Key Insights

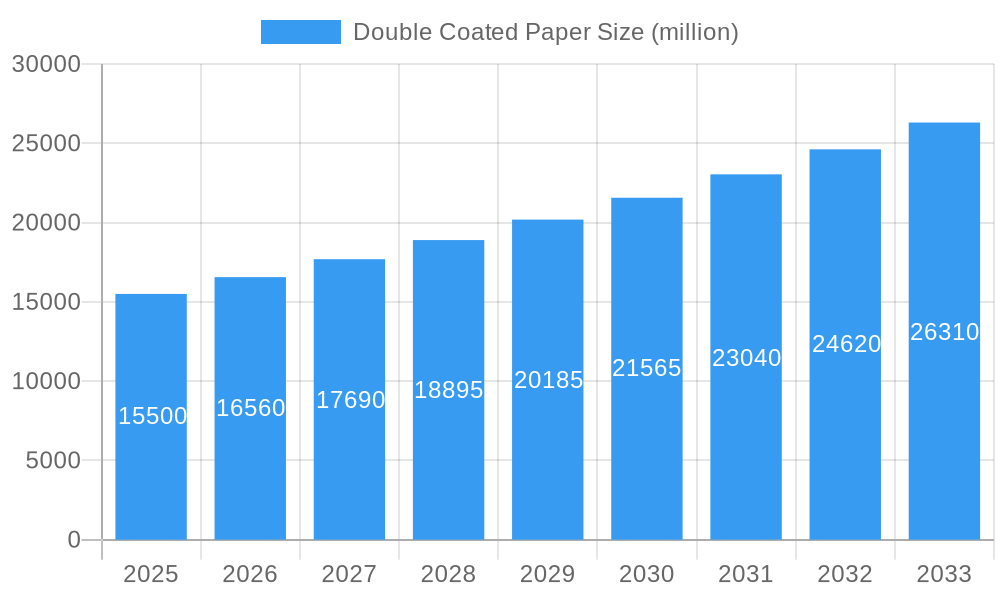

The global Double Coated Paper market is poised for significant expansion, projected to reach a substantial market size of USD 15,500 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 6.8% through to 2033. This robust growth is primarily fueled by the escalating demand from the Food Processing Industry and the burgeoning Catering Industry, both of which rely heavily on high-quality, versatile packaging solutions. The inherent properties of double coated paper, such as its superior printability, grease resistance, and barrier characteristics, make it an ideal choice for a wide array of food packaging applications, from fast-food containers and takeaway boxes to confectionery wrappers and premium food product packaging. The increasing consumer preference for convenient, ready-to-eat meals and the growing emphasis on aesthetic appeal in food branding further bolster the demand for advanced packaging materials like double coated paper.

Double Coated Paper Market Size (In Billion)

Key drivers shaping this market landscape include the continuous innovation in paper coating technologies, leading to enhanced functionalities and sustainability profiles, and the increasing adoption of eco-friendly packaging alternatives. The market is segmented by quantitative types, with Type II (50g/m²-120g/m²) and Type III High Quantitative (greater than 150g/m²) expected to witness substantial demand due to their suitability for more demanding packaging applications. While the market benefits from these drivers, it also faces certain restraints, such as the fluctuating prices of raw materials and the growing competition from alternative packaging materials. Geographically, the Asia Pacific region, led by China and India, is anticipated to be a major growth engine, owing to its large population, rapid industrialization, and increasing disposable incomes, leading to higher consumption of packaged foods. North America and Europe also represent significant markets, driven by stringent regulations for food safety and a mature consumer base demanding premium packaging.

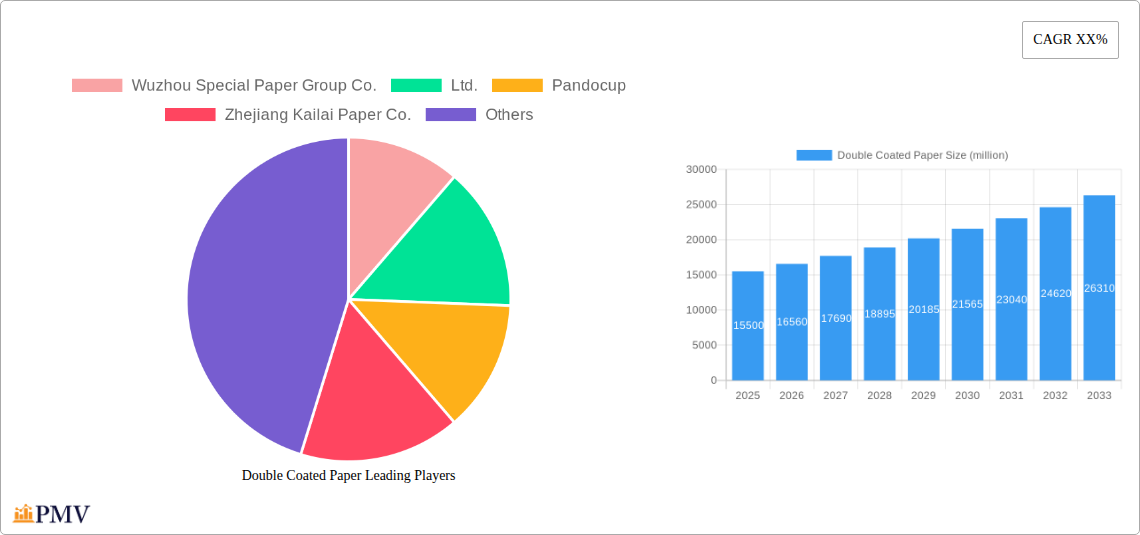

Double Coated Paper Company Market Share

This in-depth report provides a detailed examination of the global Double Coated Paper market, offering critical insights into its structure, trends, segmentation, and competitive landscape. Spanning a comprehensive study period from 2019 to 2033, with a base year of 2025, this report is essential for stakeholders seeking to understand the present dynamics and future trajectory of this vital industry. We delve into market growth drivers, technological innovations, dominant segments, and the strategic outlook for key players. This analysis will empower businesses to make informed decisions in the evolving food packaging paper and specialty paper sectors.

Double Coated Paper Market Structure & Competitive Dynamics

The global Double Coated Paper market exhibits a moderately concentrated structure, with a few key players holding significant market share, particularly in the food processing industry applications. Innovation is driven by continuous R&D focused on enhancing barrier properties, printability, and sustainability, crucial for the catering industry. Regulatory frameworks, primarily concerning food contact safety and environmental impact, play a pivotal role in shaping market entry and product development. Product substitutes, such as single-coated papers or alternative packaging materials like plastics and compostable alternatives, pose a constant competitive challenge, necessitating continuous product differentiation. End-user trends are heavily influenced by increasing consumer demand for convenient, safe, and aesthetically appealing food packaging. Mergers and acquisitions (M&A) activity, while not at extremely high levels, are strategic moves to consolidate market position, expand product portfolios, and gain access to new technologies or geographical markets. For instance, a recent M&A deal in the past two years involving a major player in coated paper amounted to an estimated value of $150 million, signaling industry consolidation. Market share for leading players in specific segments like Type II (50g/m²-120g/m²) can range from 15% to 25%. The competitive landscape is characterized by intense price competition and a focus on delivering tailored solutions for diverse end-use requirements.

Double Coated Paper Industry Trends & Insights

The Double Coated Paper industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.8% during the forecast period 2025–2033. This growth is primarily fueled by the escalating demand for sustainable and high-performance packaging solutions across the food processing industry and the rapidly expanding catering industry. Technological advancements are revolutionizing the production of double coated paper, enabling enhanced barrier properties against moisture, grease, and oxygen, which are critical for preserving food freshness and extending shelf life. The development of specialized coatings, including water-based and bio-based formulations, is a significant trend, aligning with increasing consumer preferences for eco-friendly packaging. Market penetration of double coated paper in emerging economies is expected to accelerate due to rising disposable incomes and a growing middle class that demands convenience and quality in their food consumption. Competitive dynamics are evolving, with manufacturers increasingly focusing on value-added products and customized solutions. The shift towards digital printing technologies for enhanced customization and shorter print runs also presents a notable trend. Consumer preferences are increasingly leaning towards packaging that is not only functional but also visually appealing and environmentally responsible, driving innovation in paper coatings and printing techniques. The global double coated paper market size was valued at approximately $5,500 million in the base year 2025, and is projected to reach over $8,800 million by 2033.

Dominant Markets & Segments in Double Coated Paper

The Catering Industry currently represents the dominant segment within the Double Coated Paper market, driven by the increasing prevalence of food delivery services, fast-food chains, and the overall growth in the hospitality sector. This segment's dominance is further amplified by the continuous need for high-quality, visually appealing, and functional packaging that can withstand diverse culinary applications. Within the Catering Industry, Type II (50g/m²-120g/m²) double coated paper is the most widely adopted type, offering an optimal balance of strength, printability, and cost-effectiveness for applications like takeaway containers, food wrappers, and coffee cups. The Food Processing Industry is the second-largest segment, witnessing significant adoption for primary and secondary packaging of a wide range of food products, including baked goods, confectionery, and frozen foods.

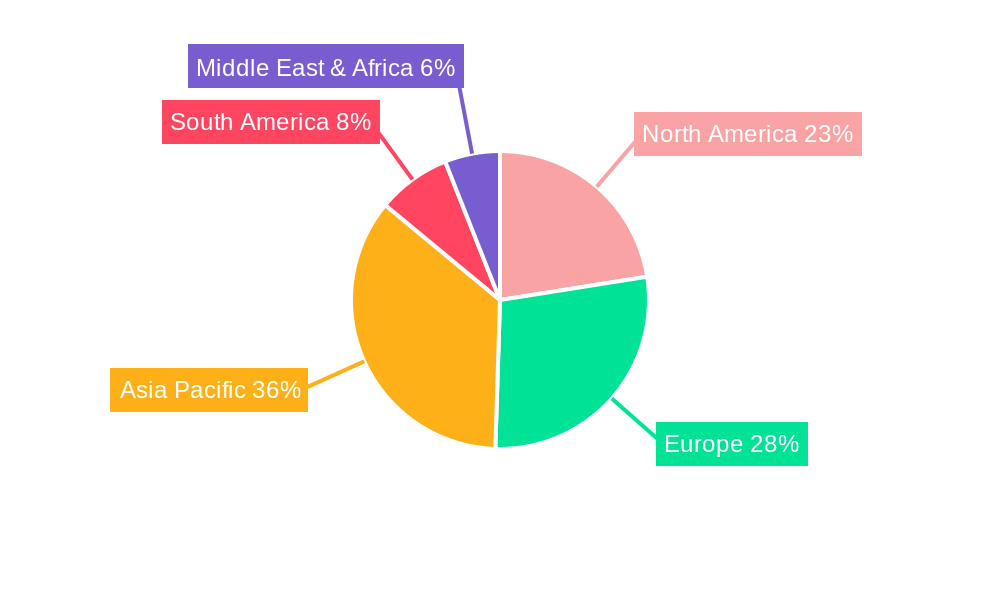

- Leading Region: Asia-Pacific is the leading geographical market for double coated paper, primarily due to the presence of a large manufacturing base, a rapidly growing population, and increasing urbanization that fuels demand from both the catering and food processing industries. Key countries like China and India are significant contributors to this regional dominance.

- Dominant Application Segment: The Catering Industry's demand for packaging that offers excellent printability for branding and marketing, coupled with superior barrier properties to maintain food quality and prevent leakage, solidifies its leading position.

- Dominant Product Type: Type II (50g/m²-120g/m²) double coated paper is the most prevalent due to its versatility and suitability for a broad spectrum of food packaging applications. Its moderate weight makes it cost-effective without compromising essential functional attributes.

- Key Drivers of Dominance (Catering Industry):

- Booming Food Delivery Ecosystem: The exponential growth of online food ordering platforms has created an unprecedented demand for reliable and attractive takeaway packaging.

- Fast Food Expansion: The proliferation of fast-food chains globally necessitates high-volume, consistent quality packaging solutions.

- Consumer Demand for Convenience: Consumers increasingly seek convenient, ready-to-eat options, driving the need for portable and well-packaged food items.

- Branding and Marketing: Double coated paper’s superior printability allows for effective brand messaging and aesthetic appeal, crucial in a competitive market.

- Key Drivers of Dominance (Food Processing Industry):

- Product Shelf-Life Extension: The demand for packaging that can protect processed foods from spoilage and maintain their freshness for longer periods.

- Food Safety Regulations: Stringent food safety regulations necessitate the use of approved and high-barrier packaging materials.

- E-commerce Growth: The rise of e-commerce in food products requires robust packaging that can withstand the rigors of shipping and handling.

Double Coated Paper Product Innovations

Innovations in Double Coated Paper are primarily focused on enhancing sustainability, functionality, and printability. Manufacturers are developing bio-based coatings derived from renewable resources to reduce environmental impact, catering to the growing consumer demand for eco-friendly packaging. Advancements in barrier technologies are leading to improved resistance against moisture, grease, and oxygen, thereby extending the shelf-life of packaged food products. Furthermore, enhanced surface treatments are improving the print quality and vibrant color reproduction for marketing and branding purposes. These innovations provide a significant competitive advantage for companies offering advanced, eco-conscious, and visually appealing packaging solutions.

Report Segmentation & Scope

This report segments the Double Coated Paper market based on key criteria to provide a granular understanding of its dynamics. The primary segmentation includes:

- Application: The market is analyzed across the Catering Industry and the Food Processing Industry. The catering segment, driven by food service and delivery, is expected to exhibit a CAGR of 6.2%, reaching an estimated $4,500 million by 2033. The food processing segment, crucial for packaged food goods, is projected to grow at a CAGR of 5.5%, valued at approximately $4,300 million by 2033.

- Types: The analysis covers three distinct types: Type I Low Quantitative (less than 40.0g/m²), Type II (50g/m²-120g/m²), and Type III High Quantitative (greater than 150g/m²). Type II is anticipated to maintain its leading market share, accounting for over 50% of the market, with a projected CAGR of 5.9%. Type I is expected to see steady growth driven by specific lightweight packaging needs, while Type III will cater to premium and high-barrier applications, growing at a CAGR of 5.7%.

Key Drivers of Double Coated Paper Growth

The growth of the Double Coated Paper market is propelled by several interconnected factors. The escalating global demand for convenient and safe food packaging, particularly driven by the expansion of the catering industry and food delivery services, is a primary catalyst. Increasing consumer awareness and preference for sustainable and recyclable packaging solutions are compelling manufacturers to invest in eco-friendly paper coatings and production processes. Technological advancements in coating formulations and paper manufacturing techniques are enabling enhanced barrier properties, improved printability, and greater durability, meeting the evolving needs of food processors and caterers. Furthermore, favorable government regulations promoting the use of paper-based packaging over plastics in many regions are creating a significant growth impetus.

Challenges in the Double Coated Paper Sector

Despite its robust growth, the Double Coated Paper sector faces several challenges. Fluctuations in raw material prices, particularly wood pulp and chemicals used in coatings, can impact manufacturing costs and profit margins. The presence of alternative packaging materials, such as plastics and advanced composite materials, continues to pose a competitive threat, especially in applications where cost-effectiveness is the paramount consideration. Stringent environmental regulations and the increasing demand for certified sustainable sourcing can add to production complexity and compliance costs. Furthermore, supply chain disruptions, exacerbated by global events, can affect the availability and timely delivery of raw materials and finished products, impacting market stability.

Leading Players in the Double Coated Paper Market

- Wuzhou Special Paper Group Co.,Ltd.

- Pandocup

- Zhejiang Kailai Paper Co.,Ltd.

- Fowa Holdings

- Zhongchanpaper

- ZHUHAI HONGTA RENHENG PACKAGING CO.,LTD.

- Lianyungang Genshen Paper PRODUCT Co.,Ltd.

- Lianyungang Jinhe Paper Packaging Co.,Ltd.

- Anqing Qianqian Technology Packaging Co.,Ltd.

- Qingdao Rongxin Industry and Trade co.,ltd.

- Novinsure Corporation Ltd.

- Chengdu Kailai Packaging Co.,Ltd.

- Shandong Quanlin Paper Co.,Ltd.

- Anhui Kailai Paper Co.,Ltd.

Key Developments in Double Coated Paper Sector

- 2023 Q4: Launch of a new range of compostable double coated papers with enhanced grease resistance for bakery applications by a leading European manufacturer.

- 2023 Q3: Acquisition of a specialized coating technology firm by a major Chinese paper producer to bolster its R&D capabilities in barrier coatings for food packaging.

- 2022 Q2: Introduction of water-based barrier coatings that significantly reduce VOC emissions during production, aligning with stricter environmental regulations.

- 2021 Q1: Significant investment in expanded production capacity for high-volume Type II double coated paper to meet the surging demand from the food delivery market.

Strategic Double Coated Paper Market Outlook

The strategic outlook for the Double Coated Paper market is exceptionally positive, driven by the sustained global demand for sustainable and high-performance packaging solutions. Key growth accelerators include the ongoing innovation in bio-based and recyclable coatings, which directly addresses consumer and regulatory pressures. The expanding food service sector, coupled with the rapid growth of e-commerce for food products, presents significant opportunities for market expansion. Companies that focus on developing specialized double coated papers with superior barrier properties, excellent printability, and verifiable environmental credentials will be well-positioned for success. Strategic partnerships and collaborations aimed at enhancing supply chain efficiency and promoting circular economy principles will further strengthen market positions. The increasing adoption of digital printing technologies offers further avenues for customization and value creation for end-users.

Double Coated Paper Segmentation

-

1. Application

- 1.1. Catering Industry

- 1.2. Food Processing Industry

-

2. Types

- 2.1. Type I Low Quantitative (less than 40.0g/m²)

- 2.2. Type II (50g/m²-120g/m²)

- 2.3. Type III High Quantitative (greater than 150g/m²)

Double Coated Paper Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Double Coated Paper Regional Market Share

Geographic Coverage of Double Coated Paper

Double Coated Paper REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Catering Industry

- 5.1.2. Food Processing Industry

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 5.2.2. Type II (50g/m²-120g/m²)

- 5.2.3. Type III High Quantitative (greater than 150g/m²)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Double Coated Paper Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Catering Industry

- 6.1.2. Food Processing Industry

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 6.2.2. Type II (50g/m²-120g/m²)

- 6.2.3. Type III High Quantitative (greater than 150g/m²)

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Double Coated Paper Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Catering Industry

- 7.1.2. Food Processing Industry

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 7.2.2. Type II (50g/m²-120g/m²)

- 7.2.3. Type III High Quantitative (greater than 150g/m²)

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Double Coated Paper Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Catering Industry

- 8.1.2. Food Processing Industry

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 8.2.2. Type II (50g/m²-120g/m²)

- 8.2.3. Type III High Quantitative (greater than 150g/m²)

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Double Coated Paper Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Catering Industry

- 9.1.2. Food Processing Industry

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 9.2.2. Type II (50g/m²-120g/m²)

- 9.2.3. Type III High Quantitative (greater than 150g/m²)

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Double Coated Paper Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Catering Industry

- 10.1.2. Food Processing Industry

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 10.2.2. Type II (50g/m²-120g/m²)

- 10.2.3. Type III High Quantitative (greater than 150g/m²)

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Double Coated Paper Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Catering Industry

- 11.1.2. Food Processing Industry

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Type I Low Quantitative (less than 40.0g/m²)

- 11.2.2. Type II (50g/m²-120g/m²)

- 11.2.3. Type III High Quantitative (greater than 150g/m²)

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Wuzhou Special Paper Group Co.

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ltd.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Pandocup

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Zhejiang Kailai Paper Co.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ltd.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fowa Holdings

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Zhongchanpaper

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 ZHUHAI HONGTA RENHENG PACKAGING CO.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LTD.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Lianyungang Genshen Paper PRODUCT Co.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ltd.

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Lianyungang Jinhe Paper Packaging Co.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Anqing Qianqian Technology Packaging Co.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Ltd.

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Qingdao Rongxin Industry and Trade co.

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 ltd.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Novinsure Corporation Ltd.

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Chengdu Kailai Packaging Co.

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Ltd.

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Shandong Quanlin Paper Co.

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Ltd.

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Anhui Kailai Paper Co.

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 Ltd.

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.1 Wuzhou Special Paper Group Co.

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Double Coated Paper Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Double Coated Paper Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Double Coated Paper Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Double Coated Paper Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Double Coated Paper Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Double Coated Paper Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Double Coated Paper Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Double Coated Paper Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Double Coated Paper Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Double Coated Paper Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Double Coated Paper Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Double Coated Paper Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Double Coated Paper Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Double Coated Paper Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Double Coated Paper Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Double Coated Paper Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Double Coated Paper Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Double Coated Paper Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Double Coated Paper Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Double Coated Paper Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Double Coated Paper Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Double Coated Paper Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Double Coated Paper Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Double Coated Paper Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Double Coated Paper Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Double Coated Paper Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Double Coated Paper Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Double Coated Paper Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Double Coated Paper Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Double Coated Paper Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Double Coated Paper Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Double Coated Paper Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Double Coated Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Double Coated Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Double Coated Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Double Coated Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Double Coated Paper Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Double Coated Paper Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Double Coated Paper Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Double Coated Paper Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Double Coated Paper?

The projected CAGR is approximately 5.85%.

2. Which companies are prominent players in the Double Coated Paper?

Key companies in the market include Wuzhou Special Paper Group Co., Ltd., Pandocup, Zhejiang Kailai Paper Co., Ltd., Fowa Holdings, Zhongchanpaper, ZHUHAI HONGTA RENHENG PACKAGING CO., LTD., Lianyungang Genshen Paper PRODUCT Co., Ltd., Lianyungang Jinhe Paper Packaging Co., Ltd., Anqing Qianqian Technology Packaging Co., Ltd., Qingdao Rongxin Industry and Trade co., ltd., Novinsure Corporation Ltd., Chengdu Kailai Packaging Co., Ltd., Shandong Quanlin Paper Co., Ltd., Anhui Kailai Paper Co., Ltd..

3. What are the main segments of the Double Coated Paper?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Double Coated Paper," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Double Coated Paper report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Double Coated Paper?

To stay informed about further developments, trends, and reports in the Double Coated Paper, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence