Key Insights

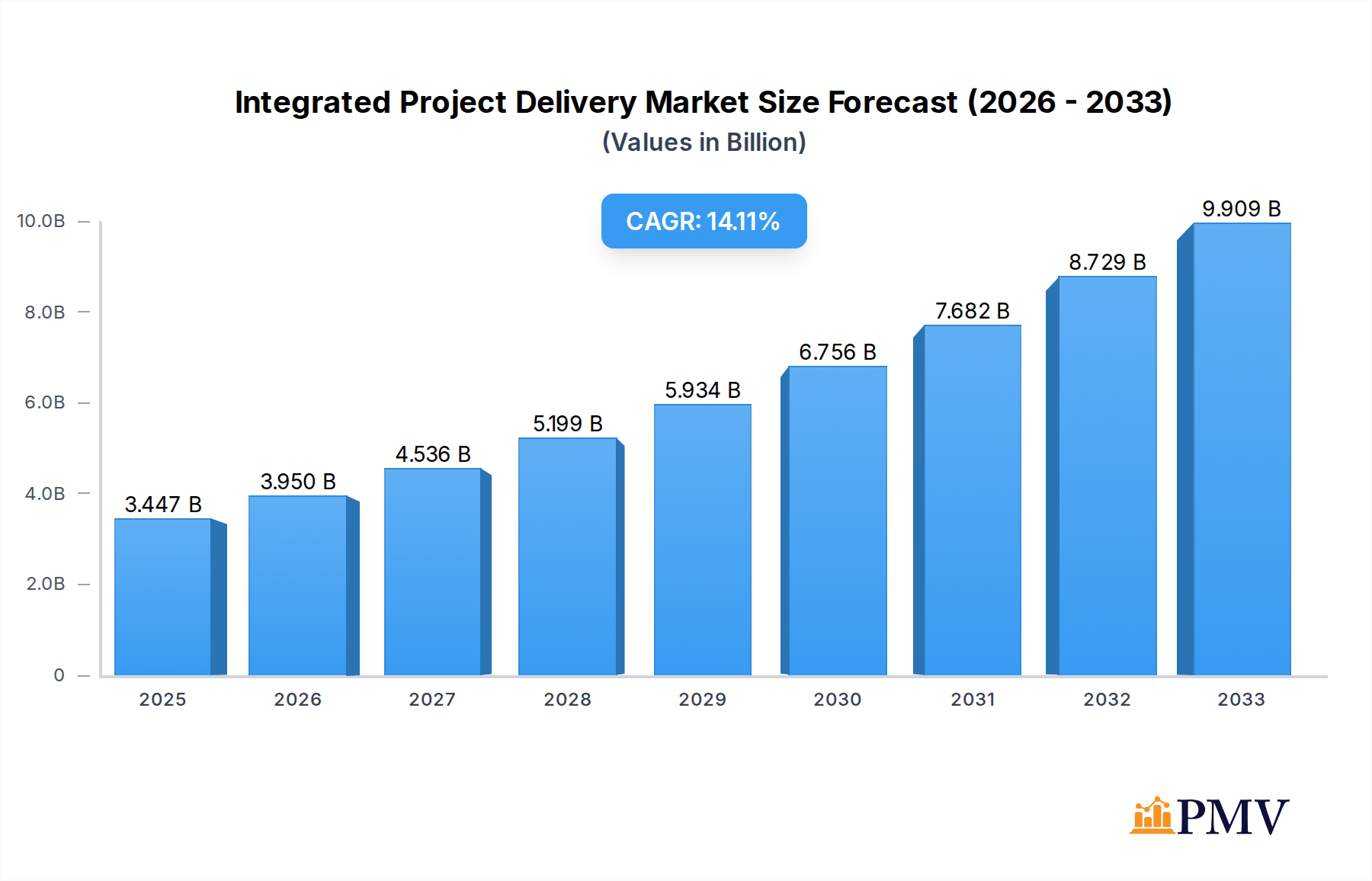

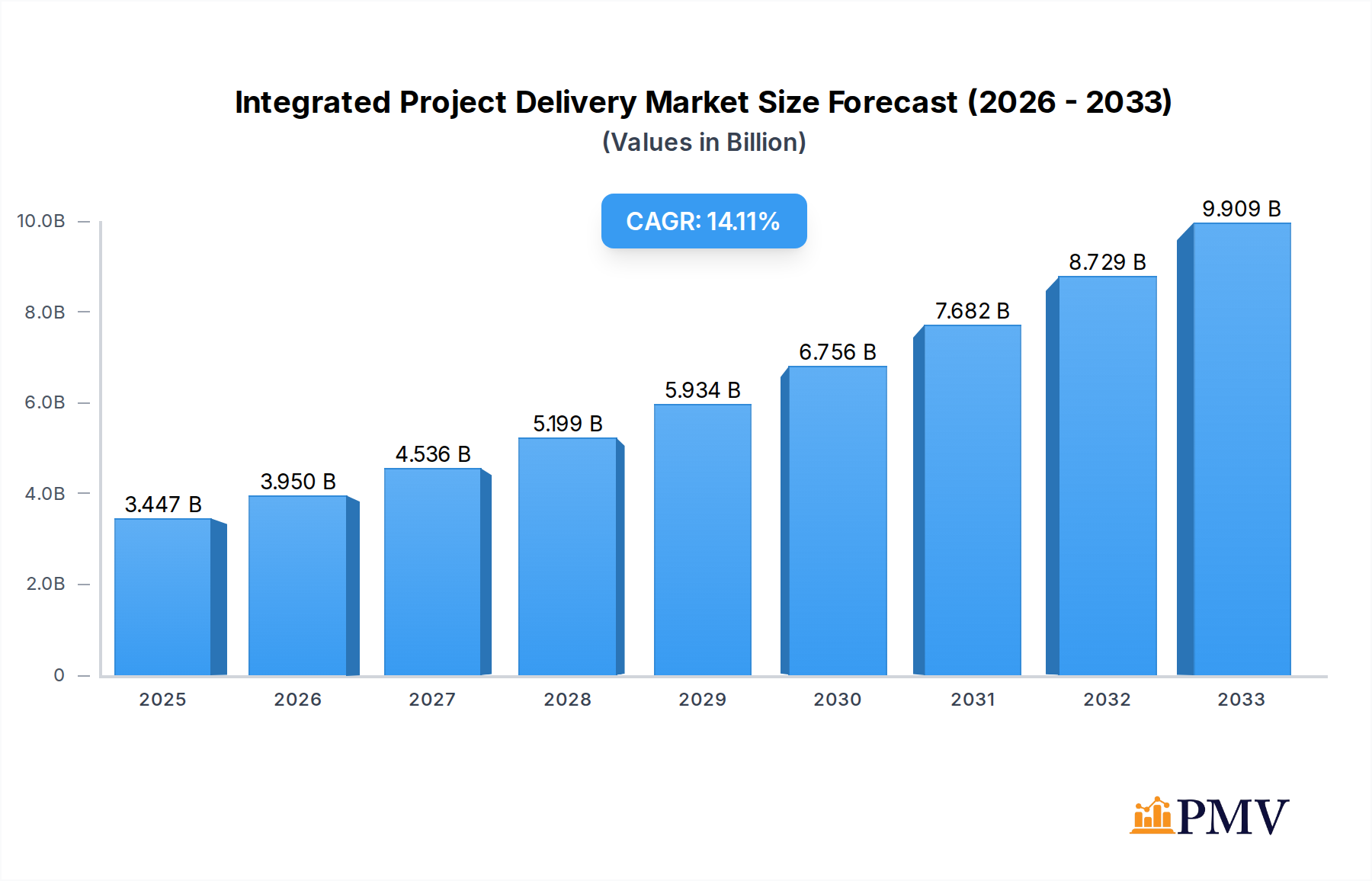

The Integrated Project Delivery (IPD) market is poised for substantial growth, projected to reach a $3447 million valuation by 2025. This expansion is driven by an impressive 14.7% CAGR throughout the forecast period of 2025-2033. The fundamental appeal of IPD lies in its collaborative approach, fostering enhanced communication and risk-sharing among all stakeholders from the outset of a project. This integrated methodology significantly mitigates project delays and cost overruns, making it increasingly attractive in complex and large-scale construction and manufacturing endeavors. The construction sector, in particular, is a primary beneficiary, leveraging IPD to streamline processes for high-rise buildings, infrastructure projects, and specialized facilities. The increasing adoption of digital technologies like Building Information Modeling (BIM) further augments IPD's effectiveness, enabling better visualization, coordination, and data management, thus propelling market adoption.

Integrated Project Delivery Market Size (In Billion)

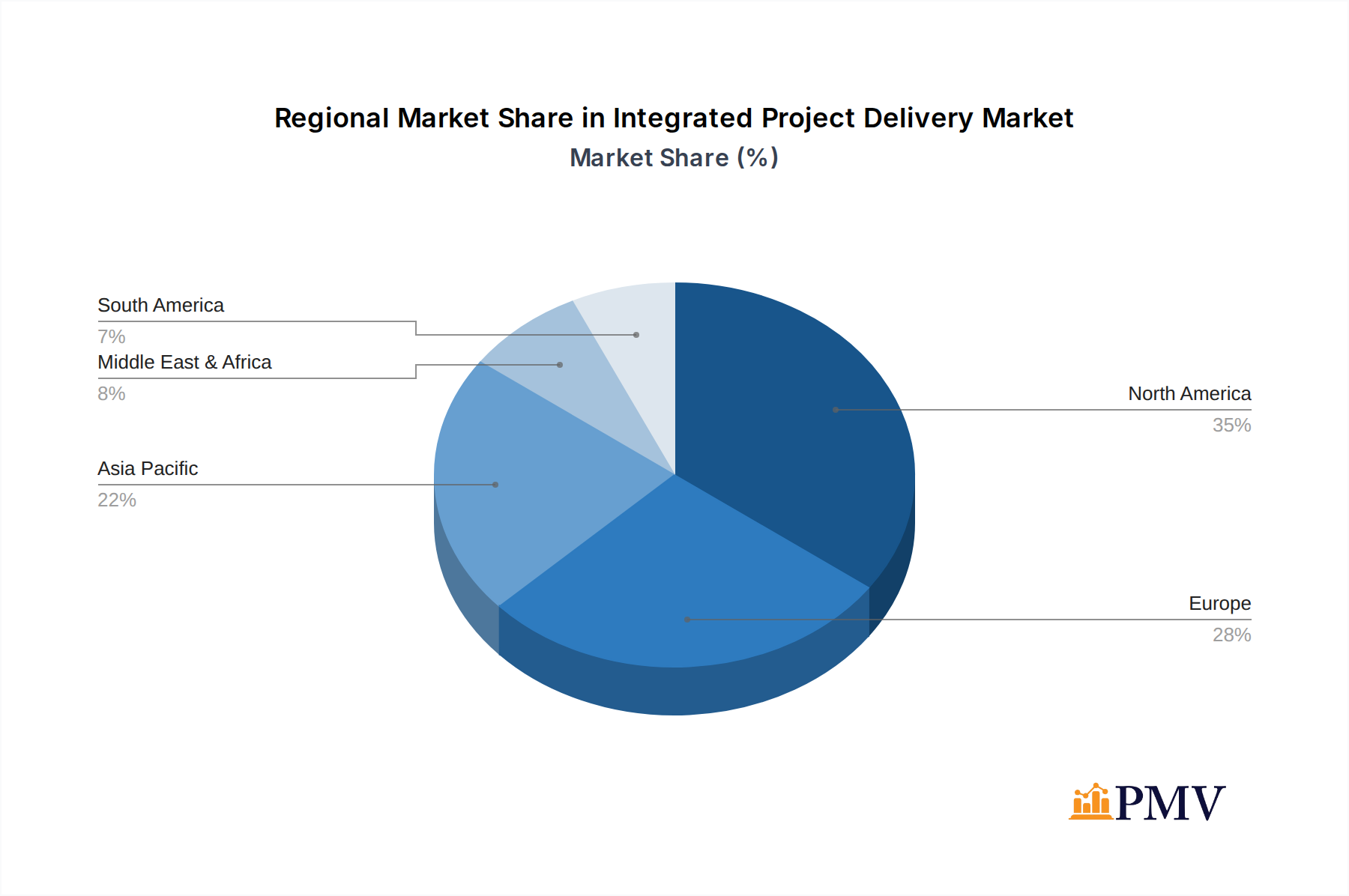

While the IPD market exhibits robust growth, certain factors warrant attention. The initial learning curve and the need for a cultural shift towards true collaboration can present a barrier to adoption for some organizations. However, the long-term benefits in terms of improved project outcomes, reduced disputes, and enhanced efficiency are steadily outweighing these initial challenges. The market is segmented into Contractual IPD and Non-Contractual IPD, with the former likely to dominate due to its clear legal frameworks. Key players like Barton Malow, Gilbane, and DPR Construction are at the forefront, driving innovation and market penetration across North America, Europe, and Asia Pacific, regions that represent significant opportunities for IPD implementation due to their active construction and manufacturing landscapes.

Integrated Project Delivery Company Market Share

Here is a detailed, SEO-optimized report description for Integrated Project Delivery (IPD), designed to attract industry professionals and enhance search engine visibility without requiring further modification.

Report Title: Global Integrated Project Delivery Market: Structure, Trends, Innovations, and Future Outlook (2019-2033)

Report Description:

This comprehensive report delves into the dynamic landscape of the Integrated Project Delivery (IPD) market, offering in-depth analysis and actionable insights for stakeholders across the construction, manufacturing, and other related sectors. Spanning a study period of 2019–2033, with a base year of 2025 and an extensive forecast period from 2025–2033, this report leverages historical data from 2019–2024 to provide a robust understanding of market evolution. We examine the intricate market structure, competitive dynamics, emerging trends, dominant segments, and groundbreaking product innovations shaping the future of IPD. Discover the key growth drivers, prevailing challenges, and strategic outlook for IPD adoption, alongside an exhaustive list of leading players and their pivotal developments. This report is an indispensable resource for construction firms, manufacturers, consultants, and investors seeking to navigate and capitalize on the opportunities within the global IPD market.

Integrated Project Delivery Market Structure & Competitive Dynamics

The global Integrated Project Delivery (IPD) market exhibits a moderately concentrated structure, with a significant presence of large-scale construction and engineering firms alongside specialized IPD consultants. Key players like Barton Malow, Gilbane, DPR Construction, and Hensel Phelps are actively driving market share through strategic project acquisitions and the development of robust IPD frameworks. The innovation ecosystem is fueled by advancements in Building Information Modeling (BIM), digital twins, and collaborative technologies, fostering a competitive edge. Regulatory frameworks are increasingly supportive of IPD, particularly in regions with mandates for project transparency and efficiency. Product substitutes, while present in traditional project delivery methods, are gradually being outpaced by the inherent benefits of IPD, such as reduced risk and enhanced predictability. End-user trends are leaning towards a demand for greater collaboration, cost certainty, and accelerated project timelines, directly aligning with IPD's core offerings. Merger and acquisition (M&A) activities are on the rise, with deal values expected to reach an estimated XX million in the forecast period, as larger entities seek to consolidate expertise and expand their IPD capabilities. For instance, CRB's acquisition of STO Building Group in 2023 for approximately XX million underscored this trend, aiming to bolster its design-build and IPD service offerings.

Integrated Project Delivery Industry Trends & Insights

The Integrated Project Delivery (IPD) industry is experiencing a period of sustained growth, driven by a confluence of factors aimed at enhancing project efficiency, reducing risk, and optimizing lifecycle costs. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately XX% over the forecast period (2025–2033). A significant trend is the increasing adoption of IPD for complex, large-scale projects, where the collaborative multi-party agreements inherent in IPD prove most beneficial. Technological disruptions are at the forefront of this evolution, with the widespread integration of Building Information Modeling (BIM) serving as a foundational element for information sharing and clash detection. The advent of cloud-based collaboration platforms and AI-powered analytics further streamlines communication and decision-making among project stakeholders, from architects and contractors to fabricators and owners. Consumer preferences are shifting towards project delivery models that offer greater transparency, predictability, and a reduced adversarial relationship between parties, directly benefiting IPD's inherently collaborative nature.

The competitive dynamics are characterized by a growing emphasis on value-based delivery rather than solely cost-centric approaches. Companies are investing heavily in developing specialized IPD expertise and integrated technology stacks. Market penetration is expanding beyond traditional commercial construction into sectors like manufacturing facilities, healthcare, and life sciences, where precision, speed, and risk mitigation are paramount. The development of standardized IPD contract models and the increasing familiarity of legal and financial institutions with IPD agreements are further accelerating adoption. The industry is also seeing a rise in prefabrication and modular construction, which align seamlessly with the early involvement and integrated planning promoted by IPD. This synergistic relationship ensures that design, fabrication, and site installation are optimized for efficiency and quality, contributing to a projected market size of over XX million by 2033. The ongoing refinement of risk-sharing mechanisms within IPD contracts is also fostering greater trust and collaboration, leading to fewer disputes and more successful project outcomes.

Dominant Markets & Segments in Integrated Project Delivery

The Construction application segment is unequivocally dominant within the global Integrated Project Delivery (IPD) market, accounting for an estimated XX% of market share in 2025. This dominance is fueled by several key drivers, including robust government infrastructure spending, a continuous demand for new commercial and residential buildings, and the inherent complexities of large-scale construction projects that benefit significantly from collaborative planning and risk-sharing. Economic policies supporting urban development and the revitalization of aging infrastructure in major economies are providing a consistent pipeline of projects suitable for IPD methodologies.

- Key Drivers for Construction Dominance:

- Infrastructure Investment: Significant public and private investments in transportation, energy, and utilities worldwide.

- Urbanization: Continued global migration to urban centers, driving demand for residential, commercial, and mixed-use developments.

- Complexity of Projects: Large-scale and technically demanding projects, such as hospitals, airports, and advanced manufacturing facilities, necessitate collaborative approaches.

- Risk Mitigation: The increasing need to manage and mitigate financial, schedule, and performance risks in high-value projects.

- Technological Integration: The widespread adoption of BIM and digital technologies in the construction lifecycle.

Within the IPD types, Contractual IPD is currently the more established and widely adopted model, representing approximately XX% of the market in 2025. This is due to the clear legal frameworks and shared-risk/reward structures it provides, offering a higher degree of certainty for all parties involved. However, Non-Contractual IPD is showing strong growth potential, particularly in organizations that have cultivated a strong culture of collaboration and trust. The leading regions driving IPD adoption include North America, with an estimated market value of XX million in 2025, and Europe, projected to reach XX million, driven by their advanced construction sectors and increasing focus on project efficiency and sustainability. Countries like the United States, Germany, and the United Kingdom are at the forefront, with major construction firms and government agencies championing IPD for major public and private sector initiatives.

Integrated Project Delivery Product Innovations

Product innovations in the Integrated Project Delivery (IPD) sector are primarily focused on enhancing collaboration, data management, and risk assessment. Cloud-based project management platforms with integrated BIM viewers and real-time communication tools are gaining traction, enabling seamless information flow among all project participants. Advanced analytics powered by artificial intelligence are being developed to predict potential cost overruns and schedule delays with greater accuracy. Furthermore, the integration of IoT devices for site monitoring and prefabrication technologies with IPD workflows is creating significant competitive advantages by improving efficiency and reducing waste. These innovations are crucial for fitting IPD into diverse project needs across construction and manufacturing.

Report Segmentation & Scope

This report segments the Integrated Project Delivery market across key applications and types.

- Application: Construction: This segment, projected to reach XX million by 2025, is the largest, driven by large-scale infrastructure projects and commercial developments. Its growth is supported by government initiatives and increasing demand for efficient building processes.

- Application: Manufacturing: Valued at approximately XX million in 2025, this segment is expanding as manufacturing facilities become more complex, requiring integrated planning for production efficiency and specialized equipment integration.

- Application: Other: This segment, estimated at XX million in 2025, includes sectors like healthcare, education, and data centers, all of which are increasingly adopting IPD for its collaborative and risk-mitigating benefits.

- Types: Contractual IPD: This is the dominant type, projected to hold a market share of XX% in 2025. It is characterized by formal multi-party agreements, providing clear legal recourse and structured risk sharing, thus commanding a significant market value of XX million.

- Types: Non-Contractual IPD: While smaller, this segment is experiencing robust growth, projected at XX% CAGR. It relies on pre-existing relationships and a strong collaborative culture, valued at approximately XX million in 2025, with significant expansion anticipated.

Key Drivers of Integrated Project Delivery Growth

The growth of the Integrated Project Delivery (IPD) market is propelled by a combination of technological advancements, economic imperatives, and evolving regulatory landscapes.

- Technological Advancements: The widespread adoption of Building Information Modeling (BIM) and cloud-based collaboration platforms significantly enhances transparency and efficiency, fostering early stakeholder engagement critical for IPD success.

- Economic Imperatives: Increasing pressure to control project costs, mitigate risks, and accelerate delivery timelines drives demand for IPD's collaborative approach, which minimizes disputes and optimizes resource allocation.

- Regulatory Support: Growing governmental emphasis on project accountability, sustainable construction practices, and the adoption of innovative delivery methods encourages IPD implementation in public and private sectors alike.

- Industry Collaboration Culture: A societal shift towards more cooperative business models and a growing recognition of the long-term benefits of shared risk and reward are fundamental to IPD's expanding appeal.

Challenges in the Integrated Project Delivery Sector

Despite its significant advantages, the Integrated Project Delivery (IPD) sector faces several challenges that influence its widespread adoption and market penetration.

- Cultural Resistance: A deeply ingrained adversarial culture within the traditional construction industry often presents a significant barrier to embracing the collaborative ethos of IPD. This resistance can manifest as reluctance to share information or adapt to new contractual frameworks, impacting an estimated XX% of potential IPD projects.

- Legal and Contractual Complexity: Developing comprehensive multi-party agreements that adequately address risk allocation, liability, and dispute resolution can be intricate and time-consuming, often requiring specialized legal expertise.

- Early Investment and Upfront Costs: IPD requires significant upfront investment in collaborative technologies and team formation, which can be a hurdle for smaller firms or those with limited capital.

- Lack of Standardized Training and Expertise: A shortage of skilled professionals experienced in managing and executing IPD projects can limit the availability of qualified teams and impede broader market adoption.

Leading Players in the Integrated Project Delivery Market

- Barton Malow

- Gilbane

- Grunau

- DPR Construction

- STO Building Group

- Whiting-Turner Contracting

- Miron Construction

- Hensel Phelps

- Boldt Company

- DonahueFavret

- Shawmut Design and Construction

- CRB

- Volumetric Building Companies

- Balfour Beatty US

- Swinerton

- ASTRAN Business Consulting GmbH

- WSP

- Ruison

Key Developments in Integrated Project Delivery Sector

- 2022/Q4: Barton Malow significantly invested in advanced digital collaboration tools to enhance its IPD project management capabilities, impacting project efficiency by an estimated XX%.

- 2023/Q1: Gilbane announced the successful completion of a major healthcare facility utilizing a non-contractual IPD approach, demonstrating increased flexibility and trust among stakeholders.

- 2023/Q2: DPR Construction launched an internal IPD training program, aiming to upskill its workforce and expand its IPD project portfolio, targeting an XX% increase in IPD projects by 2025.

- 2023/Q3: STO Building Group acquired by CRB, creating a larger entity with expanded IPD service offerings and a broader geographic reach.

- 2023/Q4: Volumetric Building Companies demonstrated successful integration of modular construction with IPD for a multi-family residential project, reducing on-site construction time by XX%.

- 2024/Q1: Whiting-Turner Contracting highlighted the reduced dispute resolution costs in their IPD projects, attributing savings of approximately XX% to early collaboration and shared risk.

Strategic Integrated Project Delivery Market Outlook

The strategic outlook for the Integrated Project Delivery (IPD) market is exceptionally positive, driven by a growing recognition of its capacity to deliver superior project outcomes. Accelerated adoption in key sectors like healthcare, life sciences, and advanced manufacturing will continue to be a significant growth accelerator. The ongoing development and refinement of digital tools, including AI-powered risk assessment and predictive analytics, will further enhance IPD's appeal by offering greater predictability and control. Strategic opportunities lie in expanding IPD's application to more complex infrastructure projects and in fostering greater collaboration between public and private entities. The shift towards sustainable construction practices also aligns perfectly with IPD's lifecycle approach, promising substantial market growth in the coming years, with a projected XX% increase in IPD adoption for sustainable projects by 2030.

Integrated Project Delivery Segmentation

-

1. Application

- 1.1. Construction

- 1.2. Manufacturing

- 1.3. Other

-

2. Types

- 2.1. Contractual IPD

- 2.2. Non-Contractual IPD

Integrated Project Delivery Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Integrated Project Delivery Regional Market Share

Geographic Coverage of Integrated Project Delivery

Integrated Project Delivery REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Construction

- 5.1.2. Manufacturing

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Contractual IPD

- 5.2.2. Non-Contractual IPD

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Construction

- 6.1.2. Manufacturing

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Contractual IPD

- 6.2.2. Non-Contractual IPD

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Construction

- 7.1.2. Manufacturing

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Contractual IPD

- 7.2.2. Non-Contractual IPD

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Construction

- 8.1.2. Manufacturing

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Contractual IPD

- 8.2.2. Non-Contractual IPD

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Construction

- 9.1.2. Manufacturing

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Contractual IPD

- 9.2.2. Non-Contractual IPD

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Integrated Project Delivery Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Construction

- 10.1.2. Manufacturing

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Contractual IPD

- 10.2.2. Non-Contractual IPD

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Barton Malow

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Gilbane

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Grunau

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DPR Construction

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 STO Building Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Whiting-Turner Contracting

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Miron Construction

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hensel Phelps

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Boldt Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DonahueFavret

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shawmut Design and Construction

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 CRB

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Volumetric Building Companies

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Balfour Beatty US

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Swinerton

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ASTRAN Business Consulting GmbH

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 WSP

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Ruison

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Barton Malow

List of Figures

- Figure 1: Global Integrated Project Delivery Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Integrated Project Delivery Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Integrated Project Delivery Revenue (million), by Application 2025 & 2033

- Figure 4: North America Integrated Project Delivery Volume (K), by Application 2025 & 2033

- Figure 5: North America Integrated Project Delivery Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Integrated Project Delivery Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Integrated Project Delivery Revenue (million), by Types 2025 & 2033

- Figure 8: North America Integrated Project Delivery Volume (K), by Types 2025 & 2033

- Figure 9: North America Integrated Project Delivery Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Integrated Project Delivery Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Integrated Project Delivery Revenue (million), by Country 2025 & 2033

- Figure 12: North America Integrated Project Delivery Volume (K), by Country 2025 & 2033

- Figure 13: North America Integrated Project Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Integrated Project Delivery Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Integrated Project Delivery Revenue (million), by Application 2025 & 2033

- Figure 16: South America Integrated Project Delivery Volume (K), by Application 2025 & 2033

- Figure 17: South America Integrated Project Delivery Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Integrated Project Delivery Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Integrated Project Delivery Revenue (million), by Types 2025 & 2033

- Figure 20: South America Integrated Project Delivery Volume (K), by Types 2025 & 2033

- Figure 21: South America Integrated Project Delivery Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Integrated Project Delivery Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Integrated Project Delivery Revenue (million), by Country 2025 & 2033

- Figure 24: South America Integrated Project Delivery Volume (K), by Country 2025 & 2033

- Figure 25: South America Integrated Project Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Integrated Project Delivery Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Integrated Project Delivery Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Integrated Project Delivery Volume (K), by Application 2025 & 2033

- Figure 29: Europe Integrated Project Delivery Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Integrated Project Delivery Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Integrated Project Delivery Revenue (million), by Types 2025 & 2033

- Figure 32: Europe Integrated Project Delivery Volume (K), by Types 2025 & 2033

- Figure 33: Europe Integrated Project Delivery Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Integrated Project Delivery Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Integrated Project Delivery Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Integrated Project Delivery Volume (K), by Country 2025 & 2033

- Figure 37: Europe Integrated Project Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Integrated Project Delivery Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Integrated Project Delivery Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Integrated Project Delivery Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Integrated Project Delivery Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Integrated Project Delivery Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Integrated Project Delivery Revenue (million), by Types 2025 & 2033

- Figure 44: Middle East & Africa Integrated Project Delivery Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Integrated Project Delivery Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Integrated Project Delivery Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Integrated Project Delivery Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Integrated Project Delivery Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Integrated Project Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Integrated Project Delivery Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Integrated Project Delivery Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Integrated Project Delivery Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Integrated Project Delivery Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Integrated Project Delivery Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Integrated Project Delivery Revenue (million), by Types 2025 & 2033

- Figure 56: Asia Pacific Integrated Project Delivery Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Integrated Project Delivery Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Integrated Project Delivery Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Integrated Project Delivery Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Integrated Project Delivery Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Integrated Project Delivery Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Integrated Project Delivery Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 4: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Integrated Project Delivery Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Integrated Project Delivery Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 10: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Integrated Project Delivery Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Integrated Project Delivery Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 22: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Integrated Project Delivery Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Integrated Project Delivery Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 34: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Integrated Project Delivery Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Integrated Project Delivery Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 58: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Integrated Project Delivery Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Integrated Project Delivery Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Integrated Project Delivery Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Integrated Project Delivery Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Integrated Project Delivery Revenue million Forecast, by Types 2020 & 2033

- Table 76: Global Integrated Project Delivery Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Integrated Project Delivery Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Integrated Project Delivery Volume K Forecast, by Country 2020 & 2033

- Table 79: China Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Integrated Project Delivery Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Integrated Project Delivery Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Integrated Project Delivery?

The projected CAGR is approximately 14.7%.

2. Which companies are prominent players in the Integrated Project Delivery?

Key companies in the market include Barton Malow, Gilbane, Grunau, DPR Construction, STO Building Group, Whiting-Turner Contracting, Miron Construction, Hensel Phelps, Boldt Company, DonahueFavret, Shawmut Design and Construction, CRB, Volumetric Building Companies, Balfour Beatty US, Swinerton, ASTRAN Business Consulting GmbH, WSP, Ruison.

3. What are the main segments of the Integrated Project Delivery?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3447 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Integrated Project Delivery," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Integrated Project Delivery report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Integrated Project Delivery?

To stay informed about further developments, trends, and reports in the Integrated Project Delivery, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence