Key Insights

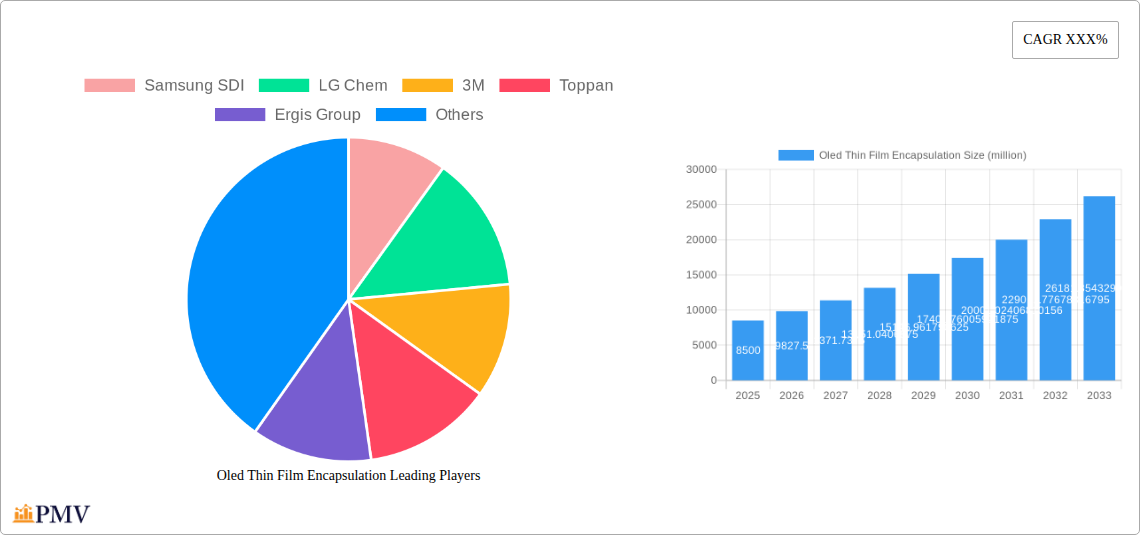

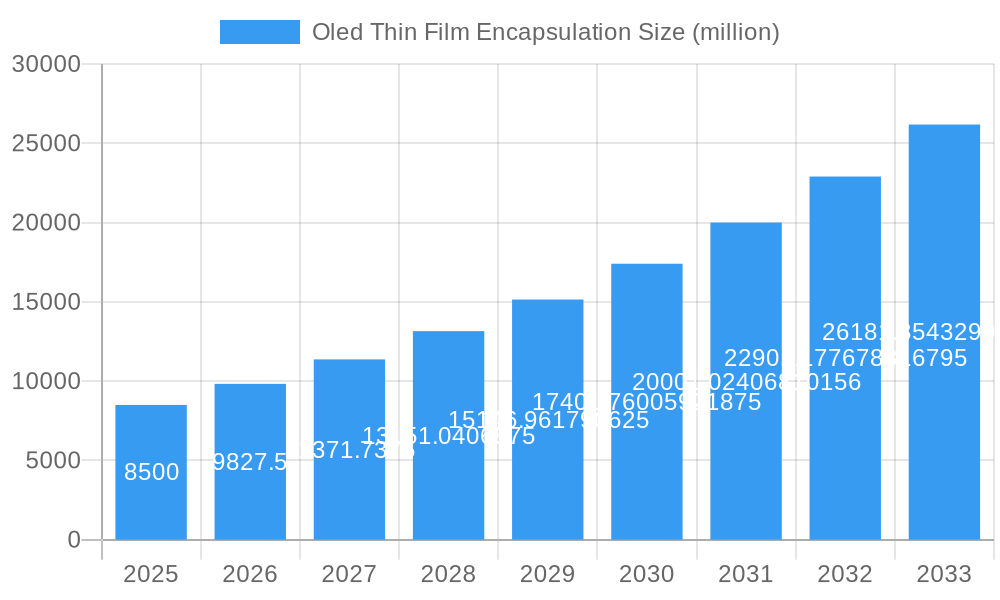

The OLED thin film encapsulation market is poised for substantial growth, projected to reach an estimated market size of USD 8,500 million in 2025. This expansion is driven by the increasing adoption of OLED technology across a spectrum of applications, most notably in consumer electronics such as smartphones, smartwatches, and high-definition televisions, where vibrant displays and energy efficiency are paramount. The automotive sector is also emerging as a significant growth area, with OLEDs being integrated into dashboards, infotainment systems, and even exterior lighting for their superior visual quality and design flexibility. Furthermore, advancements in healthcare, particularly in wearable medical devices and diagnostic displays, alongside niche applications in aerospace, are contributing to the market's upward trajectory. The compound annual growth rate (CAGR) is estimated to be around 15.5% from 2025 to 2033, indicating a robust and sustained expansion over the forecast period. This growth is fueled by continuous innovation in display technology and the demand for more immersive and durable visual experiences.

Oled Thin Film Encapsulation Market Size (In Billion)

The market's dynamism is further shaped by prevailing trends such as the development of flexible and transparent OLED displays, which unlock new design possibilities for devices and create opportunities in augmented reality (AR) and virtual reality (VR) applications. Innovations in inorganic layer deposition and organic layer deposition techniques are crucial in achieving superior barrier properties, essential for protecting sensitive OLED materials from moisture and oxygen, thereby enhancing device longevity and performance. Key players like Samsung SDI, LG Chem, 3M, and Universal Display Corporation are heavily investing in research and development to overcome challenges such as the cost-effectiveness of encapsulation processes and the scalability of manufacturing. Despite these advancements, challenges such as the complex manufacturing process and the need for specialized equipment can act as restraints. However, the overwhelming demand for advanced display solutions across diverse industries, coupled with ongoing technological refinements, strongly indicates a positive outlook for the OLED thin film encapsulation market.

Oled Thin Film Encapsulation Company Market Share

This in-depth market research report provides a definitive analysis of the global OLED thin film encapsulation market, meticulously examining its structure, competitive landscape, emerging trends, and future trajectory. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this report offers critical insights for stakeholders seeking to navigate this dynamic and rapidly evolving sector. We delve into the intricacies of inorganic and organic layer deposition technologies, analyze market penetration across key applications like consumer electronics, automotive, industrial, healthcare, and aerospace, and identify the dominant forces shaping this multi-billion dollar industry.

OLED Thin Film Encapsulation Market Structure & Competitive Dynamics

The OLED thin film encapsulation market exhibits a moderately concentrated structure, characterized by the presence of a few dominant players alongside a robust ecosystem of specialized technology providers and material suppliers. Innovation clusters are evident, particularly in regions with advanced display manufacturing capabilities, fostering a competitive environment driven by technological advancements and intellectual property. Regulatory frameworks, while still evolving, are increasingly focused on environmental sustainability and material safety, influencing manufacturing processes and product development. Product substitutes, primarily traditional encapsulation methods or alternative display technologies, pose a competitive threat but are gradually being outpaced by the superior performance and flexibility offered by advanced thin-film encapsulation. End-user trends are strongly dictated by the demand for thinner, lighter, and more flexible displays across consumer electronics and emerging automotive and industrial applications. Mergers and acquisitions (M&A) activities are a significant aspect of market dynamics, with strategic consolidations aimed at acquiring new technologies, expanding market reach, and achieving economies of scale. Notable M&A deal values in the historical period are estimated to be in the hundreds of millions of dollars, with projected future deals potentially reaching billions. The market share distribution reflects this concentration, with leading companies holding substantial portions, driven by their patented technologies and extensive production capacities.

OLED Thin Film Encapsulation Industry Trends & Insights

The OLED thin film encapsulation industry is experiencing robust growth, driven by an escalating demand for high-performance displays across a multitude of applications. Market growth drivers are primarily fueled by the insatiable appetite for thinner, more flexible, and energy-efficient electronic devices. The increasing adoption of OLED technology in smartphones, wearables, televisions, and automotive displays represents a significant catalyst. Technological disruptions, such as advancements in deposition techniques like Atomic Layer Deposition (ALD) and Plasma-Enhanced Chemical Vapor Deposition (PECVD), are enabling the creation of more effective barrier layers, crucial for OLED device longevity and performance. These innovations are addressing the inherent vulnerability of OLED materials to moisture and oxygen, thereby expanding their applicability in harsher environments. Consumer preferences are increasingly leaning towards devices with immersive visual experiences, foldable capabilities, and enhanced durability, all of which are facilitated by sophisticated thin-film encapsulation. Competitive dynamics are intense, with companies investing heavily in research and development to achieve superior encapsulation efficiency, reduced manufacturing costs, and novel functionalities. The market penetration of OLED displays, while already significant in premium consumer electronics, is projected to surge in automotive dashboards, smart home devices, and even healthcare wearables, indicating substantial untapped potential. The Compound Annual Growth Rate (CAGR) for the OLED thin film encapsulation market is estimated to be in the double digits, exceeding 15% over the forecast period, reflecting its strong growth trajectory.

Dominant Markets & Segments in OLED Thin Film Encapsulation

The Consumer Electronics segment stands as the dominant market within the OLED thin film encapsulation landscape, driven by the widespread adoption of smartphones, tablets, wearables, and high-end televisions. Key drivers for its dominance include:

- Economic Policies: Favorable trade policies and government incentives supporting the electronics manufacturing sector in key Asian economies have bolstered production and innovation.

- Infrastructure: Well-developed manufacturing infrastructure, including advanced cleanroom facilities and skilled labor, supports high-volume production of OLED displays and their encapsulation.

- Consumer Demand: A consistently high and growing consumer demand for premium visual experiences, portable devices, and smart home integration fuels the need for advanced OLED displays.

- Technological Advancements: Continuous innovation in OLED materials and encapsulation technologies further enhances display performance, leading to greater consumer appeal.

The Automotive segment is rapidly emerging as a significant growth area.

- Key Drivers: Increasing integration of digital displays in vehicle interiors for infotainment, navigation, and driver assistance systems is a primary driver. The demand for flexible and durable displays that can withstand automotive environmental conditions (temperature fluctuations, vibrations) further propels the need for advanced thin-film encapsulation. Government mandates and consumer expectations for advanced in-car technology are accelerating adoption.

Within the Type segmentation, Inorganic Layer Deposition techniques, such as ALD and sputtered oxides, are currently leading due to their superior barrier properties against moisture and oxygen.

- Key Drivers: The inherent effectiveness of inorganic materials in preventing ingress of environmental contaminants is paramount for OLED device reliability and longevity, particularly in demanding applications.

- Technological Maturity: These deposition methods have a higher degree of maturity and are well-established in high-volume manufacturing processes.

However, Organic Layer Deposition is gaining traction with advancements in polymeric materials and multi-layer structures, offering advantages in flexibility and cost-effectiveness.

- Key Drivers: The drive towards ultra-thin and flexible displays, a hallmark of modern consumer electronics and emerging applications, favors the development and application of organic encapsulation materials. Innovations in barrier performance of organic polymers are closing the gap with inorganic counterparts.

The Industrial segment is also showing promising growth, driven by the need for robust and reliable displays in manufacturing equipment, automation systems, and specialized instrumentation. Healthcare is a nascent but high-potential segment, with applications in medical wearables, diagnostic devices, and flexible displays for patient monitoring. Aerospace and Others represent niche but growing markets, where the demand for lightweight, durable, and high-performance displays is critical.

OLED Thin Film Encapsulation Product Innovations

Recent product innovations in OLED thin film encapsulation focus on enhancing barrier properties, improving flexibility, and reducing manufacturing costs. Companies are developing multi-layer structures combining inorganic and organic materials to achieve an optimal balance of performance and cost-effectiveness. Advancements in ALD and PECVD techniques enable more uniform and defect-free deposition, crucial for extending OLED device lifespan. The integration of self-healing polymers and moisture-scavenging materials within encapsulation layers is also a key trend, further boosting reliability. These innovations provide a competitive advantage by enabling the development of next-generation OLED displays with superior performance, enhanced durability, and novel form factors, such as foldable and rollable screens, catering to the evolving demands of consumer electronics, automotive, and industrial sectors.

Report Segmentation & Scope

This report segments the OLED thin film encapsulation market by Application and Type.

- Application Segmentation: The market is analyzed across Consumer Electronics, Automotive, Industrial, Healthcare, Aerospace, and Others. Consumer Electronics is projected to hold the largest market share, estimated at over 70% in 2025, with a projected market size of approximately $7,000 million. The Automotive segment is expected to witness the fastest growth, with a CAGR of over 20%, reaching an estimated market size of $2,500 million by 2033.

- Type Segmentation: The market is further divided into Inorganic Layer Deposition and Organic Layer Deposition. Inorganic Layer Deposition currently dominates, with an estimated market share of over 60% in 2025, valued at around $6,000 million. Organic Layer Deposition is anticipated to grow at a significant CAGR of approximately 18%, driven by advancements in flexible display technologies, and is projected to capture a substantial portion of the market by 2033.

Key Drivers of OLED Thin Film Encapsulation Growth

The growth of the OLED thin film encapsulation market is primarily propelled by several key factors. Firstly, the burgeoning demand for advanced display technologies in consumer electronics, including smartphones, smartwatches, and OLED TVs, remains a significant driver. Secondly, the increasing integration of OLED displays in the automotive sector for infotainment systems, digital cockpits, and advanced driver-assistance systems is creating substantial new opportunities. Thirdly, ongoing technological advancements in encapsulation materials and deposition techniques, such as Atomic Layer Deposition (ALD) and Plasma-Enhanced Chemical Vapor Deposition (PECVD), are enhancing the performance, durability, and flexibility of OLED devices, making them suitable for a wider range of applications. Finally, favorable economic conditions and supportive government policies in key manufacturing hubs are further stimulating market expansion.

Challenges in the OLED Thin Film Encapsulation Sector

Despite its robust growth, the OLED thin film encapsulation sector faces several challenges. High manufacturing costs associated with complex deposition processes and specialized materials can be a significant barrier to widespread adoption in cost-sensitive applications. The stringent requirement for ultra-low moisture and oxygen permeability necessitates advanced and often expensive equipment and processes, limiting the number of manufacturers capable of producing high-quality encapsulation. Supply chain vulnerabilities, particularly for critical raw materials and specialized equipment, can lead to production disruptions and price volatility. Furthermore, the rapid pace of technological evolution requires continuous R&D investment, posing a challenge for smaller players to keep pace with innovation leaders. Competitive pressures from alternative display technologies also necessitate constant innovation to maintain market relevance.

Leading Players in the OLED Thin Film Encapsulation Market

- Samsung SDI

- LG Chem

- 3M

- Toppan

- Ergis Group

- Veeco Instruments

- Universal Display Corporation

- Applied Materials

- Kateeva

- Toray Industries

- tesa

- Ajinomoto Fine-Techno Co

- Coat-X

- Borealis AG

- AMS Technologies

- Angstrom Engineering

- Beneq

- ENCAPSULIX

- Holst Center

- SNU PRECISION

- SAES Getters

- MBRAUN

Key Developments in OLED Thin Film Encapsulation Sector

- 2023: Kateeva launched its next-generation PVD system for advanced thin-film encapsulation, targeting improved deposition uniformity and throughput.

- 2023: Universal Display Corporation announced advancements in its phosphorescent OLED (PHOLED) technology, requiring more robust encapsulation solutions.

- 2022: Toppan developed a new multi-layer barrier film for flexible OLED displays, offering enhanced moisture resistance.

- 2022: LG Chem showcased advancements in flexible organic encapsulation materials, enabling thinner and more pliable displays.

- 2021: Veeco Instruments introduced a new ALD system tailored for high-volume OLED encapsulation, focusing on cost reduction and process control.

- 2021: Samsung SDI highlighted its ongoing investment in R&D for next-generation OLED encapsulation technologies.

- 2020: 3M introduced new flexible barrier films with improved optical clarity and barrier properties.

- 2019: Ergis Group expanded its production capacity for advanced barrier films used in OLED encapsulation.

Strategic OLED Thin Film Encapsulation Market Outlook

The strategic outlook for the OLED thin film encapsulation market remains highly positive, characterized by sustained growth and increasing opportunities. The market is poised to benefit from the continued expansion of OLED technology into new applications, particularly in the automotive and industrial sectors. Innovations in flexible and transparent encapsulation solutions will unlock novel product designs and functionalities. Strategic collaborations between material suppliers, equipment manufacturers, and display producers will be crucial for driving technological advancements and market penetration. Companies that can offer cost-effective, high-performance, and highly reliable encapsulation solutions are expected to capture significant market share. The focus on sustainability and environmental compliance will also shape future product development and manufacturing strategies, presenting an opportunity for companies offering eco-friendly encapsulation materials and processes.

Oled Thin Film Encapsulation Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Automotive

- 1.3. Industrial

- 1.4. Healthcare

- 1.5. Aerospace

- 1.6. Others

-

2. Type

- 2.1. Inorganic Layer Deposition

- 2.2. Organic Layer Deposition

Oled Thin Film Encapsulation Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

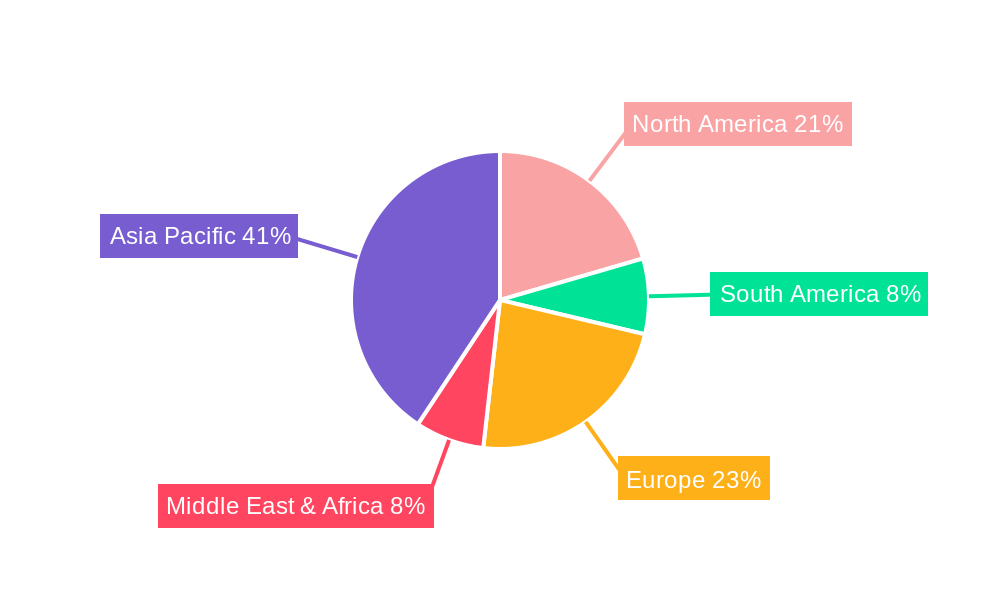

Oled Thin Film Encapsulation Regional Market Share

Geographic Coverage of Oled Thin Film Encapsulation

Oled Thin Film Encapsulation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Automotive

- 5.1.3. Industrial

- 5.1.4. Healthcare

- 5.1.5. Aerospace

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Inorganic Layer Deposition

- 5.2.2. Organic Layer Deposition

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Automotive

- 6.1.3. Industrial

- 6.1.4. Healthcare

- 6.1.5. Aerospace

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Inorganic Layer Deposition

- 6.2.2. Organic Layer Deposition

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Automotive

- 7.1.3. Industrial

- 7.1.4. Healthcare

- 7.1.5. Aerospace

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Inorganic Layer Deposition

- 7.2.2. Organic Layer Deposition

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Automotive

- 8.1.3. Industrial

- 8.1.4. Healthcare

- 8.1.5. Aerospace

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Inorganic Layer Deposition

- 8.2.2. Organic Layer Deposition

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Automotive

- 9.1.3. Industrial

- 9.1.4. Healthcare

- 9.1.5. Aerospace

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Inorganic Layer Deposition

- 9.2.2. Organic Layer Deposition

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Automotive

- 10.1.3. Industrial

- 10.1.4. Healthcare

- 10.1.5. Aerospace

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Inorganic Layer Deposition

- 10.2.2. Organic Layer Deposition

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Oled Thin Film Encapsulation Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Consumer Electronics

- 11.1.2. Automotive

- 11.1.3. Industrial

- 11.1.4. Healthcare

- 11.1.5. Aerospace

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Inorganic Layer Deposition

- 11.2.2. Organic Layer Deposition

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Samsung SDI

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 LG Chem

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 3M

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Toppan

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ergis Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Veeco Instruments

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Universal Display Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Applied Materials

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Kateeva

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Toray Industries

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 tesa

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ajinomoto Fine-Techno Co

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Coat-X

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Borealis AG

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 AMS Technologies

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Angstrom Engineering

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Beneq

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 ENCAPSULIX

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Holst Center

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 SNU PRECISION

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 SAES Getters

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 MBRAUN

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Samsung SDI

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Oled Thin Film Encapsulation Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Oled Thin Film Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Oled Thin Film Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Oled Thin Film Encapsulation Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Oled Thin Film Encapsulation Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Oled Thin Film Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Oled Thin Film Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Oled Thin Film Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Oled Thin Film Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Oled Thin Film Encapsulation Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Oled Thin Film Encapsulation Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Oled Thin Film Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Oled Thin Film Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Oled Thin Film Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Oled Thin Film Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Oled Thin Film Encapsulation Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Oled Thin Film Encapsulation Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Oled Thin Film Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Oled Thin Film Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Oled Thin Film Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Oled Thin Film Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Oled Thin Film Encapsulation Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Oled Thin Film Encapsulation Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Oled Thin Film Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Oled Thin Film Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Oled Thin Film Encapsulation Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Oled Thin Film Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Oled Thin Film Encapsulation Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Oled Thin Film Encapsulation Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Oled Thin Film Encapsulation Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Oled Thin Film Encapsulation Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Oled Thin Film Encapsulation Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Oled Thin Film Encapsulation Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oled Thin Film Encapsulation?

The projected CAGR is approximately 20.6%.

2. Which companies are prominent players in the Oled Thin Film Encapsulation?

Key companies in the market include Samsung SDI, LG Chem, 3M, Toppan, Ergis Group, Veeco Instruments, Universal Display Corporation, Applied Materials, Kateeva, Toray Industries, tesa, Ajinomoto Fine-Techno Co, Coat-X, Borealis AG, AMS Technologies, Angstrom Engineering, Beneq, ENCAPSULIX, Holst Center, SNU PRECISION, SAES Getters, MBRAUN.

3. What are the main segments of the Oled Thin Film Encapsulation?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oled Thin Film Encapsulation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oled Thin Film Encapsulation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oled Thin Film Encapsulation?

To stay informed about further developments, trends, and reports in the Oled Thin Film Encapsulation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence