Key Insights

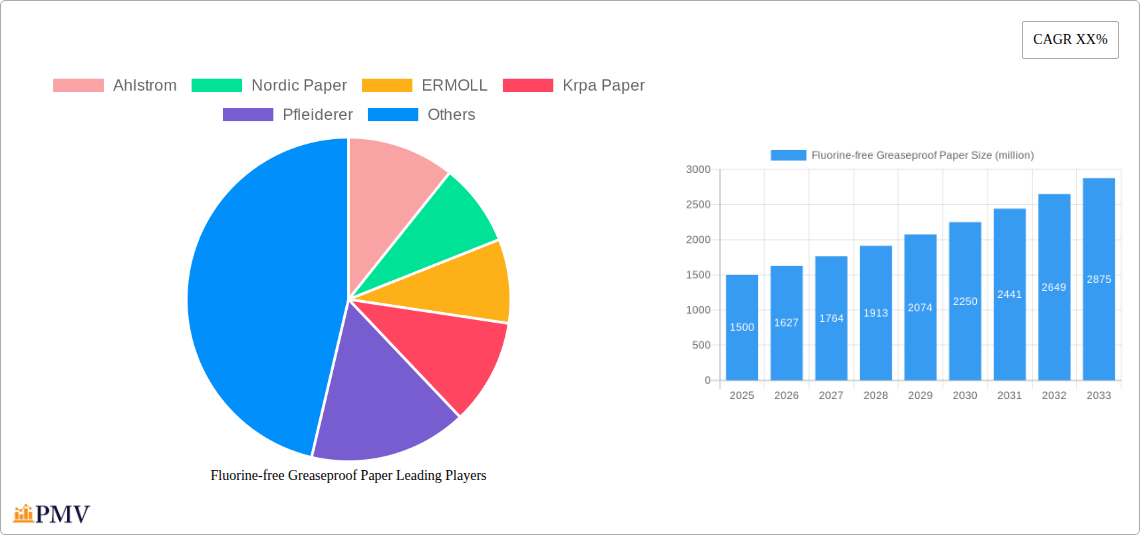

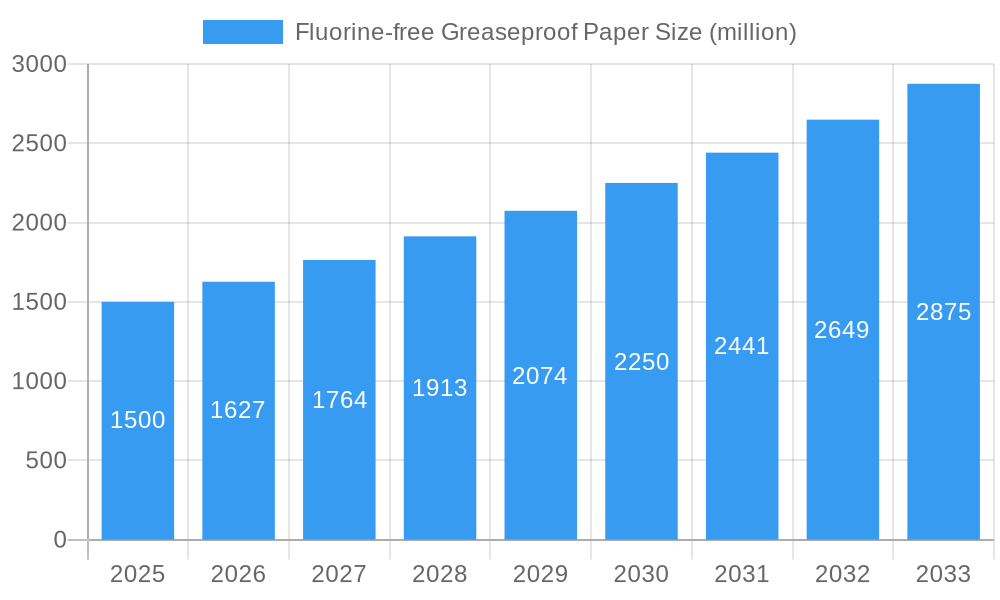

The global Fluorine-free Greaseproof Paper market is poised for significant expansion, projected to reach a substantial market size of approximately $1,500 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of around 8.5% anticipated throughout the forecast period from 2025 to 2033. This growth trajectory is primarily fueled by a confluence of escalating consumer demand for sustainable packaging solutions and increasingly stringent environmental regulations globally. The phasing out of per- and polyfluoroalkyl substances (PFAS) due to their persistent environmental impact is a critical driver, pushing manufacturers and end-users towards viable fluorine-free alternatives. Key applications such as bakery and fast-food restaurants are at the forefront of this adoption, owing to the direct contact of greaseproof paper with food products. The trend towards home cooking and baking also contributes to this demand, as consumers become more conscious of the materials used in their kitchens.

Fluorine-free Greaseproof Paper Market Size (In Billion)

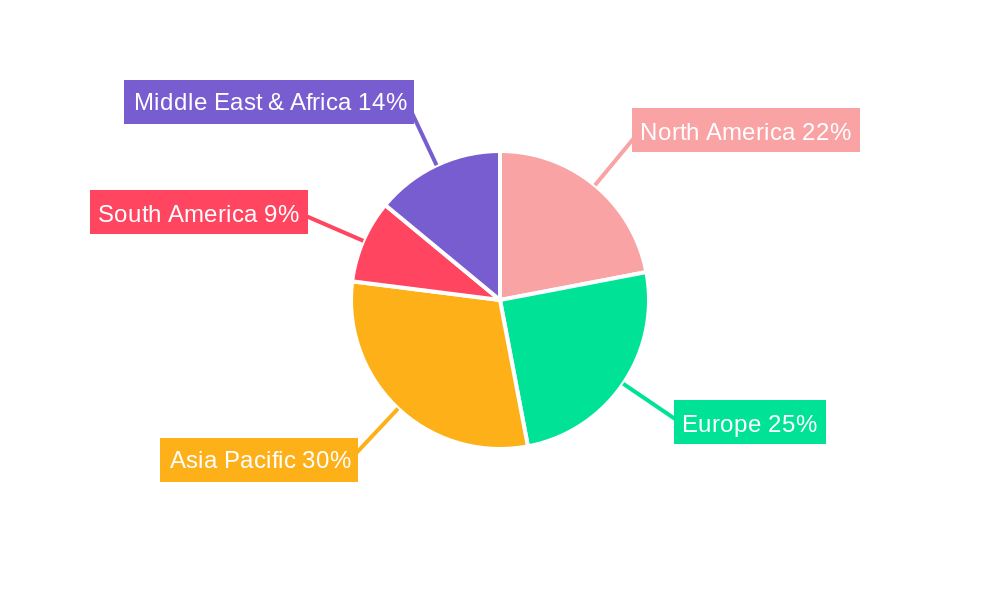

Several factors are shaping the market landscape, with a clear emphasis on innovation in material science and production processes. The development of advanced coatings and treatments that offer comparable or superior grease and moisture resistance to traditional PFAS-treated papers is a major trend. Furthermore, the increasing focus on recyclability and compostability of packaging materials aligns perfectly with the inherent benefits of fluorine-free greaseproof paper. However, the market does face certain restraints, including the initial higher cost of production for some advanced fluorine-free alternatives compared to conventional options, and the need for broader consumer and industry education to fully embrace these newer materials. Despite these challenges, the overwhelming drive towards eco-friendly solutions, coupled with technological advancements, positions the Fluorine-free Greaseproof Paper market for sustained and accelerated growth, with Asia Pacific and Europe expected to lead in terms of adoption and market value.

Fluorine-free Greaseproof Paper Company Market Share

Comprehensive Report: Fluorine-free Greaseproof Paper Market Analysis 2019-2033

This in-depth report provides a detailed examination of the global Fluorine-free Greaseproof Paper market, offering critical insights for stakeholders, manufacturers, and investors. Covering the historical period of 2019-2024, the base year of 2025, and a forecast period extending to 2033, this analysis delves into market dynamics, emerging trends, dominant segments, and future outlook. With a focus on high-ranking keywords such as "eco-friendly food packaging," "sustainable paper solutions," "PFAS-free greaseproof paper," and "biodegradable food wraps," this report aims to capture significant search visibility and engage industry professionals actively seeking alternatives to traditional fluorinated greaseproof papers. We analyze market structure, competitive landscapes, technological advancements, and consumer preferences, providing actionable intelligence for strategic decision-making.

Fluorine-free Greaseproof Paper Market Structure & Competitive Dynamics

The Fluorine-free Greaseproof Paper market is characterized by a moderate level of concentration, with key players investing heavily in research and development to innovate and differentiate their product offerings. The innovation ecosystem is driven by increasing environmental regulations and consumer demand for sustainable packaging solutions. Regulatory frameworks worldwide are becoming more stringent regarding the use of per- and polyfluoroalkyl substances (PFAS), directly fueling the growth of fluorine-free alternatives. Product substitutes, while present in the form of conventional greaseproof papers with potential coatings, are increasingly being phased out due to their environmental impact. End-user trends strongly favor bio-based and compostable materials, pushing manufacturers to develop high-performance, fluorine-free options. Merger and acquisition (M&A) activities are expected to increase as companies seek to expand their market reach and acquire proprietary technologies. Notable M&A deal values are projected to be in the range of several hundred million.

- Market Concentration: Moderate, with increasing fragmentation due to new entrants and niche product development.

- Innovation Ecosystem: Driven by sustainability mandates and technological advancements in paper treatment.

- Regulatory Frameworks: Strict regulations against PFAS are a primary market driver.

- Product Substitutes: Traditional greaseproof papers with varying degrees of effectiveness and environmental impact.

- End-User Trends: Strong preference for eco-friendly, compostable, and PFAS-free food packaging.

- M&A Activities: Expected to accelerate as companies seek market consolidation and technological integration. Projected M&A deal values are estimated to reach over 800 million.

Fluorine-free Greaseproof Paper Industry Trends & Insights

The global Fluorine-free Greaseproof Paper market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 9.5% during the forecast period of 2025-2033. This upward trajectory is significantly influenced by a confluence of market growth drivers, including heightened consumer awareness regarding the environmental and health implications of PFAS, coupled with increasingly stringent government regulations worldwide. The industry is witnessing remarkable technological disruptions, with advancements in paper manufacturing processes and the development of novel barrier coatings that deliver superior grease and moisture resistance without the use of harmful fluorine compounds. Consumer preferences are unequivocally shifting towards sustainable, compostable, and biodegradable packaging solutions, making fluorine-free greaseproof paper a preferred choice across various food service and retail applications. The competitive dynamics within the market are intensifying, with established paper manufacturers and new specialized companies vying for market share through product innovation, strategic partnerships, and market penetration efforts. Market penetration of fluorine-free alternatives is currently estimated at around 30% and is expected to rise significantly. The shift away from PFAS is not merely a trend but a fundamental change in the industry, driven by a collective global effort towards a circular economy and reduced environmental footprint. The demand for safe, effective, and environmentally responsible food packaging is creating unprecedented opportunities for fluorine-free greaseproof paper manufacturers. Innovations in cellulose-based materials and bio-derived coatings are further enhancing the performance characteristics of these papers, making them a viable and often superior alternative to traditional packaging. The increasing adoption in food packaging for baked goods, fast food, and convenience meals underscores the broad applicability and growing acceptance of these eco-friendly solutions. The market penetration in the bakery segment is projected to reach over 50% by 2033.

Dominant Markets & Segments in Fluorine-free Greaseproof Paper

The Bakery application segment is poised to dominate the Fluorine-free Greaseproof Paper market, driven by its extensive use in packaging a wide array of baked goods, from bread and pastries to cakes and cookies. This dominance is further propelled by the increasing demand for visually appealing and functional packaging that maintains product freshness and prevents grease stains, thereby enhancing consumer experience. The Natural Greaseproof Paper type is also expected to hold a significant market share, owing to its inherent biodegradability and compostability, aligning perfectly with the growing consumer preference for sustainable options. The economic policies that incentivize the use of eco-friendly materials and the robust infrastructure supporting sustainable packaging solutions in leading regions contribute to this segment's growth.

- Dominant Application Segment: Bakery

- Key Drivers:

- High volume usage in packaging diverse baked goods.

- Consumer demand for grease-resistant and aesthetically pleasing packaging.

- Growth of the artisanal and specialty bakery sector.

- Regulatory push for food-safe packaging.

- Key Drivers:

- Dominant Product Type: Natural Greaseproof Paper

- Key Drivers:

- Superior biodegradability and compostability credentials.

- Consumer preference for natural and plant-based materials.

- Increasing availability of advanced manufacturing techniques for natural greaseproof paper.

- Alignment with circular economy principles.

- Key Drivers:

Geographically, North America and Europe are anticipated to lead the market, primarily due to their proactive regulatory environments concerning PFAS and strong consumer demand for sustainable products. Stringent environmental regulations in these regions, coupled with government initiatives promoting green packaging, are significant growth accelerators. The well-established food service industry and widespread adoption of advanced packaging technologies further bolster their leading positions.

- Dominant Geographic Region: North America & Europe

- Key Drivers:

- Strict PFAS regulations and bans.

- High consumer awareness and willingness to pay for sustainable products.

- Developed food service and retail infrastructure.

- Government incentives and grants for eco-friendly packaging.

- Key Drivers:

The Fast Food Restaurant segment also presents substantial growth opportunities, as quick-service restaurants increasingly adopt sustainable packaging to align with corporate social responsibility goals and meet customer expectations. The Coated Greaseproof Paper type, while potentially having a slightly lower market share than natural variants due to advancements in natural barrier technologies, will still be a significant segment, particularly for applications requiring enhanced moisture resistance.

- Significant Application Segment: Fast Food Restaurant

- Key Drivers:

- Growing fast-food industry and demand for convenient packaging.

- Brand image enhancement through sustainable packaging adoption.

- Cost-effectiveness and performance of fluorine-free alternatives.

- Key Drivers:

- Significant Product Type: Coated Greaseproof Paper

- Key Drivers:

- Enhanced barrier properties for specific food types.

- Technological advancements in biodegradable coatings.

- Meeting performance requirements for high-volume food service.

- Key Drivers:

Fluorine-free Greaseproof Paper Product Innovations

Product innovations in the fluorine-free greaseproof paper sector are primarily focused on developing enhanced barrier properties against grease and moisture, while simultaneously improving biodegradability and compostability. Advances in bio-based coatings, such as those derived from plant starches and natural polymers, are enabling paper manufacturers to achieve performance levels comparable to or exceeding traditional fluorinated papers. These innovations are crucial for meeting the demands of diverse applications, from bakery packaging to fast-food wrappers. Competitive advantages are being gained through the development of papers with superior printability, heat sealability, and recyclability, further solidifying their position as a sustainable and high-performing alternative. The market is witnessing a trend towards specialized fluorine-free papers tailored for specific food types and cooking methods, such as microwaveable or oven-safe applications.

Report Segmentation & Scope

This report meticulously segments the Fluorine-free Greaseproof Paper market across key dimensions to provide a granular understanding of market dynamics. The Application segmentation includes Bakery, Fast Food Restaurant, Home Use, and Others, encompassing a wide spectrum of end-user industries. The Types segmentation focuses on Natural Greaseproof Paper and Coated Greaseproof Paper, highlighting the technological variations and their respective market penetration. Each segment is analyzed for its growth projections, estimated market sizes, and competitive dynamics, offering a comprehensive overview of opportunities and challenges within specific niches. The scope extends to analyzing global market sizes, regional trends, and the impact of evolving consumer preferences and regulatory landscapes on each segment. The estimated market size for the Bakery segment is over 1.2 billion.

- Application Segments: Detailed analysis of the Bakery, Fast Food Restaurant, Home Use, and Others segments, including their individual growth trajectories and market share projections.

- Types Segments: In-depth examination of Natural Greaseproof Paper and Coated Greaseproof Paper, assessing their market penetration, performance characteristics, and competitive landscape.

Key Drivers of Fluorine-free Greaseproof Paper Growth

The growth of the Fluorine-free Greaseproof Paper market is primarily propelled by a synergistic combination of technological, economic, and regulatory factors. Environmentally conscious consumerism is a significant economic driver, with a growing segment of the population actively seeking and willing to pay a premium for sustainable and PFAS-free food packaging. Economically, the development of cost-effective manufacturing processes for fluorine-free alternatives is making them increasingly competitive with traditional options. Regulatory mandates, such as bans and restrictions on PFAS in various countries and regions, are a critical catalyst, forcing manufacturers and food businesses to transition to safer alternatives. For instance, regulations in California and the European Union are creating a strong impetus for the adoption of these eco-friendly papers. Technological advancements in creating effective grease and moisture barriers using natural or bio-based materials are also crucial, enabling fluorine-free papers to meet high performance standards.

Challenges in the Fluorine-free Greaseproof Paper Sector

Despite its promising growth, the Fluorine-free Greaseproof Paper sector faces several challenges that could impede its rapid expansion. One significant challenge is the perception and reality of performance parity with traditional fluorinated papers, especially in demanding applications requiring extreme grease or heat resistance. Achieving comparable barrier properties consistently and cost-effectively remains an ongoing area of research and development. Supply chain issues, including the availability and cost of sustainable raw materials and specialized coating agents, can also present hurdles. Competitive pressures from established players offering traditional solutions and the inertia of long-standing supply contracts can slow down the adoption rate. Furthermore, the evolving regulatory landscape, while a driver, can also create uncertainty for manufacturers as new standards are introduced. The estimated cost increase for fluorine-free paper compared to conventional options is currently around 10-15%.

Leading Players in the Fluorine-free Greaseproof Paper Market

- Ahlstrom

- Nordic Paper

- ERMOLL

- Krpa Paper

- Pfleiderer

- Pudumjee Group

- Zhejiang Kaifeng New Material

- Qingdao Rongxin Industry and Trade

- Zhejiang Fulai New Materials

Key Developments in Fluorine-free Greaseproof Paper Sector

- 2023/Q4: Launch of new biodegradable coatings for enhanced grease resistance by Nordic Paper.

- 2024/Q1: ERMOLL expands production capacity for fluorine-free greaseproof paper to meet growing demand.

- 2024/Q2: Ahlstrom introduces a novel compostable greaseproof paper with superior oil barrier properties.

- 2024/Q3: Krpa Paper invests in advanced pulp treatment technologies to improve natural greaseproof paper performance.

- 2024/Q4: Pudumjee Group announces strategic partnerships to accelerate the adoption of PFAS-free packaging solutions.

- 2025/Q1: Zhejiang Kaifeng New Material unveils a new line of fluorine-free papers for direct food contact applications.

- 2025/Q2: Qingdao Rongxin Industry and Trade enhances its R&D focus on sustainable paper coatings.

- 2025/Q3: Zhejiang Fulai New Materials obtains key certifications for its eco-friendly greaseproof paper products.

Strategic Fluorine-free Greaseproof Paper Market Outlook

The strategic outlook for the Fluorine-free Greaseproof Paper market is overwhelmingly positive, driven by a robust combination of regulatory support, escalating consumer demand for sustainable products, and continuous technological innovation. Growth accelerators include the increasing global ban on PFAS substances, which will mandate a widespread transition to fluorine-free alternatives across the food packaging industry. The expanding quick-service restaurant (QSR) sector and the bakery industry, both significant consumers of greaseproof paper, are actively seeking eco-friendly packaging solutions to align with their sustainability goals and enhance brand reputation. Strategic opportunities lie in further developing high-performance, cost-competitive fluorine-free papers that offer superior grease, moisture, and heat resistance, thereby overcoming existing performance perceptions. Investment in advanced bio-based coatings and sustainable manufacturing processes will be crucial for market leaders. The projected market size for fluorine-free greaseproof paper is estimated to exceed 3.5 billion by 2033.

Fluorine-free Greaseproof Paper Segmentation

-

1. Application

- 1.1. Bakery

- 1.2. Fast Food Restaurant

- 1.3. Home Use

- 1.4. Others

-

2. Types

- 2.1. Natural Greaseproof Paper

- 2.2. Coated Greaseproof Paper

Fluorine-free Greaseproof Paper Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fluorine-free Greaseproof Paper Regional Market Share

Geographic Coverage of Fluorine-free Greaseproof Paper

Fluorine-free Greaseproof Paper REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Bakery

- 5.1.2. Fast Food Restaurant

- 5.1.3. Home Use

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Natural Greaseproof Paper

- 5.2.2. Coated Greaseproof Paper

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Bakery

- 6.1.2. Fast Food Restaurant

- 6.1.3. Home Use

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Natural Greaseproof Paper

- 6.2.2. Coated Greaseproof Paper

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Bakery

- 7.1.2. Fast Food Restaurant

- 7.1.3. Home Use

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Natural Greaseproof Paper

- 7.2.2. Coated Greaseproof Paper

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Bakery

- 8.1.2. Fast Food Restaurant

- 8.1.3. Home Use

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Natural Greaseproof Paper

- 8.2.2. Coated Greaseproof Paper

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Bakery

- 9.1.2. Fast Food Restaurant

- 9.1.3. Home Use

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Natural Greaseproof Paper

- 9.2.2. Coated Greaseproof Paper

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Bakery

- 10.1.2. Fast Food Restaurant

- 10.1.3. Home Use

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Natural Greaseproof Paper

- 10.2.2. Coated Greaseproof Paper

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Fluorine-free Greaseproof Paper Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Bakery

- 11.1.2. Fast Food Restaurant

- 11.1.3. Home Use

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Natural Greaseproof Paper

- 11.2.2. Coated Greaseproof Paper

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ahlstrom

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nordic Paper

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 ERMOLL

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Krpa Paper

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Pfleiderer

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pudumjee Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Zhejiang Kaifeng New Material

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Qingdao Rongxin Industry and Trade

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Zhejiang Fulai New Materials

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Ahlstrom

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fluorine-free Greaseproof Paper Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Fluorine-free Greaseproof Paper Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Fluorine-free Greaseproof Paper Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fluorine-free Greaseproof Paper Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Fluorine-free Greaseproof Paper Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fluorine-free Greaseproof Paper Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Fluorine-free Greaseproof Paper Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fluorine-free Greaseproof Paper Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Fluorine-free Greaseproof Paper Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fluorine-free Greaseproof Paper Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Fluorine-free Greaseproof Paper Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fluorine-free Greaseproof Paper Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Fluorine-free Greaseproof Paper Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fluorine-free Greaseproof Paper Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Fluorine-free Greaseproof Paper Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fluorine-free Greaseproof Paper Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Fluorine-free Greaseproof Paper Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fluorine-free Greaseproof Paper Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Fluorine-free Greaseproof Paper Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fluorine-free Greaseproof Paper Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fluorine-free Greaseproof Paper Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fluorine-free Greaseproof Paper Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fluorine-free Greaseproof Paper Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fluorine-free Greaseproof Paper Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fluorine-free Greaseproof Paper Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fluorine-free Greaseproof Paper Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Fluorine-free Greaseproof Paper Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fluorine-free Greaseproof Paper Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Fluorine-free Greaseproof Paper Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fluorine-free Greaseproof Paper Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Fluorine-free Greaseproof Paper Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Fluorine-free Greaseproof Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fluorine-free Greaseproof Paper Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluorine-free Greaseproof Paper?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Fluorine-free Greaseproof Paper?

Key companies in the market include Ahlstrom, Nordic Paper, ERMOLL, Krpa Paper, Pfleiderer, Pudumjee Group, Zhejiang Kaifeng New Material, Qingdao Rongxin Industry and Trade, Zhejiang Fulai New Materials.

3. What are the main segments of the Fluorine-free Greaseproof Paper?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluorine-free Greaseproof Paper," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluorine-free Greaseproof Paper report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluorine-free Greaseproof Paper?

To stay informed about further developments, trends, and reports in the Fluorine-free Greaseproof Paper, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence