

- 5.1.2.1. Fruit and Vegetable Juices

- 5.1.2.2. Dairy

- 5.1.2.3. Coffee and Tea

- 5.1.2.4. Other Non-alcoholic Beverages

- 5.1.1. Alcoholic

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Convenience Stores

- 5.2.3. Specialist Retailers

- 5.2.4. Online Retailers

- 5.2.5. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Organic Drinks Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Alcoholic

- 6.1.1.1. Wine

- 6.1.1.2. Beer

- 6.1.1.3. Spirits

- 6.1.1.4. Other Alcoholic Beverages

- 6.1.2. Non-alcoholic

- 6.1.2.1. Fruit and Vegetable Juices

- 6.1.2.2. Dairy

- 6.1.2.3. Coffee and Tea

- 6.1.2.4. Other Non-alcoholic Beverages

- 6.1.1. Alcoholic

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Convenience Stores

- 6.2.3. Specialist Retailers

- 6.2.4. Online Retailers

- 6.2.5. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Organic Drinks Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Alcoholic

- 7.1.1.1. Wine

- 7.1.1.2. Beer

- 7.1.1.3. Spirits

- 7.1.1.4. Other Alcoholic Beverages

- 7.1.2. Non-alcoholic

- 7.1.2.1. Fruit and Vegetable Juices

- 7.1.2.2. Dairy

- 7.1.2.3. Coffee and Tea

- 7.1.2.4. Other Non-alcoholic Beverages

- 7.1.1. Alcoholic

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Convenience Stores

- 7.2.3. Specialist Retailers

- 7.2.4. Online Retailers

- 7.2.5. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Organic Drinks Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Alcoholic

- 8.1.1.1. Wine

- 8.1.1.2. Beer

- 8.1.1.3. Spirits

- 8.1.1.4. Other Alcoholic Beverages

- 8.1.2. Non-alcoholic

- 8.1.2.1. Fruit and Vegetable Juices

- 8.1.2.2. Dairy

- 8.1.2.3. Coffee and Tea

- 8.1.2.4. Other Non-alcoholic Beverages

- 8.1.1. Alcoholic

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Convenience Stores

- 8.2.3. Specialist Retailers

- 8.2.4. Online Retailers

- 8.2.5. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Organic Drinks Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Alcoholic

- 9.1.1.1. Wine

- 9.1.1.2. Beer

- 9.1.1.3. Spirits

- 9.1.1.4. Other Alcoholic Beverages

- 9.1.2. Non-alcoholic

- 9.1.2.1. Fruit and Vegetable Juices

- 9.1.2.2. Dairy

- 9.1.2.3. Coffee and Tea

- 9.1.2.4. Other Non-alcoholic Beverages

- 9.1.1. Alcoholic

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Convenience Stores

- 9.2.3. Specialist Retailers

- 9.2.4. Online Retailers

- 9.2.5. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Organic Drinks Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Alcoholic

- 10.1.1.1. Wine

- 10.1.1.2. Beer

- 10.1.1.3. Spirits

- 10.1.1.4. Other Alcoholic Beverages

- 10.1.2. Non-alcoholic

- 10.1.2.1. Fruit and Vegetable Juices

- 10.1.2.2. Dairy

- 10.1.2.3. Coffee and Tea

- 10.1.2.4. Other Non-alcoholic Beverages

- 10.1.1. Alcoholic

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Convenience Stores

- 10.2.3. Specialist Retailers

- 10.2.4. Online Retailers

- 10.2.5. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Organic Drinks Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Alcoholic

- 11.1.1.1. Wine

- 11.1.1.2. Beer

- 11.1.1.3. Spirits

- 11.1.1.4. Other Alcoholic Beverages

- 11.1.2. Non-alcoholic

- 11.1.2.1. Fruit and Vegetable Juices

- 11.1.2.2. Dairy

- 11.1.2.3. Coffee and Tea

- 11.1.2.4. Other Non-alcoholic Beverages

- 11.1.1. Alcoholic

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Convenience Stores

- 11.2.3. Specialist Retailers

- 11.2.4. Online Retailers

- 11.2.5. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nestlé SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lacorata Beverage LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Anheuser-Busch InBev

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SYSTM Foods Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 PepsiCo Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Whitewave Foods Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 James White Drinks

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bison Organic Beer

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Danone SA

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Organic Valley*List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 PS Organic LLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Drake's Organic Spirits LLC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Nestlé SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Organic Drinks Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Organic Drinks Industry Volume Breakdown (liter , %) by Region 2025 & 2033

- Figure 3: North America Organic Drinks Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Organic Drinks Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 5: North America Organic Drinks Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Organic Drinks Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Organic Drinks Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 8: North America Organic Drinks Industry Volume (liter ), by Distribution Channel 2025 & 2033

- Figure 9: North America Organic Drinks Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Organic Drinks Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 11: North America Organic Drinks Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Organic Drinks Industry Volume (liter ), by Country 2025 & 2033

- Figure 13: North America Organic Drinks Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Organic Drinks Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Organic Drinks Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 16: Europe Organic Drinks Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 17: Europe Organic Drinks Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Organic Drinks Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 19: Europe Organic Drinks Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 20: Europe Organic Drinks Industry Volume (liter ), by Distribution Channel 2025 & 2033

- Figure 21: Europe Organic Drinks Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 22: Europe Organic Drinks Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 23: Europe Organic Drinks Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Organic Drinks Industry Volume (liter ), by Country 2025 & 2033

- Figure 25: Europe Organic Drinks Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Organic Drinks Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Organic Drinks Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 28: Asia Pacific Organic Drinks Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 29: Asia Pacific Organic Drinks Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 30: Asia Pacific Organic Drinks Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 31: Asia Pacific Organic Drinks Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 32: Asia Pacific Organic Drinks Industry Volume (liter ), by Distribution Channel 2025 & 2033

- Figure 33: Asia Pacific Organic Drinks Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 34: Asia Pacific Organic Drinks Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 35: Asia Pacific Organic Drinks Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Organic Drinks Industry Volume (liter ), by Country 2025 & 2033

- Figure 37: Asia Pacific Organic Drinks Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Organic Drinks Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Organic Drinks Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 40: South America Organic Drinks Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 41: South America Organic Drinks Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 42: South America Organic Drinks Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 43: South America Organic Drinks Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 44: South America Organic Drinks Industry Volume (liter ), by Distribution Channel 2025 & 2033

- Figure 45: South America Organic Drinks Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: South America Organic Drinks Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: South America Organic Drinks Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: South America Organic Drinks Industry Volume (liter ), by Country 2025 & 2033

- Figure 49: South America Organic Drinks Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Organic Drinks Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Organic Drinks Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Organic Drinks Industry Volume (liter ), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Organic Drinks Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Organic Drinks Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Organic Drinks Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 56: Middle East and Africa Organic Drinks Industry Volume (liter ), by Distribution Channel 2025 & 2033

- Figure 57: Middle East and Africa Organic Drinks Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Middle East and Africa Organic Drinks Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Middle East and Africa Organic Drinks Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Organic Drinks Industry Volume (liter ), by Country 2025 & 2033

- Figure 61: Middle East and Africa Organic Drinks Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Organic Drinks Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 3: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Organic Drinks Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Organic Drinks Industry Volume liter Forecast, by Region 2020 & 2033

- Table 7: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 9: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 11: Global Organic Drinks Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Organic Drinks Industry Volume liter Forecast, by Country 2020 & 2033

- Table 13: United States Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 15: Canada Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 17: Mexico Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 19: Rest of North America Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of North America Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 21: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 22: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 23: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 24: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 25: Global Organic Drinks Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Organic Drinks Industry Volume liter Forecast, by Country 2020 & 2033

- Table 27: Spain Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Spain Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 29: United Kingdom Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: United Kingdom Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 31: Germany Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 33: France Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: France Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 35: Italy Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Italy Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 37: Russia Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Russia Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 39: Rest of Europe Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Europe Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 41: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 42: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 43: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 44: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 45: Global Organic Drinks Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 46: Global Organic Drinks Industry Volume liter Forecast, by Country 2020 & 2033

- Table 47: China Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: China Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 49: Japan Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Japan Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 51: India Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: India Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 53: Australia Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Australia Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 55: Rest of Asia Pacific Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Rest of Asia Pacific Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 57: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 58: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 59: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 60: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 61: Global Organic Drinks Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 62: Global Organic Drinks Industry Volume liter Forecast, by Country 2020 & 2033

- Table 63: Brazil Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: Brazil Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 65: Argentina Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Argentina Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 67: Rest of South America Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 68: Rest of South America Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 69: Global Organic Drinks Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 70: Global Organic Drinks Industry Volume liter Forecast, by Product Type 2020 & 2033

- Table 71: Global Organic Drinks Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 72: Global Organic Drinks Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 73: Global Organic Drinks Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 74: Global Organic Drinks Industry Volume liter Forecast, by Country 2020 & 2033

- Table 75: South Africa Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: South Africa Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 77: United Arab Emirates Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: United Arab Emirates Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 79: Rest of Middle East and Africa Organic Drinks Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: Rest of Middle East and Africa Organic Drinks Industry Volume (liter ) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Organic Drinks Industry?

The projected CAGR is approximately 4.91%.

2. Which companies are prominent players in the Organic Drinks Industry?

Key companies in the market include Nestlé SA, Lacorata Beverage LLC, Anheuser-Busch InBev, SYSTM Foods Inc, PepsiCo Inc, Whitewave Foods Company, James White Drinks, Bison Organic Beer, Danone SA, Organic Valley*List Not Exhaustive, PS Organic LLC, Drake's Organic Spirits LLC.

3. What are the main segments of the Organic Drinks Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.19 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Health-conscious consumers are increasingly demanding organic beverages.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

In June 2022, the food and beverage brand, Systm Foods acquired Chameleon Organic Coffee from Nestlé USA. Chameleon Organic Coffee's product portfolio includes single-serve ready-to-drink products as well as multi-serve concentrates.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Organic Drinks Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Organic Drinks Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Organic Drinks Industry?

To stay informed about further developments, trends, and reports in the Organic Drinks Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence