Key Insights

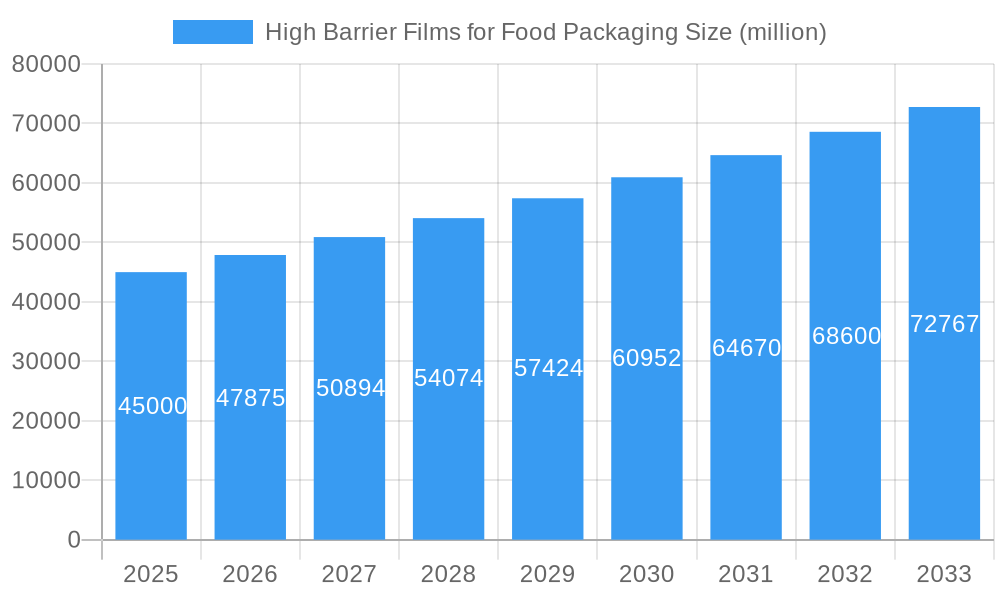

The global High Barrier Films for Food Packaging market is projected for substantial growth, with an estimated market size of USD 38 billion by 2025 and a Compound Annual Growth Rate (CAGR) of 5.5% from 2025 to 2033. This expansion is driven by increasing consumer demand for extended shelf-life and superior food safety, fueled by preferences for convenience and premium packaged goods. The rising consumption of processed foods, fresh produce, and seafood are key demand drivers. Furthermore, the films' critical role in reducing food waste by preserving product freshness significantly contributes to market momentum. Innovations in material science are introducing more sustainable and high-performance barrier films, such as PLA, addressing both environmental concerns and performance requirements.

High Barrier Films for Food Packaging Market Size (In Billion)

The market features intense competition among established players and emerging innovators. Segmentation spans applications like fresh meat, seafood, processed foods, and fruits and vegetables, each with distinct barrier needs. PET, CPP, and BOPP films currently hold significant market share, but the adoption of eco-friendly options like PLA is a notable trend. Asia Pacific, particularly China and India, is a major growth hub due to industrialization, a growing middle class, and rising disposable incomes. North America and Europe remain crucial markets, supported by stringent food safety regulations and consumer demand for high-quality packaging. Market restraints, including fluctuating raw material prices and initial investment costs for advanced technologies, are being addressed through continuous advancements and strategic partnerships.

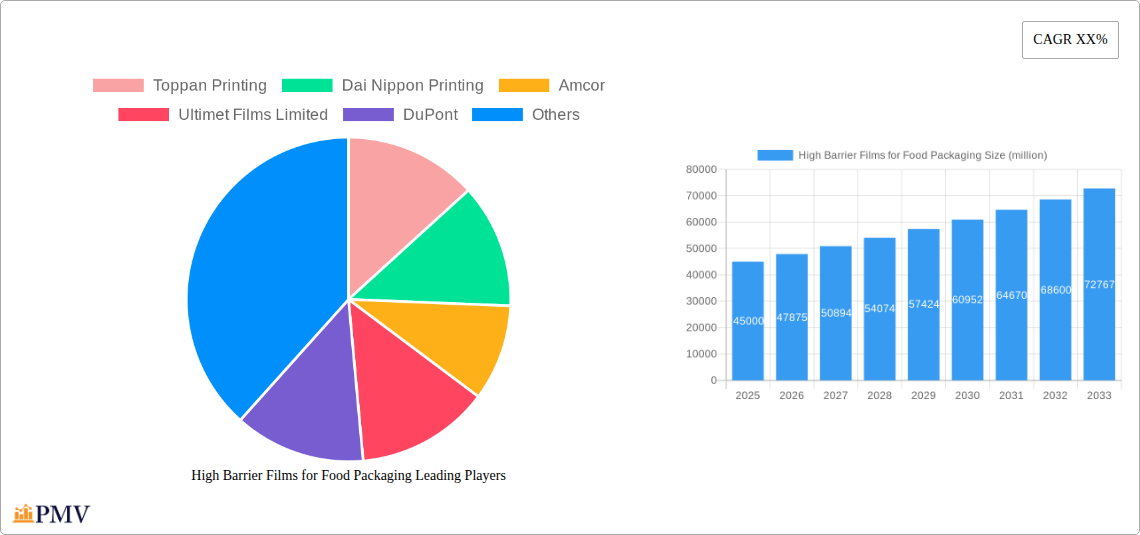

High Barrier Films for Food Packaging Company Market Share

This report offers an SEO-optimized, detailed analysis of the High Barrier Films for Food Packaging market to enhance search visibility and engage industry professionals.

This in-depth market report provides a definitive analysis of the high barrier films for food packaging market, offering critical insights for stakeholders navigating this dynamic sector. Spanning a study period from 2019 to 2033, with a base year of 2025, this report meticulously details the market structure, competitive landscape, industry trends, dominant markets, and future outlook. Leveraging an extensive forecast period from 2025 to 2033, our analysis highlights key growth drivers, technological innovations, and potential challenges impacting the global food packaging industry. We delve into specific segments including PET, CPP, BOPP, PVA, PLA high barrier films and applications for Fresh Meat, Seafood, Processed Foods, Fruits and Vegetables, providing granular data and actionable intelligence. This report is an indispensable resource for packaging manufacturers, food producers, material suppliers, and investors seeking to understand and capitalize on the evolving demands for advanced food preservation solutions and extended shelf-life packaging.

High Barrier Films for Food Packaging Market Structure & Competitive Dynamics

The high barrier films for food packaging market exhibits a moderately concentrated structure, with a mix of large, diversified players and specialized innovators. Market leaders like Toppan Printing, Dai Nippon Printing, Amcor, and DuPont hold significant market share, driven by extensive R&D capabilities and global distribution networks. The innovation ecosystem is robust, fueled by increasing demand for sustainable high barrier packaging solutions and enhanced food safety. Regulatory frameworks, particularly concerning food contact materials and environmental impact, are increasingly shaping market dynamics, encouraging the adoption of advanced and compliant barrier film technologies. Product substitutes, such as rigid packaging and alternative preservation methods, are present but face limitations in cost-effectiveness and flexibility compared to modern flexible barrier films. End-user trends are heavily influenced by consumer demand for longer shelf life, reduced food waste, and convenience, directly stimulating growth in sectors requiring superior oxygen and moisture barriers. Mergers and acquisitions (M&A) have been strategic, focusing on acquiring innovative technologies or expanding market reach. For instance, M&A deal values in the past five years have reached over $500 million, with acquisitions targeting companies with specialized high barrier film extrusion or coating capabilities. The market penetration of advanced high barrier films is projected to reach 65% by 2030.

High Barrier Films for Food Packaging Industry Trends & Insights

The high barrier films for food packaging industry is experiencing robust growth, projected to grow at a CAGR of 6.2% from 2025 to 2033. This expansion is primarily driven by an escalating global demand for extended shelf-life food packaging, which significantly reduces food spoilage and waste. Consumers are increasingly prioritizing food safety and quality, thereby boosting the adoption of high barrier films capable of protecting sensitive food products from oxygen, moisture, light, and aroma loss. Technological disruptions are at the forefront of this trend, with advancements in material science leading to the development of novel multilayer barrier films and sophisticated coating technologies. These innovations enable thinner, stronger, and more sustainable barrier packaging solutions. The integration of nanotechnology and bio-based materials into high barrier films is a significant trend, offering improved performance and enhanced environmental profiles, aligning with corporate sustainability goals and consumer preferences for eco-friendly options. Competitive dynamics are intensifying, with players investing heavily in R&D to develop proprietary barrier film technologies and differentiated product offerings. The market penetration of high barrier films in developed economies is already high, at approximately 70%, while emerging markets present substantial untapped potential, projected to grow at a CAGR of 7.5%. The increasing awareness and stringent regulations regarding food waste are acting as significant catalysts for the widespread adoption of high barrier packaging solutions. The processed foods and fresh meat and seafood segments are leading this demand, driven by the need for enhanced product integrity during longer distribution chains. The overall market size is estimated to reach $25 billion by 2033.

Dominant Markets & Segments in High Barrier Films for Food Packaging

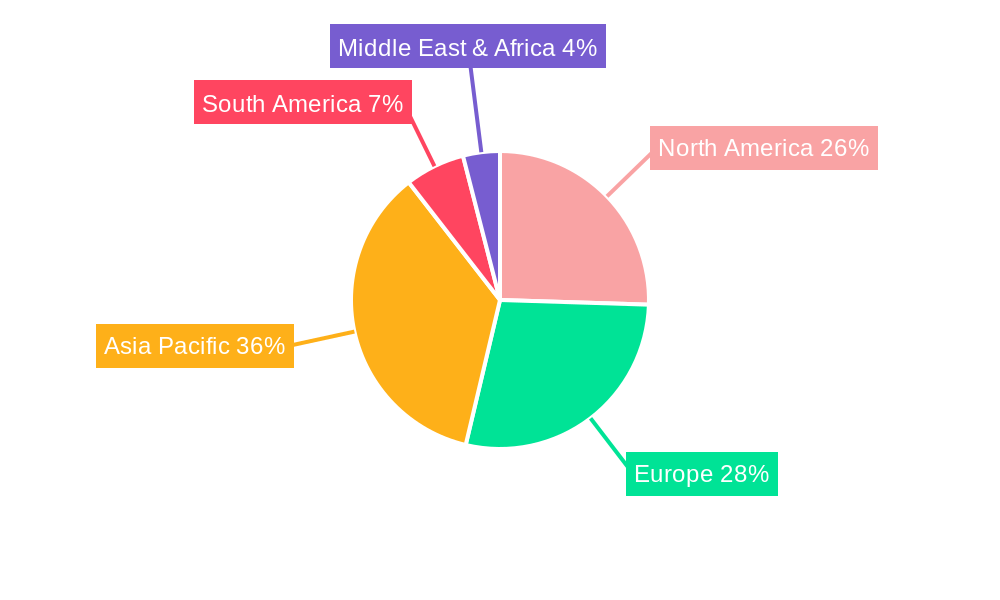

The high barrier films for food packaging market is currently dominated by Asia-Pacific, with China leading the charge due to its massive food production and consumption base, coupled with significant government initiatives supporting advanced manufacturing and sustainable packaging. The region's economic policies favoring industrial growth and substantial investments in infrastructure for food processing and distribution create a fertile ground for high barrier film adoption. Within this region, Processed Foods represent the largest application segment, accounting for an estimated 30% of the market share. This is closely followed by Fresh Meat and Seafood, which demand superior oxygen barriers to maintain freshness and extend shelf life, contributing approximately 25% of the market.

The PET (Polyethylene Terephthalate) type of high barrier film is a dominant material, holding about 35% of the market due to its excellent clarity, mechanical strength, and barrier properties against oxygen and moisture. BOPP (Biaxially Oriented Polypropylene) films are also significant, particularly for their cost-effectiveness and good moisture barrier, capturing around 20% of the market.

Key drivers for this regional dominance include:

- Strong economic growth and rising disposable incomes: Leading to increased demand for packaged food products.

- Government support for food processing and export: Encouraging the use of advanced packaging to meet international standards.

- Rapid urbanization: Increasing the need for convenient, ready-to-eat, and longer-lasting food options.

- Growing middle class: Driving demand for premium and safe food products.

North America and Europe are also substantial markets, driven by high consumer awareness regarding food safety and sustainability, and the presence of major food manufacturers and packaging converters. However, the growth rate in these regions is more mature compared to Asia-Pacific.

High Barrier Films for Food Packaging Product Innovations

Product innovations in high barrier films for food packaging are primarily focused on enhancing barrier performance, improving sustainability, and enabling advanced functionalities. Developments include the introduction of novel multilayer structures incorporating advanced polymers and nanocoatings that significantly reduce oxygen and moisture transmission rates, extending shelf life beyond 30 days for sensitive products like fresh meat and seafood. The incorporation of bio-based and recyclable materials, such as PLA (Polylactic Acid), is a key trend, addressing environmental concerns and meeting consumer demand for eco-friendly packaging. These innovations offer a competitive advantage by meeting stringent regulatory requirements and consumer preferences for sustainable, high-performance food packaging solutions.

Report Segmentation & Scope

This report segments the high barrier films for food packaging market across key applications and material types.

Application Segments:

- Fresh Meat: Driven by the need for oxygen barriers to prevent spoilage and maintain color. This segment is projected to reach $6 billion by 2033.

- Seafood: Requiring exceptional barrier properties against oxygen and moisture to preserve freshness. Estimated market size of $4 billion by 2033.

- Processed Foods: Benefiting from extended shelf life and protection against contamination. This segment is expected to grow to $7 billion by 2033.

- Fruits and Vegetables: Utilizing barrier films to control respiration and extend freshness. Projected market of $3 billion by 2033.

- Other: Encompassing niche applications like dairy, snacks, and ready-to-eat meals. Expected to reach $5 billion by 2033.

Type Segments:

- PET: Dominant due to its excellent clarity and barrier properties, holding an estimated $8 billion market share.

- CPP: Valued for its heat sealability and moisture barrier, with a projected $4 billion market.

- BOPP: Offering cost-effectiveness and good moisture barrier, estimated at $5 billion.

- PVA: Known for its superior oxygen barrier properties, contributing approximately $2 billion.

- PLA: Emerging as a sustainable alternative, with a growing market of $1.5 billion.

- Others: Including specialized films like EVOH and nylon, with an estimated $1.5 billion market.

Key Drivers of High Barrier Films for Food Packaging Growth

The growth of the high barrier films for food packaging market is propelled by several interconnected factors.

- Increasing consumer demand for longer shelf-life products: Directly translates to the need for superior barrier properties to reduce food waste.

- Growing global population and urbanization: Enhances the demand for convenient, safe, and preserved food options.

- Technological advancements in film manufacturing: Leading to improved performance, thinner films, and cost-effectiveness, with an estimated 5% reduction in production costs over the forecast period.

- Stringent food safety regulations: Mandating higher standards for packaging to protect consumers.

- Focus on reducing food spoilage: Both from a consumer perspective and for major food retailers aiming to minimize losses, estimated at a $1 trillion global impact.

Challenges in the High Barrier Films for Food Packaging Sector

Despite strong growth, the high barrier films for food packaging sector faces notable challenges.

- Recyclability concerns: The complex multilayer structures of many high barrier films hinder their recyclability, creating environmental pressures and regulatory hurdles.

- Volatility of raw material prices: Fluctuations in the cost of petrochemicals and other raw materials can impact profit margins, with price variations of up to 15% observed in the historical period.

- Competition from alternative packaging solutions: Including rigid packaging and emerging biodegradable materials that may offer different benefits.

- High initial investment for advanced manufacturing technologies: Can be a barrier for smaller players entering the market.

- Energy-intensive production processes: Contributing to a higher carbon footprint for some barrier film types.

Leading Players in the High Barrier Films for Food Packaging Market

- Toppan Printing

- Dai Nippon Printing

- Amcor

- Ultimet Films Limited

- DuPont

- Toray Advanced Film

- Mitsubishi PLASTICS

- Toyobo

- Schur Flexibles Group

- Sealed Air

- Mondi

- Wipak

- 3M

- QIKE

- Berry Plastics

- Taghleef Industries

- Fraunhofer POLO

- Sunrise

- JBF RAK

- Konica Minolta

- FUJIFILM

- Biofilm

Key Developments in High Barrier Films for Food Packaging Sector

- 2023 October: Amcor launches new recyclable high barrier films for snacks, enhancing sustainability in the flexible packaging market.

- 2023 May: DuPont introduces advanced barrier coatings for PET bottles, offering improved protection and shelf life.

- 2022 November: Toppan Printing develops a novel bio-based high barrier film with a significant reduction in carbon footprint.

- 2022 July: Dai Nippon Printing announces investment in advanced extrusion technology for enhanced barrier film production.

- 2021 September: Fraunhofer POLO showcases innovative vacuum coating techniques for superior oxygen barrier performance.

- 2021 March: Toray Advanced Film expands its production capacity for high barrier films to meet growing demand in Asia.

Strategic High Barrier Films for Food Packaging Market Outlook

The strategic outlook for the high barrier films for food packaging market is highly positive, driven by a confluence of increasing consumer demand for safety and convenience, coupled with a growing imperative for sustainability. The market is poised for continued expansion as innovations in material science unlock new possibilities for performance and eco-friendliness. Key growth accelerators will include the development of monolayer recyclable high barrier films, the integration of smart packaging features, and expanded applications in minimally processed and fresh food categories. Companies that can effectively balance advanced barrier properties with sustainable end-of-life solutions will be best positioned to capture market share and lead the industry towards a future of efficient, safe, and responsible food packaging. Strategic partnerships and continued investment in R&D for advanced barrier solutions will be crucial for maintaining competitive advantage.

High Barrier Films for Food Packaging Segmentation

-

1. Application

- 1.1. Fresh Meat

- 1.2. Seafood

- 1.3. Processed Foods

- 1.4. Fruits and Vegetables

- 1.5. Other

-

2. Types

- 2.1. PET

- 2.2. CPP

- 2.3. BOPP

- 2.4. PVA

- 2.5. PLA

- 2.6. Others

High Barrier Films for Food Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Barrier Films for Food Packaging Regional Market Share

Geographic Coverage of High Barrier Films for Food Packaging

High Barrier Films for Food Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Fresh Meat

- 5.1.2. Seafood

- 5.1.3. Processed Foods

- 5.1.4. Fruits and Vegetables

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PET

- 5.2.2. CPP

- 5.2.3. BOPP

- 5.2.4. PVA

- 5.2.5. PLA

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Fresh Meat

- 6.1.2. Seafood

- 6.1.3. Processed Foods

- 6.1.4. Fruits and Vegetables

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PET

- 6.2.2. CPP

- 6.2.3. BOPP

- 6.2.4. PVA

- 6.2.5. PLA

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Fresh Meat

- 7.1.2. Seafood

- 7.1.3. Processed Foods

- 7.1.4. Fruits and Vegetables

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PET

- 7.2.2. CPP

- 7.2.3. BOPP

- 7.2.4. PVA

- 7.2.5. PLA

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Fresh Meat

- 8.1.2. Seafood

- 8.1.3. Processed Foods

- 8.1.4. Fruits and Vegetables

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PET

- 8.2.2. CPP

- 8.2.3. BOPP

- 8.2.4. PVA

- 8.2.5. PLA

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Fresh Meat

- 9.1.2. Seafood

- 9.1.3. Processed Foods

- 9.1.4. Fruits and Vegetables

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PET

- 9.2.2. CPP

- 9.2.3. BOPP

- 9.2.4. PVA

- 9.2.5. PLA

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Fresh Meat

- 10.1.2. Seafood

- 10.1.3. Processed Foods

- 10.1.4. Fruits and Vegetables

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PET

- 10.2.2. CPP

- 10.2.3. BOPP

- 10.2.4. PVA

- 10.2.5. PLA

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Barrier Films for Food Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Fresh Meat

- 11.1.2. Seafood

- 11.1.3. Processed Foods

- 11.1.4. Fruits and Vegetables

- 11.1.5. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. PET

- 11.2.2. CPP

- 11.2.3. BOPP

- 11.2.4. PVA

- 11.2.5. PLA

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Toppan Printing

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dai Nippon Printing

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Amcor

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ultimet Films Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 DuPont

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Toray Advanced Film

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Mitsubishi PLASTICS

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Toyobo

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Schur Flexibles Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sealed Air

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Mondi

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Wipak

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 3M

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 QIKE

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Berry Plastics

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Taghleef Industries

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Fraunhofer POLO

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Sunrise

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 JBF RAK

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Konica Minolta

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 FUJIFILM

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Biofilm

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Toppan Printing

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Barrier Films for Food Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High Barrier Films for Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America High Barrier Films for Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Barrier Films for Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America High Barrier Films for Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America High Barrier Films for Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America High Barrier Films for Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Barrier Films for Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America High Barrier Films for Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Barrier Films for Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America High Barrier Films for Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America High Barrier Films for Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America High Barrier Films for Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Barrier Films for Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe High Barrier Films for Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Barrier Films for Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe High Barrier Films for Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe High Barrier Films for Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe High Barrier Films for Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Barrier Films for Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Barrier Films for Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Barrier Films for Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa High Barrier Films for Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa High Barrier Films for Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Barrier Films for Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Barrier Films for Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific High Barrier Films for Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Barrier Films for Food Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific High Barrier Films for Food Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific High Barrier Films for Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific High Barrier Films for Food Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global High Barrier Films for Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Barrier Films for Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Barrier Films for Food Packaging?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the High Barrier Films for Food Packaging?

Key companies in the market include Toppan Printing, Dai Nippon Printing, Amcor, Ultimet Films Limited, DuPont, Toray Advanced Film, Mitsubishi PLASTICS, Toyobo, Schur Flexibles Group, Sealed Air, Mondi, Wipak, 3M, QIKE, Berry Plastics, Taghleef Industries, Fraunhofer POLO, Sunrise, JBF RAK, Konica Minolta, FUJIFILM, Biofilm.

3. What are the main segments of the High Barrier Films for Food Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 38 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Barrier Films for Food Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Barrier Films for Food Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Barrier Films for Food Packaging?

To stay informed about further developments, trends, and reports in the High Barrier Films for Food Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence