Key Insights

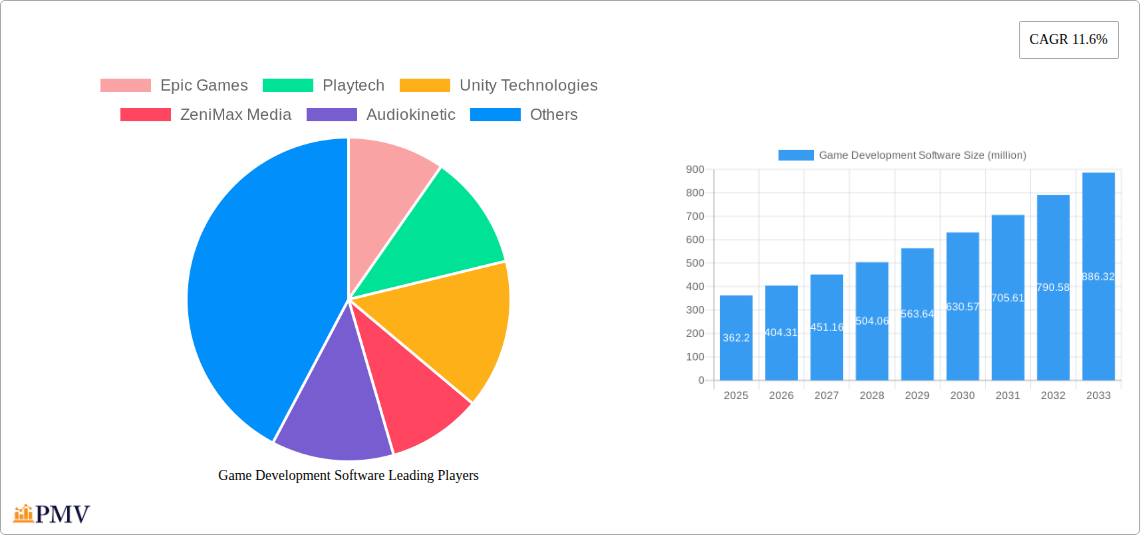

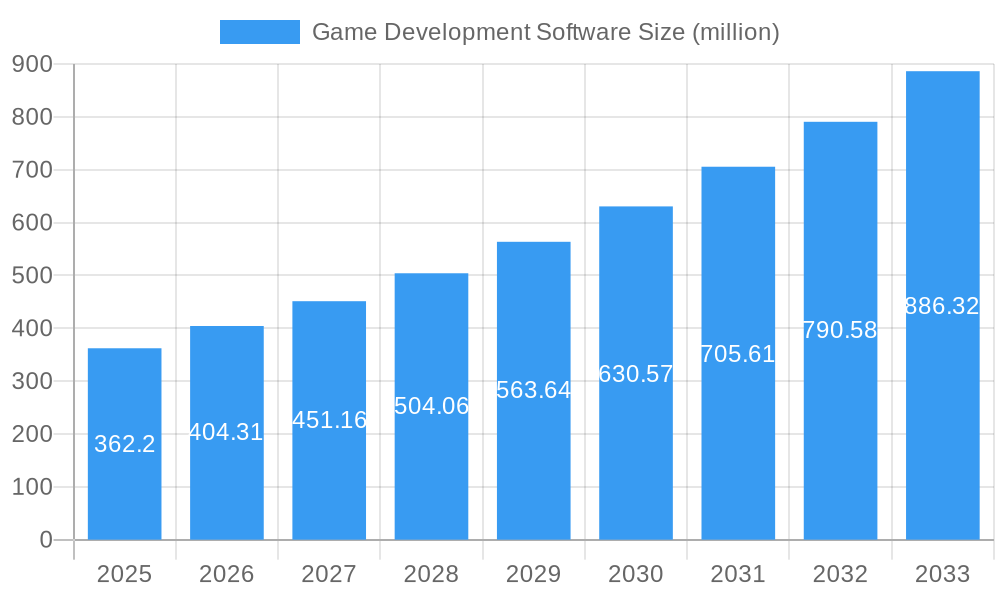

The global Game Development Software market is poised for robust expansion, projected to reach a significant valuation of 362.2 million USD by 2025, driven by an impressive 11.6% CAGR. This sustained growth is fueled by several dynamic factors, primarily the increasing demand for sophisticated and immersive gaming experiences across diverse platforms. The proliferation of mobile gaming, the growing popularity of esports, and the continuous evolution of virtual and augmented reality technologies are creating a fertile ground for game development software. Furthermore, the democratization of game creation tools, making them more accessible to independent developers and smaller studios, is also a significant catalyst. The rise of cross-platform development capabilities inherent in many modern game engines is further expanding the reach and appeal of these software solutions. Key applications within this market include Android and iOS, reflecting the dominance of mobile gaming, alongside PCs, catering to hardcore gamers and professional development.

Game Development Software Market Size (In Million)

The market's trajectory is further shaped by emerging trends such as the integration of AI and machine learning for streamlined game asset creation and AI-driven gameplay mechanics. The growing adoption of cloud-based development platforms is also enhancing collaboration and efficiency for development teams. While the market is buoyant, certain restraints could influence its pace. These include the high cost of advanced development tools for some smaller entities and the ever-present need for specialized skill sets in game development. However, the overall outlook remains exceptionally positive, with segments like GameMaker, Pygame, and Java expected to see substantial uptake, alongside established giants like C++. Leading companies such as Epic Games, Unity Technologies, and Playtech are at the forefront of innovation, continually pushing the boundaries of what's possible in game creation, ensuring a dynamic and competitive landscape for the foreseeable future.

Game Development Software Company Market Share

Here is an SEO-optimized, detailed report description for Game Development Software, incorporating your specified keywords, structure, and content requirements.

This in-depth game development software market report provides a comprehensive analysis of the global landscape, offering critical insights for stakeholders seeking to understand the game engine market, game development tools, and game creation software industry. Covering the historical period from 2019 to 2024, the base year of 2025, and a robust forecast period extending to 2033, this study details market structures, competitive dynamics, emerging trends, and strategic outlooks. Leveraging extensive data and expert analysis, the report delves into key segments such as game development applications for Android, iOS, PCs, and other platforms, alongside dominant game development languages like C++, Java, and frameworks like GameMaker and Pygame. With an estimated market size projected to reach millions by 2025, this report is an indispensable resource for game developers, game studios, independent game developers, and game publishers.

Game Development Software Market Structure & Competitive Dynamics

The game development software market exhibits a dynamic and evolving structure characterized by both concentrated innovation and a growing ecosystem of independent developers. Major players like Epic Games, Unity Technologies, and Playtech command significant market share, driven by advanced game engine technology and comprehensive game development platforms. Innovation is fueled by continuous advancements in graphics rendering, artificial intelligence, and cross-platform compatibility, fostering an environment where technological superiority is a key differentiator. Regulatory frameworks, while generally supportive of the industry, can introduce complexities related to intellectual property and data privacy. Product substitutes, such as no-code/low-code game creation tools, are emerging to democratize game development, appealing to a broader user base. End-user trends, including the rise of mobile gaming, cloud gaming, and the metaverse, are profoundly influencing demand for flexible and powerful game development solutions. Mergers and acquisitions (M&A) activity, with significant deal values in the tens of millions, continues to shape the competitive landscape, as larger entities seek to acquire innovative technologies or expand their market reach. The market concentration is moderate, with a healthy balance between established giants and a vibrant community of smaller studios leveraging specialized game development tools.

Game Development Software Industry Trends & Insights

The game development software industry is experiencing unprecedented growth, driven by a confluence of technological advancements, shifting consumer preferences, and expanding market opportunities. The Compound Annual Growth Rate (CAGR) is projected to be in the double digits, indicating robust expansion throughout the forecast period. Technological disruptions, including the integration of artificial intelligence (AI) for procedural content generation and enhanced gameplay, the widespread adoption of cloud-based game development environments, and the increasing sophistication of Virtual Reality (VR) and Augmented Reality (AR) capabilities, are revolutionizing how games are created and experienced. Consumer preferences are increasingly leaning towards immersive, interactive, and socially connected gaming experiences across all platforms, from mobile devices to high-end PCs. This surge in demand for diverse gaming content necessitates more efficient and accessible game creation tools. The competitive dynamics are intensifying, with companies constantly innovating to offer superior game engines, advanced game development frameworks, and more intuitive game development platforms. Market penetration for specialized game development software is expanding as independent developers gain access to powerful tools previously exclusive to large studios. The growth drivers include the explosive popularity of esports, the continuous evolution of the mobile gaming market, and the increasing investment in the metaverse and decentralized gaming experiences. The demand for cross-platform development capabilities is also a significant trend, enabling developers to reach wider audiences with a single codebase and toolset.

Dominant Markets & Segments in Game Development Software

The game development software market showcases distinct regional and segmental dominance, crucial for strategic market entry and expansion. The PC game development segment continues to be a powerhouse, fueled by sophisticated hardware capabilities and a large, engaged player base willing to invest in AAA titles and high-fidelity experiences. PC game development software often features the most advanced rendering engines, physics simulations, and complex scripting capabilities. Furthermore, Android game development and iOS game development represent colossal and rapidly growing segments, driven by the ubiquitous nature of smartphones and tablets, and the ever-increasing demand for accessible and engaging mobile games. This segment benefits from widespread adoption of mobile-first game development tools and optimized frameworks for touch-based interfaces. The "Other" application segment, encompassing consoles and emerging platforms like VR/AR headsets, also presents significant growth potential, albeit with specialized development requirements.

Within the game development software types, C++ remains a cornerstone for performance-critical game development, powering most AAA titles due to its efficiency and control. Java continues to be relevant, particularly in certain mobile and cross-platform development scenarios. GameMaker and Pygame represent accessible and powerful options for indie developers and educational purposes, fostering rapid prototyping and learning. Key drivers for the dominance of PC and mobile segments include robust economic policies supporting the technology sector, well-developed digital distribution infrastructure, and widespread internet penetration. Government initiatives promoting digital content creation and technological innovation also play a vital role. The sheer volume of users on these platforms, coupled with the monetization models prevalent in each, solidify their leadership. For instance, the substantial revenue generated through in-app purchases and subscriptions in mobile gaming directly fuels demand for specialized game development software for these platforms. Similarly, the PC market thrives on premium game sales and digital distribution platforms like Steam, which rely heavily on advanced game development engines.

Game Development Software Product Innovations

Recent game development software innovations focus on enhancing developer efficiency, expanding creative possibilities, and democratizing access to powerful tools. Advancements in real-time rendering, AI-driven asset creation, and integrated cloud collaboration are key. These developments provide competitive advantages by enabling faster iteration cycles, richer visual fidelity, and more complex gameplay mechanics. Market fit is being optimized through modular game engine designs and adaptable game development frameworks that cater to diverse project scopes, from hyper-casual mobile games to expansive open-world experiences.

Report Segmentation & Scope

This report meticulously segments the game development software market by Application and Type.

- Application: The market is analyzed across Android, iOS, PCs, and Other platforms. Each segment is projected to witness substantial growth, with PCs and mobile platforms (Android, iOS) expected to maintain their leading positions, driven by distinct user bases and monetization strategies. The "Other" category, encompassing consoles and emerging XR devices, is poised for significant expansion.

- Types: Segmentation includes GameMaker, Pygame, Java, C++, and Other programming languages and frameworks. C++ is anticipated to dominate the high-end development space, while Java will retain its importance in mobile and cross-platform applications. GameMaker and Pygame will continue to be crucial for indie developers and educational markets.

Key Drivers of Game Development Software Growth

Several key factors are propelling the growth of the game development software market. Technological advancements, including AI integration for content creation and procedural generation, are making development more efficient and innovative. The escalating demand for engaging mobile games and the expanding reach of PC gaming are significant economic drivers. Furthermore, government support for the digital creative industries and the burgeoning interest in cloud gaming and the metaverse are creating new avenues for expansion. The increasing accessibility of powerful game development tools to independent creators also contributes significantly to market expansion.

Challenges in the Game Development Software Sector

Despite robust growth, the game development software sector faces several challenges. Regulatory hurdles, particularly concerning data privacy and content moderation across global markets, can impede development and distribution. Supply chain issues, though less prevalent for software compared to hardware, can impact the availability of development resources and tools. Intense competitive pressures among established game engine providers and emerging game creation platforms necessitate continuous innovation and significant investment. Furthermore, the high cost of AAA game development and the increasing complexity of game design present barriers for smaller studios.

Leading Players in the Game Development Software Market

- Epic Games

- Playtech

- Unity Technologies

- ZeniMax Media

- Audiokinetic

Key Developments in Game Development Software Sector

- 2023 September: Unity Technologies announces major updates to its engine, focusing on real-time rendering and AI integration.

- 2023 October: Epic Games releases new features for Unreal Engine 5, enhancing virtual production capabilities.

- 2024 January: Playtech expands its portfolio with the acquisition of a prominent indie game studio, strengthening its content offerings.

- 2024 February: ZeniMax Media demonstrates new AI tools for character animation within its proprietary game development pipeline.

- 2024 March: Audiokinetic introduces advancements in its middleware for immersive audio experiences in games.

Strategic Game Development Software Market Outlook

The strategic outlook for the game development software market is exceptionally bright, fueled by the persistent demand for innovative gaming experiences and the ongoing digital transformation. Growth accelerators include the continued rise of the creator economy, the increasing adoption of cloud-native game development solutions, and the exploration of new monetization models within decentralized gaming environments. The metaverse and extended reality (XR) technologies represent significant future potential, requiring sophisticated game creation software to realize their full interactive capabilities. Companies that can offer flexible, powerful, and accessible game development platforms will be best positioned to capitalize on these emerging opportunities.

Game Development Software Segmentation

-

1. Application

- 1.1. Android

- 1.2. IOS

- 1.3. PCs

- 1.4. Other

-

2. Types

- 2.1. GameMaker

- 2.2. Pygame

- 2.3. Java

- 2.4. C++

- 2.5. Other

Game Development Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

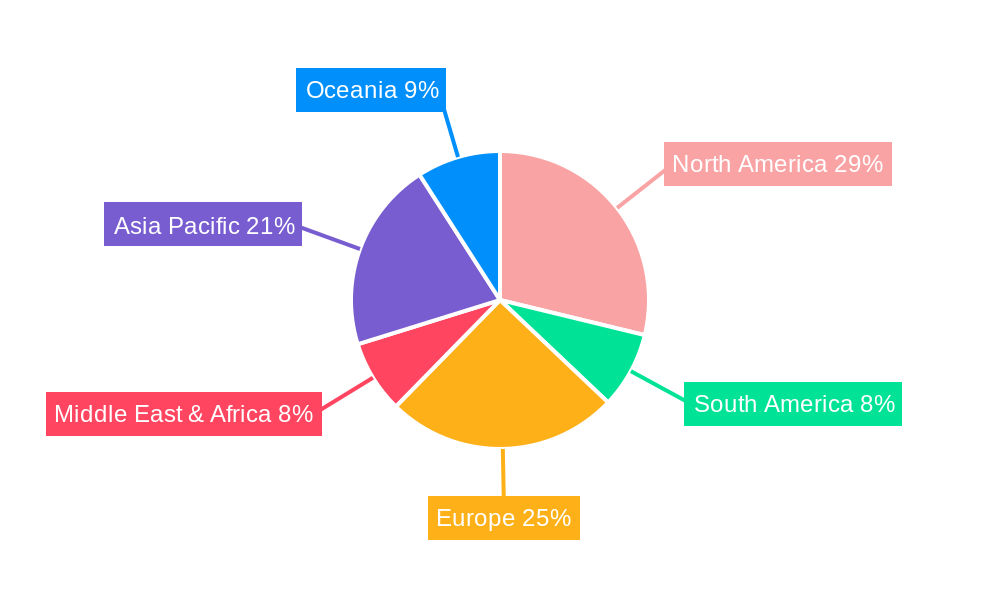

Game Development Software Regional Market Share

Geographic Coverage of Game Development Software

Game Development Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Game Development Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Android

- 5.1.2. IOS

- 5.1.3. PCs

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. GameMaker

- 5.2.2. Pygame

- 5.2.3. Java

- 5.2.4. C++

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Game Development Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Android

- 6.1.2. IOS

- 6.1.3. PCs

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. GameMaker

- 6.2.2. Pygame

- 6.2.3. Java

- 6.2.4. C++

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Game Development Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Android

- 7.1.2. IOS

- 7.1.3. PCs

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. GameMaker

- 7.2.2. Pygame

- 7.2.3. Java

- 7.2.4. C++

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Game Development Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Android

- 8.1.2. IOS

- 8.1.3. PCs

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. GameMaker

- 8.2.2. Pygame

- 8.2.3. Java

- 8.2.4. C++

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Game Development Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Android

- 9.1.2. IOS

- 9.1.3. PCs

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. GameMaker

- 9.2.2. Pygame

- 9.2.3. Java

- 9.2.4. C++

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Game Development Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Android

- 10.1.2. IOS

- 10.1.3. PCs

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. GameMaker

- 10.2.2. Pygame

- 10.2.3. Java

- 10.2.4. C++

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Epic Games

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Playtech

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Unity Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ZeniMax Media

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Audiokinetic

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.1 Epic Games

List of Figures

- Figure 1: Global Game Development Software Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Game Development Software Revenue (million), by Application 2025 & 2033

- Figure 3: North America Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Game Development Software Revenue (million), by Types 2025 & 2033

- Figure 5: North America Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Game Development Software Revenue (million), by Country 2025 & 2033

- Figure 7: North America Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Game Development Software Revenue (million), by Application 2025 & 2033

- Figure 9: South America Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Game Development Software Revenue (million), by Types 2025 & 2033

- Figure 11: South America Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Game Development Software Revenue (million), by Country 2025 & 2033

- Figure 13: South America Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Game Development Software Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Game Development Software Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Game Development Software Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Game Development Software Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Game Development Software Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Game Development Software Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Game Development Software Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Game Development Software Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Game Development Software Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Game Development Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Game Development Software Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Game Development Software Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Game Development Software Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Game Development Software Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Game Development Software Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Game Development Software Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Game Development Software Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Game Development Software Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Game Development Software Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Game Development Software?

The projected CAGR is approximately 11.6%.

2. Which companies are prominent players in the Game Development Software?

Key companies in the market include Epic Games, Playtech, Unity Technologies, ZeniMax Media, Audiokinetic.

3. What are the main segments of the Game Development Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 362.2 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Game Development Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Game Development Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Game Development Software?

To stay informed about further developments, trends, and reports in the Game Development Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence