Key Insights

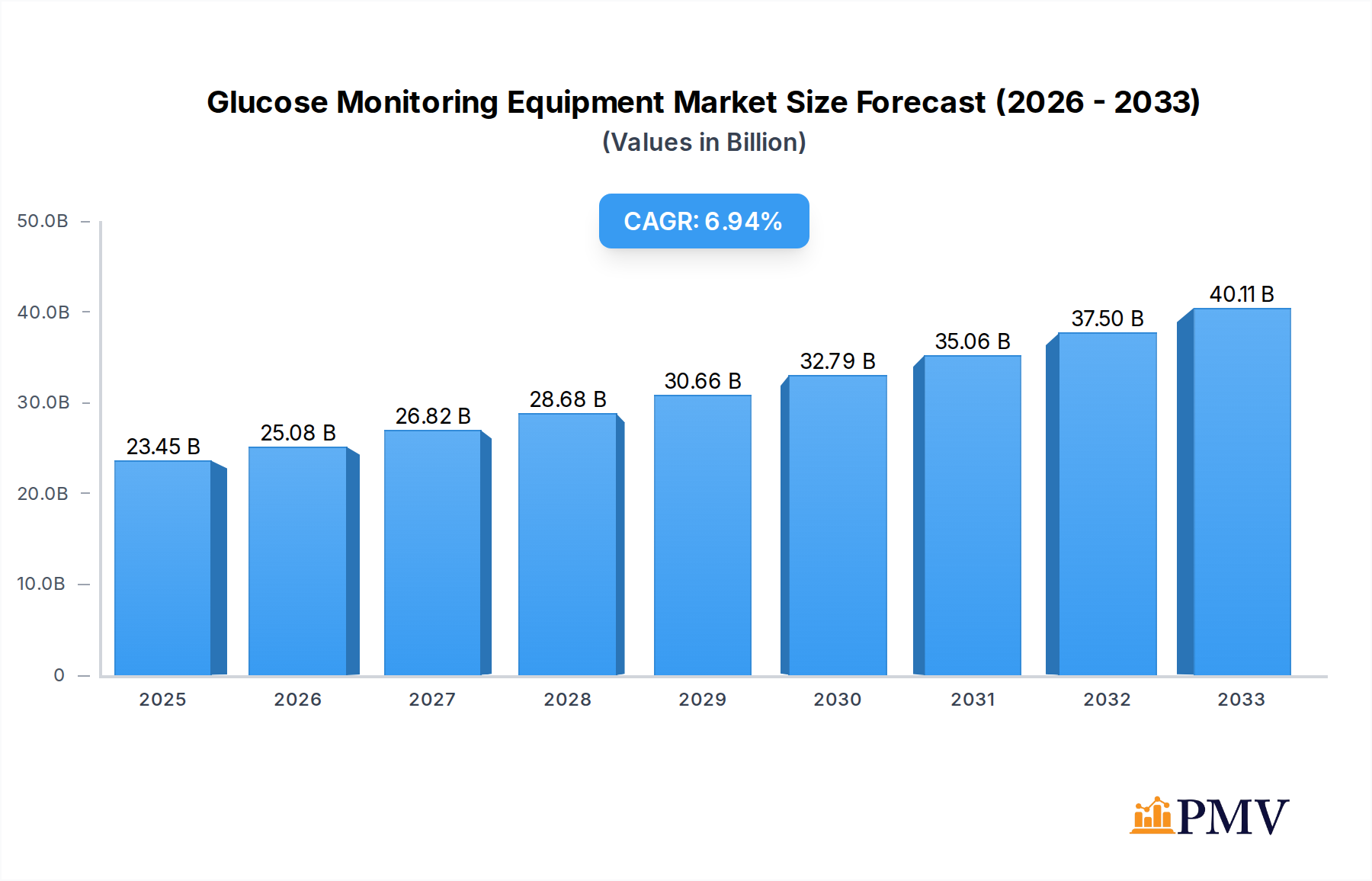

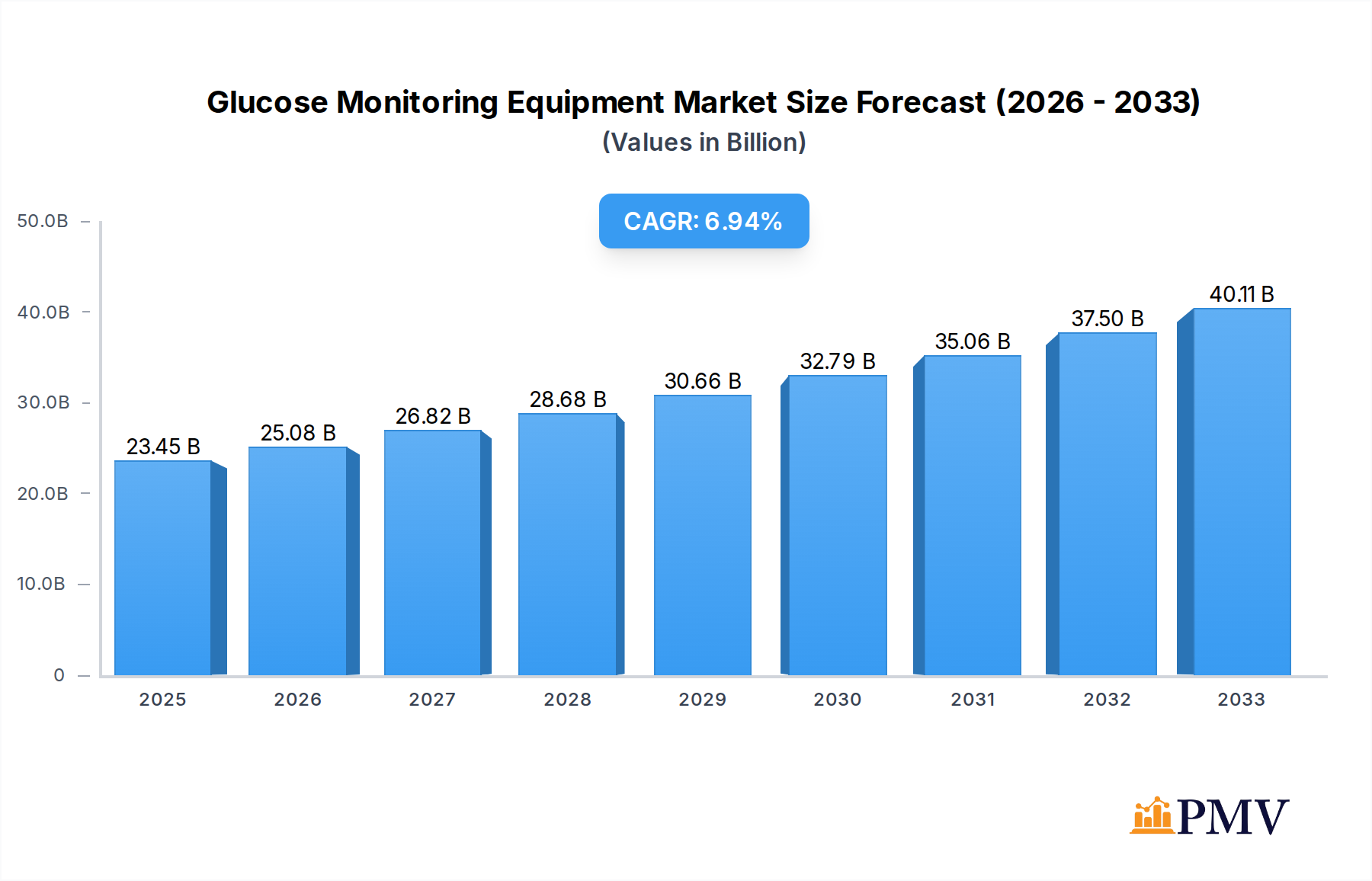

The global Glucose Monitoring Equipment market is poised for significant expansion, with a projected market size of $23.45 billion in 2025, driven by an impressive compound annual growth rate (CAGR) of 10.75%. This robust growth is fueled by an increasing prevalence of diabetes worldwide, a growing awareness among patients and healthcare providers regarding the importance of proactive glucose management, and advancements in technology leading to more accurate, user-friendly, and less invasive monitoring solutions. The rising adoption of Continuous Glucose Monitoring (CGM) systems, particularly among Type 1 diabetes patients and increasingly for Type 2 management, is a major catalyst. Furthermore, the expanding geriatric population, which is more susceptible to chronic conditions like diabetes, and the growing demand for home-based healthcare solutions are contributing to market dynamism. The market is segmented by application, including Child, Adult, and Elderly, with adults representing the largest segment due to the widespread diagnosis of diabetes in this demographic. By type, minimally invasive and non-invasive devices are gaining traction, with a strong preference shifting towards less painful and more convenient options.

Glucose Monitoring Equipment Market Size (In Billion)

The market's trajectory is further supported by key trends such as the integration of glucose monitoring devices with smartphones and other connected health platforms, enabling seamless data sharing and remote patient monitoring. This interconnectivity empowers individuals to better manage their condition and facilitates proactive interventions by healthcare professionals. The ongoing research and development efforts aimed at improving sensor accuracy, extending wear time, and reducing the cost of these devices are also expected to accelerate market penetration. While the market presents substantial opportunities, certain restraints, such as the high cost of advanced monitoring systems, reimbursement challenges in some regions, and the need for ongoing patient education and training, need to be addressed to fully unlock its potential. However, the sustained focus on innovation by leading companies like Dexcom, Abbott Laboratories, and Medtronic, coupled with supportive government initiatives and increasing healthcare expenditure globally, paints a very positive outlook for the glucose monitoring equipment market in the coming years.

Glucose Monitoring Equipment Company Market Share

This in-depth market research report provides an exhaustive analysis of the global Glucose Monitoring Equipment market, covering the historical period from 2019 to 2024, the base year of 2025, and a detailed forecast extending from 2025 to 2033. The report aims to equip industry stakeholders, including manufacturers, investors, researchers, and healthcare providers, with actionable insights and strategic guidance to navigate the evolving landscape of diabetes management technology. With an estimated market size projected to reach trillions by 2033, driven by an annual CAGR of XX%, this report delves into the intricacies of market structure, competitive dynamics, emerging trends, dominant segments, product innovations, and key growth drivers.

Glucose Monitoring Equipment Market Structure & Competitive Dynamics

The global Glucose Monitoring Equipment market exhibits a dynamic and evolving structure, characterized by a blend of established giants and innovative disruptors. Market concentration is moderately high, with key players like Dexcom, Abbott Laboratories, and Medtronic holding significant market shares, estimated to be in the billions of dollars. However, the emergence of specialized companies such as Senseonics Holdings, GlySens Incorporated, and Taiwan Biophotonic is fostering a competitive ecosystem driven by technological advancements. Innovation thrives through robust R&D investments, evidenced by the billions invested annually in developing next-generation continuous glucose monitoring (CGM) systems and non-invasive technologies. Regulatory frameworks, governed by bodies like the FDA and EMA, play a crucial role in shaping market entry and product approvals, often requiring billions in compliance costs. The threat of product substitutes, primarily traditional blood glucose meters, is diminishing as CGM adoption accelerates. End-user trends are strongly influenced by the increasing prevalence of diabetes and a growing demand for convenient, accurate, and real-time glucose data. Mergers and acquisition (M&A) activities are a prominent feature, with several billion-dollar deals recorded in recent years, as larger companies seek to acquire innovative technologies and expand their product portfolios. For instance, the acquisition of San Meditech by an undisclosed entity for an estimated billions highlights strategic consolidation.

Glucose Monitoring Equipment Industry Trends & Insights

The Glucose Monitoring Equipment industry is experiencing a paradigm shift, driven by a confluence of technological advancements, increasing diabetes prevalence, and evolving patient expectations. The market is poised for substantial growth, with an estimated market size projected to reach billions by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This expansion is fueled by several key growth drivers. Firstly, the escalating global incidence of diabetes, both type 1 and type 2, is creating an ever-increasing demand for effective glucose management solutions. The growing awareness among patients and healthcare professionals about the benefits of proactive diabetes management, including reduced long-term complications, further propels market adoption.

Technological disruptions are at the forefront of this evolution. Continuous Glucose Monitoring (CGM) systems have revolutionized diabetes care, offering real-time glucose readings, trend arrows, and alerts that empower individuals to make informed decisions. The transition from minimally invasive sensor technologies to more advanced, longer-wear, and less intrusive designs is a significant trend. Furthermore, significant investments, in the billions of dollars, are being poured into research and development for truly non-invasive glucose monitoring technologies, which, if successful, could represent a disruptive innovation, potentially impacting billions of lives. The integration of artificial intelligence (AI) and machine learning (ML) into glucose monitoring platforms is also gaining traction. These technologies are enabling personalized insights, predictive analytics for glycemic events, and enhanced data management, leading to improved patient outcomes and reduced healthcare burdens, potentially saving billions in treatment costs.

Consumer preferences are shifting towards user-friendly, connected devices that seamlessly integrate with smartphones and other wearable technologies. Patients are actively seeking solutions that offer greater convenience, accuracy, and a reduced need for frequent finger pricks. This demand is driving innovation in areas like Bluetooth connectivity, mobile applications for data analysis, and remote patient monitoring capabilities. The competitive landscape is intensifying, with existing players expanding their product offerings and new entrants vying for market share through innovative solutions. Strategic partnerships and collaborations are becoming increasingly common as companies aim to leverage each other's expertise and accelerate product development and market penetration. The market penetration of advanced CGM devices is projected to increase significantly, moving from a current estimate of XX% to XX% by 2033, signifying a major shift in diabetes management practices. The overall market revenue is expected to climb from billions in the historical period to billions by the estimated year of 2025, underscoring the substantial growth trajectory.

Dominant Markets & Segments in Glucose Monitoring Equipment

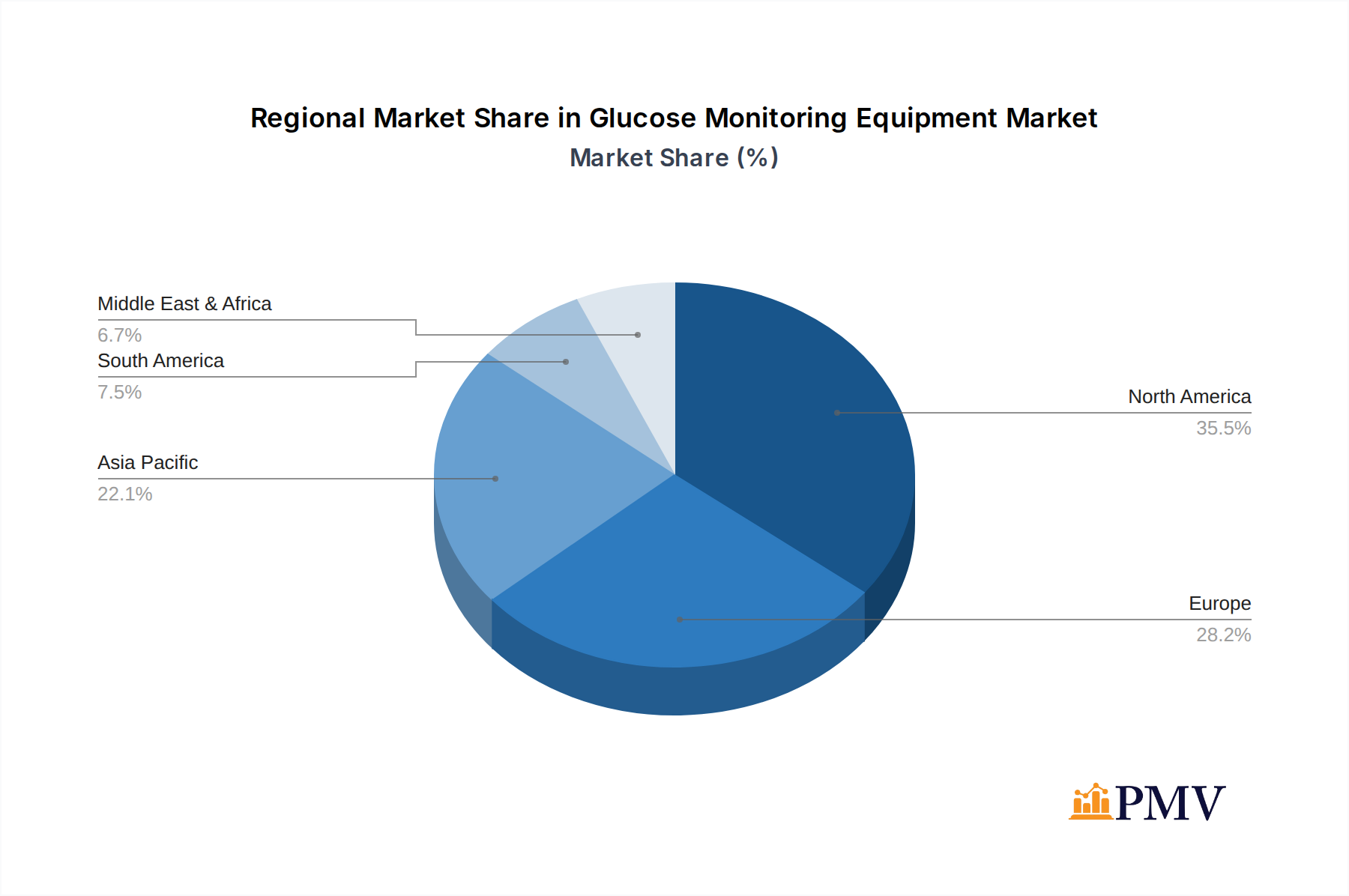

The global Glucose Monitoring Equipment market's dominance is intricately linked to regional economic strength, healthcare infrastructure, and patient demographics. Geographically, North America, particularly the United States, currently commands the largest market share, driven by high disposable incomes, advanced healthcare systems, and a high prevalence of diabetes. Government initiatives and robust insurance coverage for diabetes management devices further bolster this dominance, contributing billions to market value. The European region, with countries like Germany, the UK, and France, follows closely, propelled by similar factors and a strong emphasis on public health initiatives. Asia-Pacific is emerging as a high-growth region, fueled by a burgeoning middle class, increasing awareness of diabetes, and significant investments in healthcare infrastructure, with countries like China and India projected to contribute billions in market revenue.

Within the application segment, the Adult population represents the largest and most influential segment. This is attributed to the higher prevalence of type 2 diabetes in adults, coupled with an increased understanding and proactive approach to managing the condition. The adult segment is estimated to contribute billions to the overall market value. The Elderly segment, while also significant due to age-related comorbidities and the prevalence of diabetes, presents unique challenges and opportunities. The demand for user-friendly, intuitive devices is paramount, and the segment's growth is projected to be substantial, reaching billions by 2033. The Child segment, though smaller in absolute terms, is characterized by high growth potential due to the increasing incidence of pediatric diabetes and the long-term implications of early and effective management. Innovations tailored for children, such as discreet and easy-to-use sensors, are crucial for this segment, with market projections indicating growth into the billions.

In terms of product types, the Minimally Invasive segment, primarily encompassing Continuous Glucose Monitoring (CGM) systems, currently dominates the market. The accuracy, convenience, and real-time data offered by these systems have led to widespread adoption among individuals seeking better glycemic control. The global market for minimally invasive devices is expected to reach billions by 2033. However, the Non-invasive segment holds immense future potential. While still in developmental stages for widespread commercialization, the promise of a truly non-invasive glucose monitoring solution, eliminating the need for any skin penetration, is a disruptive force that could reshape the entire market, potentially impacting billions of users and driving market value into the hundreds of billions. Key drivers for the dominance of minimally invasive technologies include technological advancements in sensor accuracy and longevity, supportive reimbursement policies amounting to billions, and extensive clinical validation. The increasing preference for integrated diabetes management ecosystems, comprising glucose monitors, insulin pumps, and data analytics platforms, further solidifies the position of advanced monitoring solutions.

Glucose Monitoring Equipment Product Innovations

Recent product innovations in glucose monitoring equipment are centered on enhancing accuracy, patient comfort, and data connectivity. Companies are investing billions in developing next-generation Continuous Glucose Monitoring (CGM) sensors with extended wear times, reduced calibration needs, and improved accuracy across the glycemic spectrum. The integration of advanced algorithms, often powered by AI, is enabling predictive alerts for hypo- and hyperglycemia, proactively safeguarding patient health. Furthermore, there's a significant push towards miniaturization and discreet sensor designs, particularly for pediatric and adolescent users, making monitoring less obtrusive. The competitive advantage lies in seamless smartphone integration, cloud-based data sharing for remote monitoring by healthcare providers, and user-friendly mobile applications that translate complex data into actionable insights, ultimately aiming to improve patient outcomes and reduce healthcare costs, potentially saving billions annually.

Report Segmentation & Scope

This comprehensive report segments the Glucose Monitoring Equipment market to provide granular insights into its diverse landscape. The Application segmentation includes: Child, Adult, and Elderly populations. The Child segment, while a smaller portion of the current market, exhibits high growth projections due to the rising incidence of pediatric diabetes, with an estimated market size of billions by 2033 and a projected CAGR of XX%. The Adult segment, currently the largest, is expected to reach billions in market value by 2033, driven by the high prevalence of type 2 diabetes and widespread adoption of advanced monitoring technologies. The Elderly segment, valued at billions in 2025, is also projected for significant growth, driven by age-related diabetes and the need for user-friendly devices.

The Types segmentation encompasses: Minimally Invasive and Non-invasive technologies. The Minimally Invasive segment, dominated by CGM devices, is forecast to reach billions by 2033, driven by technological advancements and reimbursement policies. The Non-invasive segment, while in its nascent stages, holds transformative potential. Its market size is projected to grow exponentially from a smaller base, reaching billions by 2033, as breakthroughs in sensor technology materialize.

Key Drivers of Glucose Monitoring Equipment Growth

The growth of the Glucose Monitoring Equipment market is propelled by a multifaceted interplay of technological, economic, and regulatory factors. Technologically, the continuous evolution of Continuous Glucose Monitoring (CGM) systems, offering unparalleled accuracy, real-time data, and trend analysis, is a primary driver. Billions are invested in R&D to enhance sensor longevity, reduce invasiveness, and improve user experience. Economically, the rising global prevalence of diabetes, a condition affecting billions worldwide, creates an ever-expanding demand for effective management tools. Increased disposable income in emerging economies and supportive reimbursement policies, which account for billions in healthcare spending, further facilitate market access. Regulatory bodies, by streamlining approval processes for innovative devices, also play a crucial role in accelerating market penetration. The pursuit of improved patient outcomes and reduced long-term diabetes-related complications is a significant societal imperative, driving demand for advanced monitoring solutions, projected to save billions in healthcare costs annually.

Challenges in the Glucose Monitoring Equipment Sector

Despite its robust growth, the Glucose Monitoring Equipment sector faces several significant challenges that could impede its full potential. Regulatory hurdles, particularly for novel non-invasive technologies, can be extensive and costly, requiring billions in clinical trials and approvals. The high cost of advanced CGM devices can be a barrier to adoption for a substantial portion of the population, especially in regions with limited insurance coverage. Supply chain disruptions, as evidenced in recent years, can impact the availability of critical components and finished products, potentially affecting billions of users reliant on these devices. Furthermore, the competitive pressure from established players and emerging innovators necessitates continuous investment in R&D and marketing, adding billions to operational expenses. The lack of universal standardization in data formats and interoperability between different devices and platforms also presents a challenge, hindering seamless integration into broader healthcare ecosystems, potentially costing billions in lost efficiency.

Leading Players in the Glucose Monitoring Equipment Market

- Dexcom

- Abbott Laboratories

- Medtronic

- Senseonics Holdings

- GlySens Incorporated

- San Meditech

- Cnoga Medical

- Integrity Applications

- MediWise

- Meiqi Medical Equipment

- Taiwan Biophotonic

Key Developments in Glucose Monitoring Equipment Sector

- 2023: Dexcom launched its G7 CGM system, offering improved accuracy and a smaller, more discreet design.

- 2023: Abbott Laboratories received FDA clearance for its FreeStyle Libre 3 system, further enhancing connectivity and data accuracy.

- 2022: Medtronic advanced its next-generation CGM technology with a focus on enhanced integration with insulin delivery systems.

- 2022: Senseonics Holdings continued to expand the market reach of its Eversense continuous glucose monitoring system.

- 2021: GlySens Incorporated made significant progress in its development of long-term implantable glucose sensors.

- 2020: Taiwan Biophotonic unveiled novel optical sensing technologies for potential non-invasive glucose monitoring.

- 2020: San Meditech focused on developing cost-effective and accessible glucose monitoring solutions for emerging markets.

- 2019: Integrity Applications launched its GlucoTrack™ non-invasive glucose monitoring device for the consumer market.

- 2019: MediWise continued its research into advanced biosensor technology for glucose monitoring.

- 2019: Meiqi Medical Equipment expanded its portfolio of diabetes management devices, including glucose meters.

Strategic Glucose Monitoring Equipment Market Outlook

The strategic outlook for the Glucose Monitoring Equipment market is exceptionally positive, driven by sustained innovation and increasing global demand for proactive diabetes management. Key growth accelerators include the continued advancement of CGM technology towards greater accuracy, longer wear times, and reduced invasiveness, coupled with the potential breakthrough of truly non-invasive monitoring. The increasing adoption of integrated diabetes management platforms, leveraging AI and cloud connectivity for personalized insights and remote patient monitoring, presents a significant strategic opportunity. Furthermore, the expanding market penetration in emerging economies, supported by rising healthcare expenditure and government initiatives, offers substantial growth potential, estimated to contribute billions in future revenue. Companies that focus on user-centric design, robust data analytics, and strategic partnerships are well-positioned to capture market share and drive the future of diabetes care, ultimately improving the lives of billions.

Glucose Monitoring Equipment Segmentation

-

1. Application

- 1.1. Child

- 1.2. Adult

- 1.3. Elderly

-

2. Types

- 2.1. Minimally Invasive

- 2.2. Non-invasive

Glucose Monitoring Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Glucose Monitoring Equipment Regional Market Share

Geographic Coverage of Glucose Monitoring Equipment

Glucose Monitoring Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Child

- 5.1.2. Adult

- 5.1.3. Elderly

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Minimally Invasive

- 5.2.2. Non-invasive

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Child

- 6.1.2. Adult

- 6.1.3. Elderly

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Minimally Invasive

- 6.2.2. Non-invasive

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Child

- 7.1.2. Adult

- 7.1.3. Elderly

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Minimally Invasive

- 7.2.2. Non-invasive

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Child

- 8.1.2. Adult

- 8.1.3. Elderly

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Minimally Invasive

- 8.2.2. Non-invasive

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Child

- 9.1.2. Adult

- 9.1.3. Elderly

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Minimally Invasive

- 9.2.2. Non-invasive

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Glucose Monitoring Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Child

- 10.1.2. Adult

- 10.1.3. Elderly

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Minimally Invasive

- 10.2.2. Non-invasive

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Dexcom

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Abbott Laboratories

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Medtronic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Senseonics Holdings

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 GlySens Incorporated

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 San Meditech

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cnoga Medical

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Integrity Applications

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MediWise

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Meiqi Medical Equipment

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Taiwan Biophotonic

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Dexcom

List of Figures

- Figure 1: Global Glucose Monitoring Equipment Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Glucose Monitoring Equipment Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Glucose Monitoring Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Glucose Monitoring Equipment Volume (K), by Application 2025 & 2033

- Figure 5: North America Glucose Monitoring Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Glucose Monitoring Equipment Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Glucose Monitoring Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Glucose Monitoring Equipment Volume (K), by Types 2025 & 2033

- Figure 9: North America Glucose Monitoring Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Glucose Monitoring Equipment Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Glucose Monitoring Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Glucose Monitoring Equipment Volume (K), by Country 2025 & 2033

- Figure 13: North America Glucose Monitoring Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Glucose Monitoring Equipment Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Glucose Monitoring Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Glucose Monitoring Equipment Volume (K), by Application 2025 & 2033

- Figure 17: South America Glucose Monitoring Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Glucose Monitoring Equipment Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Glucose Monitoring Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Glucose Monitoring Equipment Volume (K), by Types 2025 & 2033

- Figure 21: South America Glucose Monitoring Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Glucose Monitoring Equipment Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Glucose Monitoring Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Glucose Monitoring Equipment Volume (K), by Country 2025 & 2033

- Figure 25: South America Glucose Monitoring Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Glucose Monitoring Equipment Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Glucose Monitoring Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Glucose Monitoring Equipment Volume (K), by Application 2025 & 2033

- Figure 29: Europe Glucose Monitoring Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Glucose Monitoring Equipment Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Glucose Monitoring Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Glucose Monitoring Equipment Volume (K), by Types 2025 & 2033

- Figure 33: Europe Glucose Monitoring Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Glucose Monitoring Equipment Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Glucose Monitoring Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Glucose Monitoring Equipment Volume (K), by Country 2025 & 2033

- Figure 37: Europe Glucose Monitoring Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Glucose Monitoring Equipment Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Glucose Monitoring Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Glucose Monitoring Equipment Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Glucose Monitoring Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Glucose Monitoring Equipment Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Glucose Monitoring Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Glucose Monitoring Equipment Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Glucose Monitoring Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Glucose Monitoring Equipment Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Glucose Monitoring Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Glucose Monitoring Equipment Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Glucose Monitoring Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Glucose Monitoring Equipment Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Glucose Monitoring Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Glucose Monitoring Equipment Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Glucose Monitoring Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Glucose Monitoring Equipment Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Glucose Monitoring Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Glucose Monitoring Equipment Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Glucose Monitoring Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Glucose Monitoring Equipment Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Glucose Monitoring Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Glucose Monitoring Equipment Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Glucose Monitoring Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Glucose Monitoring Equipment Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Glucose Monitoring Equipment Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Glucose Monitoring Equipment Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Glucose Monitoring Equipment Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Glucose Monitoring Equipment Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Glucose Monitoring Equipment Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Glucose Monitoring Equipment Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Glucose Monitoring Equipment Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Glucose Monitoring Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Glucose Monitoring Equipment Volume K Forecast, by Country 2020 & 2033

- Table 79: China Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Glucose Monitoring Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Glucose Monitoring Equipment Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Glucose Monitoring Equipment?

The projected CAGR is approximately 10.75%.

2. Which companies are prominent players in the Glucose Monitoring Equipment?

Key companies in the market include Dexcom, Abbott Laboratories, Medtronic, Senseonics Holdings, GlySens Incorporated, San Meditech, Cnoga Medical, Integrity Applications, MediWise, Meiqi Medical Equipment, Taiwan Biophotonic.

3. What are the main segments of the Glucose Monitoring Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Glucose Monitoring Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Glucose Monitoring Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Glucose Monitoring Equipment?

To stay informed about further developments, trends, and reports in the Glucose Monitoring Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence