Key Insights

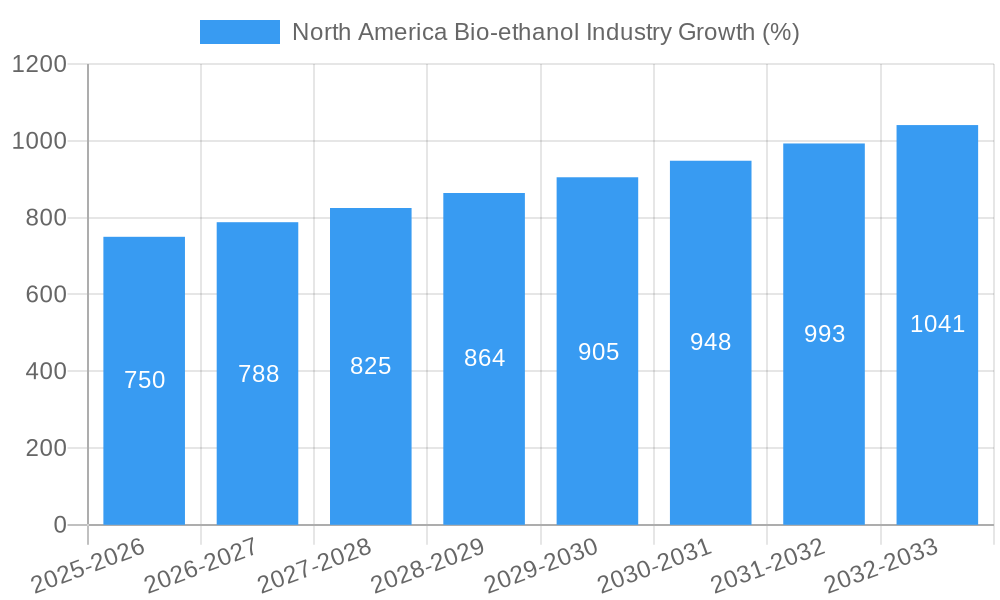

The North American bioethanol industry, currently valued at approximately $XX million (assuming a reasonable value based on global market size and North America's share), is projected to experience robust growth with a Compound Annual Growth Rate (CAGR) exceeding 5% from 2025 to 2033. This expansion is driven by several key factors. Firstly, increasing government mandates and incentives promoting the use of renewable fuels are significantly bolstering demand. Secondly, the growing focus on reducing greenhouse gas emissions and achieving carbon neutrality is fueling the adoption of bioethanol as a sustainable alternative to fossil fuels, particularly within the automotive and transportation sector. Furthermore, the diversification of feedstocks beyond corn, encompassing sugarcane, wheat, and other sources, enhances the industry's resilience and reduces reliance on a single agricultural commodity. The food and beverage industry's increasing use of bioethanol as a solvent and ingredient also contributes to market growth.

However, the industry faces challenges. Fluctuations in agricultural commodity prices and the availability of feedstocks can impact production costs and profitability. Competition from other renewable energy sources, such as biodiesel and electricity from renewable sources, also presents a restraint. Despite these hurdles, the long-term outlook remains positive, driven by sustained governmental support, technological advancements improving bioethanol production efficiency, and the increasing consumer awareness of environmental sustainability. Market segmentation, focusing on feedstock type (sugarcane, corn, wheat, others) and application (automotive, food & beverage, pharmaceutical, cosmetics, others), offers opportunities for strategic growth and specialization within the industry. Key players like ADM, Green Plains, and others are well-positioned to capitalize on this expanding market, through continuous innovation and strategic partnerships.

North America Bio-ethanol Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the North America bio-ethanol industry, covering the period from 2019 to 2033. It offers valuable insights into market structure, competitive dynamics, key trends, and future growth prospects, equipping stakeholders with actionable intelligence for strategic decision-making. The report leverages extensive data analysis and incorporates expert perspectives to deliver a clear and concise overview of this dynamic sector. With a focus on key segments, leading players, and emerging technologies, this report is an essential resource for industry professionals, investors, and researchers seeking to understand and capitalize on opportunities within the North American bio-ethanol market.

North America Bio-ethanol Industry Market Structure & Competitive Dynamics

The North American bio-ethanol market exhibits a moderately concentrated structure, with several large players holding significant market share. Key players such as ADM, ADM, Green Plains Inc, and Valero exert considerable influence, shaping market dynamics through their production capacity and distribution networks. The industry's competitive landscape is further characterized by ongoing mergers and acquisitions (M&A) activity, as companies seek to expand their market reach and consolidate their positions. For instance, ADM's 2021 sale of its Peoria ethanol plant for xx Million illustrates strategic portfolio adjustments within the sector. The total value of M&A deals in the industry during the study period (2019-2024) reached approximately xx Million. The regulatory framework, particularly concerning renewable fuel mandates and environmental regulations, significantly influences the industry's competitive dynamics. Furthermore, the market is witnessing increasing innovation in feedstock utilization and production technologies, creating new opportunities for both established players and emerging entrants. Product substitution, mainly from other biofuels and traditional gasoline, presents a notable challenge to the industry's growth. End-user trends towards sustainable transportation fuels are, however, driving demand for bio-ethanol.

- Market Concentration: Moderately Concentrated

- M&A Activity: Significant, with total deal value of approximately xx Million (2019-2024).

- Regulatory Framework: Strong influence, driving both opportunity and challenge.

- Product Substitutes: Significant pressure from other biofuels and gasoline.

- End-user Trends: Growing demand driven by sustainable transportation goals.

North America Bio-ethanol Industry Industry Trends & Insights

The North American bio-ethanol industry is experiencing robust growth, driven by increasing demand for renewable fuels, government support for biofuel mandates, and advancements in bio-ethanol production technologies. The Compound Annual Growth Rate (CAGR) for the period 2019-2024 is estimated at xx%, with a projected CAGR of xx% for the forecast period (2025-2033). Market penetration of bio-ethanol in the transportation sector is steadily increasing, fuelled by stringent emission regulations and consumer preferences for environmentally friendly fuels. Technological disruptions, such as the development of cellulosic ethanol and advanced biofuel production technologies, are further accelerating the sector's growth. However, challenges remain, including feedstock price volatility and competition from other renewable energy sources. The industry's competitive landscape is evolving rapidly, with continuous innovation and strategic partnerships shaping the future market dynamics. The increasing focus on sustainability and the circular economy is creating new opportunities for bio-ethanol producers to integrate into broader value chains.

Dominant Markets & Segments in North America Bio-ethanol Industry

Corn is the dominant feedstock in North America's bio-ethanol production, accounting for approximately xx% of the total feedstock volume in 2025. The Automotive and Transportation segment is the primary application for bio-ethanol, with a market share of around xx% in the base year.

Dominant Feedstock:

- Corn: Dominant due to large-scale production, established infrastructure, and government support. Key drivers include favorable agricultural policies and readily available land for cultivation.

- Sugarcane: Significant presence in certain regions, but smaller overall contribution compared to corn.

Dominant Application:

- Automotive and Transportation: Dominates due to government mandates (Renewable Fuel Standard) and consumer preference for greener alternatives. Key drivers include stricter emission standards and increasing environmental awareness.

- Other Applications (Food and Beverage, Pharmaceuticals etc.): Smaller but growing market segment.

North America Bio-ethanol Industry Product Innovations

Recent advancements in bio-ethanol production include the development of cellulosic ethanol, which utilizes non-food biomass, thereby minimizing competition with food production. The successful commissioning of VERBIO AG's cellulosic RNG plant in 2022 signifies a step change in the industry's technological capabilities, offering a path towards more sustainable and efficient biofuel production. Furthermore, research into advanced biofuel technologies is accelerating, potentially leading to improved yields and reduced costs. These innovations are shaping a more competitive and sustainable bio-ethanol market, enhancing its market fit and providing companies with key competitive advantages.

Report Segmentation & Scope

This report segments the North American bio-ethanol market by feedstock type (Corn, Sugarcane, Wheat, Other Feedstocks) and application (Automotive and Transportation, Food and Beverage, Pharmaceutical, Cosmetics and Personal Care, Other Applications). Each segment's growth trajectory, market size (in Million gallons), and competitive dynamics are analyzed. The report covers the historical period (2019-2024), the base year (2025), and provides projections for the forecast period (2025-2033). The analysis includes detailed insights into market drivers, challenges, and key industry players in each segment.

Key Drivers of North America Bio-ethanol Industry Growth

The growth of the North American bio-ethanol industry is propelled by several key factors: Stringent government regulations promoting renewable fuels (like the Renewable Fuel Standard), increasing consumer demand for sustainable transportation alternatives, advancements in production technologies (cellulosic ethanol), and supportive government policies incentivizing biofuel production. Furthermore, the ongoing shift towards a circular economy and the exploration of new feedstocks contribute to the industry's expansion.

Challenges in the North America Bio-ethanol Industry Sector

The North American bio-ethanol industry faces several challenges, including feedstock price volatility impacting production costs, competition from other renewable fuels and traditional gasoline, and stringent environmental regulations requiring continuous improvement in production processes. Supply chain disruptions and fluctuations in global energy markets also pose significant challenges to the industry. Furthermore, achieving wider adoption in applications beyond transportation remains an ongoing challenge.

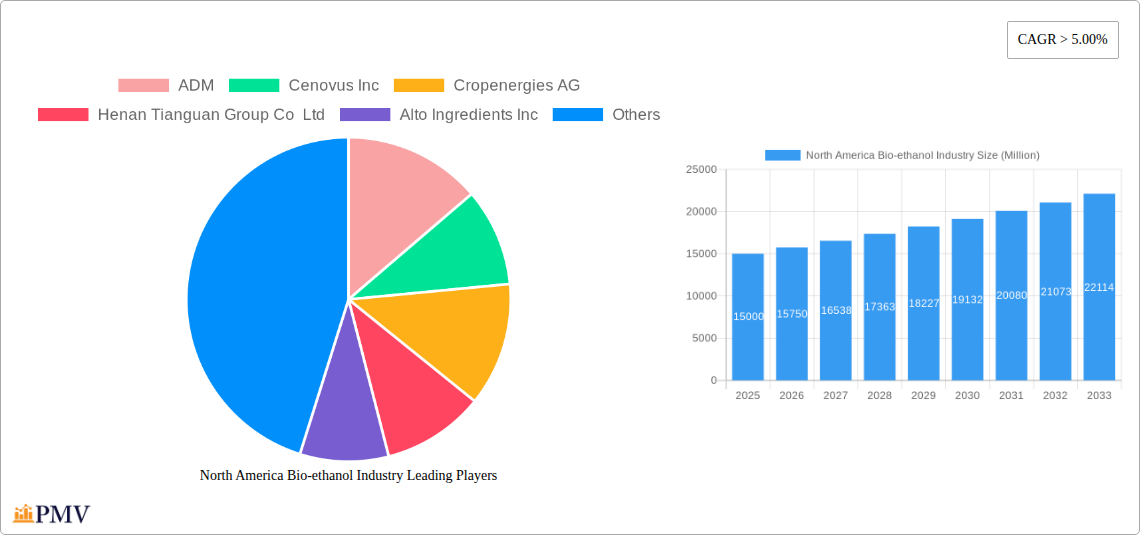

Leading Players in the North America Bio-ethanol Industry Market

- ADM

- Cenovus Inc

- Cropenergies AG

- Henan Tianguan Group Co Ltd

- Alto Ingredients Inc

- Green Plains Inc

- Suncor Energy Inc

- Valero

- Ethanol Technologies

- Verbio Vereinigte Bioenergie AG

- Abengoa

- Granbio Investimentos SA

- Sekab

- Blue Bio Fuels Inc

- Lantmannen

- Cristalco

- Poet LLC

- Jilin Fuel Ethanol Co Ltd

- Raizen

- KWST

Key Developments in North America Bio-ethanol Industry Sector

- October 2021: ADM signed an agreement to sell its Peoria, Illinois ethanol plant to BioUrja Group.

- May 2022: VERBIO AG launched its first cellulosic RNG plant in the US, achieving full-scale production of 7 Million EGE of RNG annually. In 2023, the facility began producing 60 Million gallons of corn-based ethanol annually.

Strategic North America Bio-ethanol Industry Market Outlook

The North American bio-ethanol industry is poised for continued growth, driven by supportive government policies, technological advancements, and increasing consumer awareness of sustainability. Strategic opportunities exist for companies focused on innovation, efficiency improvements, and diversification of feedstocks. The expanding applications of bio-ethanol beyond transportation fuel, coupled with further integration into the circular economy, present significant future market potential. The development and commercialization of advanced biofuels will play a crucial role in shaping the industry's long-term trajectory and competitiveness.

North America Bio-ethanol Industry Segmentation

-

1. Feedstock Type

- 1.1. Sugarcane

- 1.2. Corn

- 1.3. Wheat

- 1.4. Other Feedstocks

-

2. Application

- 2.1. Automotive and Transportation

- 2.2. Food and Beverage

- 2.3. Pharmaceutical

- 2.4. Cosmetics and Personal Care

- 2.5. Other Applications

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

North America Bio-ethanol Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America Bio-ethanol Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies; Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels

- 3.3. Market Restrains

- 3.3.1. Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles; Shifting Focus to Bio-butanol

- 3.4. Market Trends

- 3.4.1. Automotive and Transportation Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 5.1.1. Sugarcane

- 5.1.2. Corn

- 5.1.3. Wheat

- 5.1.4. Other Feedstocks

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive and Transportation

- 5.2.2. Food and Beverage

- 5.2.3. Pharmaceutical

- 5.2.4. Cosmetics and Personal Care

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 6. United States North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 6.1.1. Sugarcane

- 6.1.2. Corn

- 6.1.3. Wheat

- 6.1.4. Other Feedstocks

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive and Transportation

- 6.2.2. Food and Beverage

- 6.2.3. Pharmaceutical

- 6.2.4. Cosmetics and Personal Care

- 6.2.5. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 7. Canada North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 7.1.1. Sugarcane

- 7.1.2. Corn

- 7.1.3. Wheat

- 7.1.4. Other Feedstocks

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Automotive and Transportation

- 7.2.2. Food and Beverage

- 7.2.3. Pharmaceutical

- 7.2.4. Cosmetics and Personal Care

- 7.2.5. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 8. Mexico North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 8.1.1. Sugarcane

- 8.1.2. Corn

- 8.1.3. Wheat

- 8.1.4. Other Feedstocks

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Automotive and Transportation

- 8.2.2. Food and Beverage

- 8.2.3. Pharmaceutical

- 8.2.4. Cosmetics and Personal Care

- 8.2.5. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Feedstock Type

- 9. United States North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Bio-ethanol Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 ADM

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Cenovus Inc

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Cropenergies AG

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Henan Tianguan Group Co Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Alto Ingredients Inc

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Green Plains Inc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Suncor Energy Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Valero

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Ethanol Technologies

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Verbio Vereinigte Bioenergie AG*List Not Exhaustive

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Abengoa

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Granbio Investimentos SA

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 Sekab

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Blue Bio Fuels Inc

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 Lantmannen

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.16 Cristalco

- 13.2.16.1. Overview

- 13.2.16.2. Products

- 13.2.16.3. SWOT Analysis

- 13.2.16.4. Recent Developments

- 13.2.16.5. Financials (Based on Availability)

- 13.2.17 Poet LLC

- 13.2.17.1. Overview

- 13.2.17.2. Products

- 13.2.17.3. SWOT Analysis

- 13.2.17.4. Recent Developments

- 13.2.17.5. Financials (Based on Availability)

- 13.2.18 Jilin Fuel Ethanol Co Ltd

- 13.2.18.1. Overview

- 13.2.18.2. Products

- 13.2.18.3. SWOT Analysis

- 13.2.18.4. Recent Developments

- 13.2.18.5. Financials (Based on Availability)

- 13.2.19 Raizen

- 13.2.19.1. Overview

- 13.2.19.2. Products

- 13.2.19.3. SWOT Analysis

- 13.2.19.4. Recent Developments

- 13.2.19.5. Financials (Based on Availability)

- 13.2.20 KWST

- 13.2.20.1. Overview

- 13.2.20.2. Products

- 13.2.20.3. SWOT Analysis

- 13.2.20.4. Recent Developments

- 13.2.20.5. Financials (Based on Availability)

- 13.2.1 ADM

List of Figures

- Figure 1: North America Bio-ethanol Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Bio-ethanol Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Bio-ethanol Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 3: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Bio-ethanol Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Bio-ethanol Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 12: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 13: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 16: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Bio-ethanol Industry Revenue Million Forecast, by Feedstock Type 2019 & 2032

- Table 20: North America Bio-ethanol Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 21: North America Bio-ethanol Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Bio-ethanol Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Bio-ethanol Industry?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the North America Bio-ethanol Industry?

Key companies in the market include ADM, Cenovus Inc, Cropenergies AG, Henan Tianguan Group Co Ltd, Alto Ingredients Inc, Green Plains Inc, Suncor Energy Inc, Valero, Ethanol Technologies, Verbio Vereinigte Bioenergie AG*List Not Exhaustive, Abengoa, Granbio Investimentos SA, Sekab, Blue Bio Fuels Inc, Lantmannen, Cristalco, Poet LLC, Jilin Fuel Ethanol Co Ltd, Raizen, KWST.

3. What are the main segments of the North America Bio-ethanol Industry?

The market segments include Feedstock Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies; Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels.

6. What are the notable trends driving market growth?

Automotive and Transportation Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles; Shifting Focus to Bio-butanol.

8. Can you provide examples of recent developments in the market?

May 2022: VERBIO AG opened the first cellulosic RNG plant in the United States, achieving full-scale production of 7 million ethanol gallons equivalent (EGE) of RNG annually by mid-summer 2022. In 2023, this project is expected to start functioning as a biorefinery, producing 60 million gallons of corn-based ethanol annually.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Bio-ethanol Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Bio-ethanol Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Bio-ethanol Industry?

To stay informed about further developments, trends, and reports in the North America Bio-ethanol Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence