Key Insights

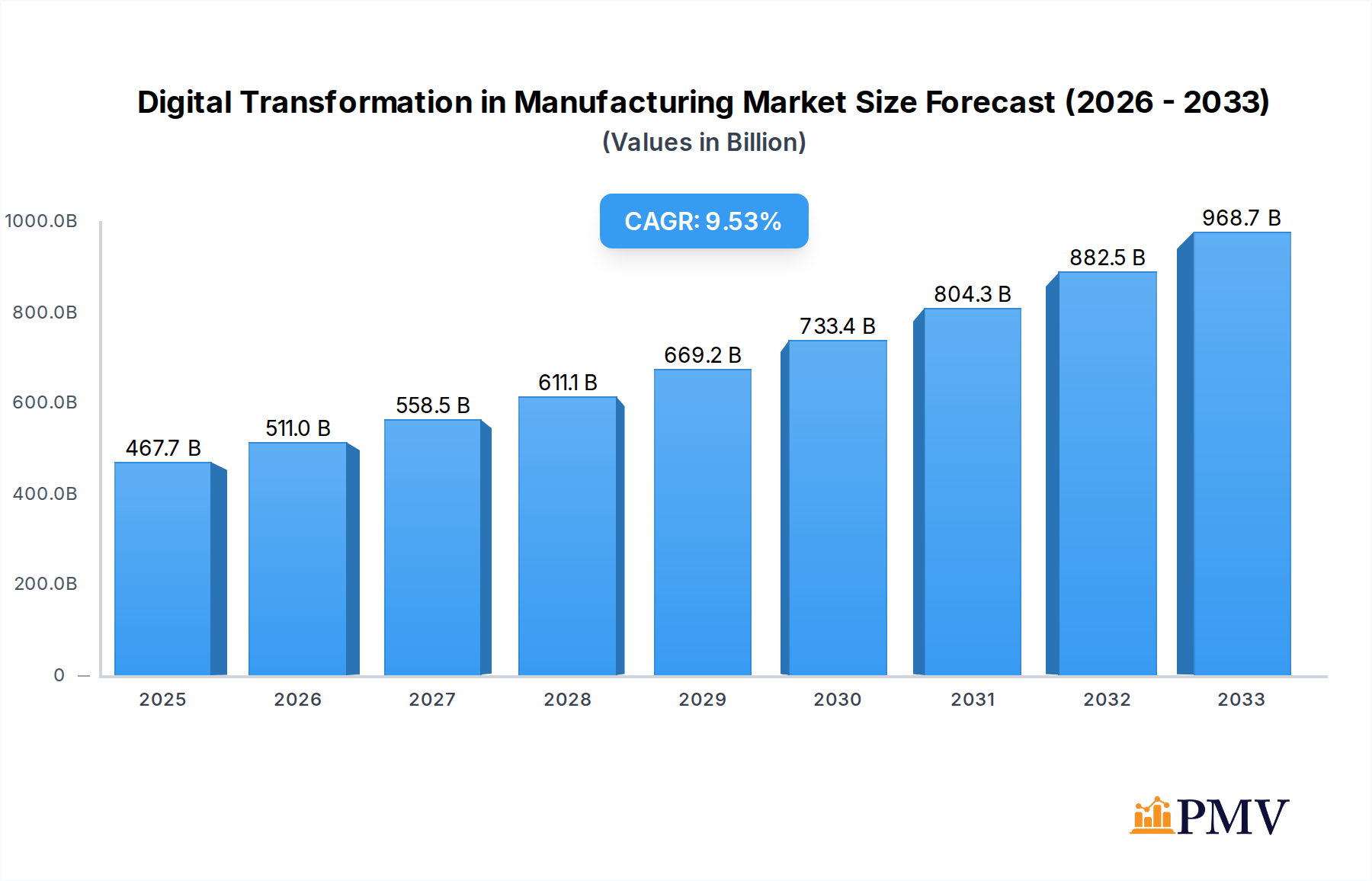

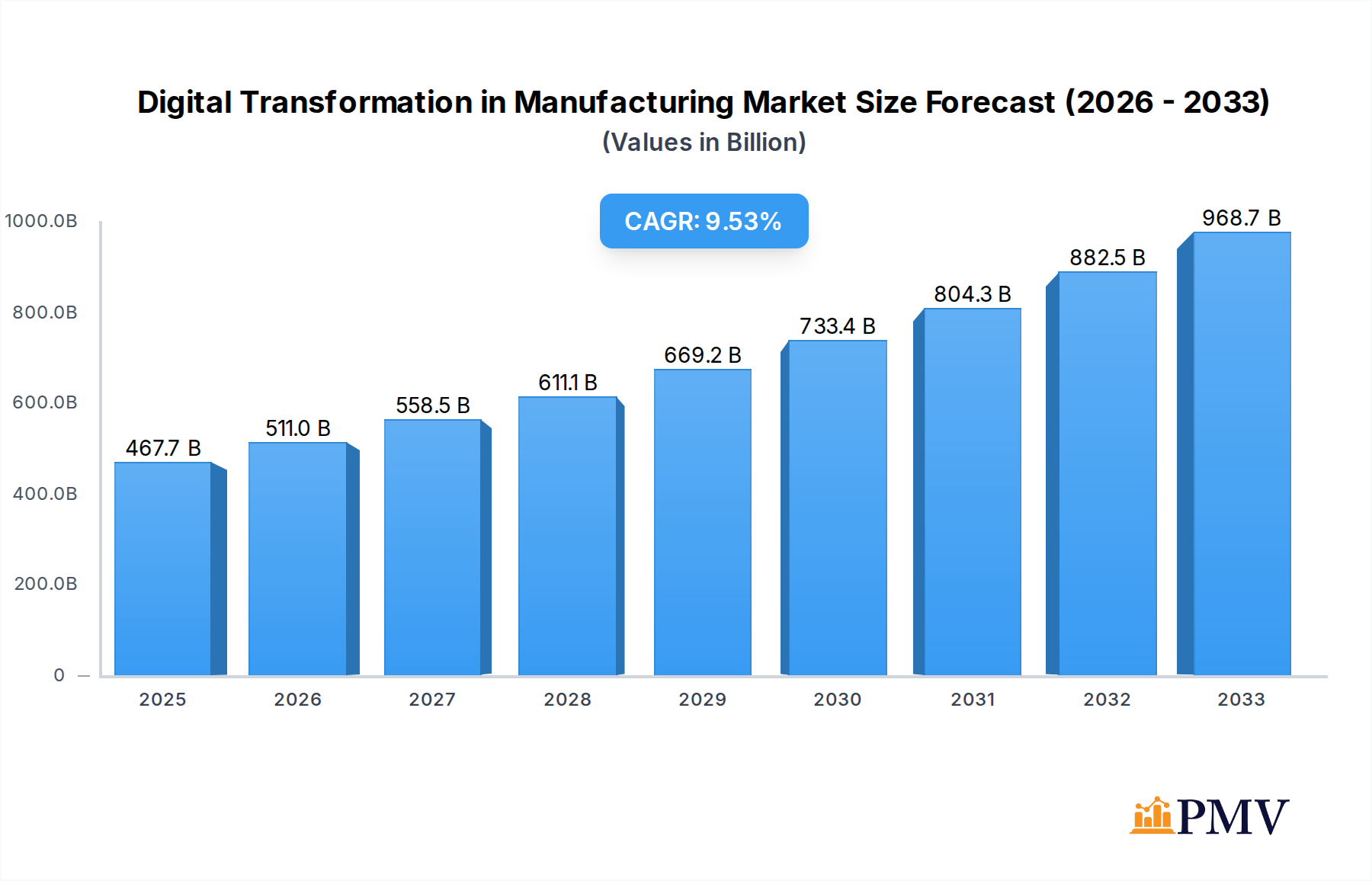

The global Digital Transformation in Manufacturing market is poised for substantial expansion, projected to reach USD 467.72 billion by 2025. This robust growth trajectory is driven by a compelling CAGR of 9.36% during the forecast period of 2025-2033. Key accelerators for this transformation include the increasing adoption of advanced technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), robotics, and 3D printing, which are revolutionizing operational efficiency, product quality, and supply chain agility. Companies are heavily investing in these solutions to enhance predictive maintenance, optimize production processes, and foster greater connectivity across their value chains. The imperative to remain competitive in a rapidly evolving industrial landscape, coupled with the growing demand for smart manufacturing and Industry 4.0 initiatives, further fuels this market's upward momentum.

Digital Transformation in Manufacturing Market Size (In Billion)

The market is segmented across various applications, including upstream, midstream, and downstream sectors, with each leveraging digital solutions to address unique challenges and capitalize on emerging opportunities. By type, robotics, IoT, 3D printing and additive manufacturing, and cybersecurity represent the dominant technological segments, with "Other" encompassing a range of emerging innovations. Restraints such as the high initial investment costs and the need for skilled labor to implement and manage these advanced systems are being addressed through strategic partnerships and government initiatives. Major players like Cisco Systems Inc., Microsoft Corporation, Intel Corporation, IBM Corporation, and Siemens AG are at the forefront, driving innovation and offering comprehensive digital solutions that cater to the diverse needs of the manufacturing industry globally.

Digital Transformation in Manufacturing Company Market Share

This comprehensive report, "Digital Transformation in Manufacturing: Market Analysis, Trends, and Future Outlook 2019-2033," delivers an in-depth examination of the burgeoning digital transformation landscape within the global manufacturing sector. Spanning a detailed study period from 2019 to 2033, with a base and estimated year of 2025, and a robust forecast period from 2025 to 2033, this analysis provides actionable intelligence for stakeholders. The historical period of 2019-2024 lays the foundation for understanding past market trajectories. This report leverages billions in market valuation to offer unparalleled insights into revenue projections and investment opportunities.

The digital transformation market in manufacturing is experiencing unprecedented growth, driven by the integration of advanced technologies like Industrial IoT (IIoT), Robotics, Artificial Intelligence (AI), and Cybersecurity solutions. Manufacturers are increasingly adopting these technologies to enhance operational efficiency, improve product quality, optimize supply chains, and achieve greater agility in a competitive global market. The report meticulously analyzes the market structure and competitive dynamics, examining market concentration, innovation ecosystems, regulatory frameworks, product substitutes, end-user trends, and significant M&A activities. With an estimated market size projected to reach hundreds of billions by 2025, and a CAGR of xx% during the forecast period, this market presents substantial opportunities.

Digital Transformation in Manufacturing Market Structure & Competitive Dynamics

The digital transformation in manufacturing market exhibits a dynamic and evolving structure, characterized by a blend of large established technology providers and agile specialized solution developers. Market concentration varies across different segments and geographical regions, with North America and Europe currently leading in adoption rates. Innovation ecosystems are thriving, fueled by collaborative efforts between technology giants, academic institutions, and manufacturing firms. Regulatory frameworks are continuously adapting to address data privacy, cybersecurity, and the ethical implications of advanced manufacturing technologies. Product substitutes are becoming increasingly sophisticated, as convergence of various digital solutions offers comprehensive alternatives to standalone technologies. End-user trends underscore a strong demand for intelligent automation, predictive maintenance, and personalized manufacturing. Merger and Acquisition (M&A) activities are prevalent, with an estimated tens of billions in deal values recorded annually, as major players seek to consolidate market presence, acquire cutting-edge technologies, and expand their service portfolios. Key players like Cisco Systems Inc., Microsoft Corporation, Intel Corporation, IBM Corporation, Siemens AG, SAP SE, Oracle Corporation, and Schneider Electric SE are actively involved in strategic acquisitions to strengthen their offerings in areas such as cloud computing, AI, and IIoT platforms.

Digital Transformation in Manufacturing Industry Trends & Insights

The global digital transformation in manufacturing market is poised for extraordinary growth, projected to surpass billions in market value by 2033. This expansion is propelled by a confluence of compelling market growth drivers and transformative technological disruptions. The increasing adoption of Industrial IoT (IIoT) is a paramount trend, enabling real-time data collection, analysis, and remote monitoring of manufacturing processes, thereby optimizing efficiency and reducing downtime. Robotics and automation are revolutionizing production lines, enhancing precision, speed, and safety, with investments in collaborative robots (cobots) and autonomous mobile robots (AMRs) surging. 3D printing and additive manufacturing are redefining product design and prototyping, enabling mass customization and on-demand production, leading to significant cost savings and accelerated time-to-market.

Cybersecurity has emerged as a critical concern and a significant market segment, as the interconnected nature of smart factories necessitates robust protection against data breaches and operational disruptions. Companies are investing heavily in advanced cybersecurity solutions to safeguard their intellectual property and operational continuity. The Upstream, Midstream, and Downstream segments of the oil and gas industry, as well as discrete and process manufacturing, are all undergoing significant digital overhauls, each with unique adoption patterns and challenges. Consumer preferences are shifting towards more personalized and sustainable products, compelling manufacturers to adopt flexible and agile production models. Competitive dynamics are intensifying, with companies that successfully integrate digital technologies gaining a substantial competitive edge. The CAGR for the digital transformation in manufacturing market is estimated at xx% over the forecast period, reflecting a robust and sustained growth trajectory. Market penetration of IIoT devices is expected to reach xx% by 2025, a testament to the widespread adoption of smart manufacturing principles.

Dominant Markets & Segments in Digital Transformation in Manufacturing

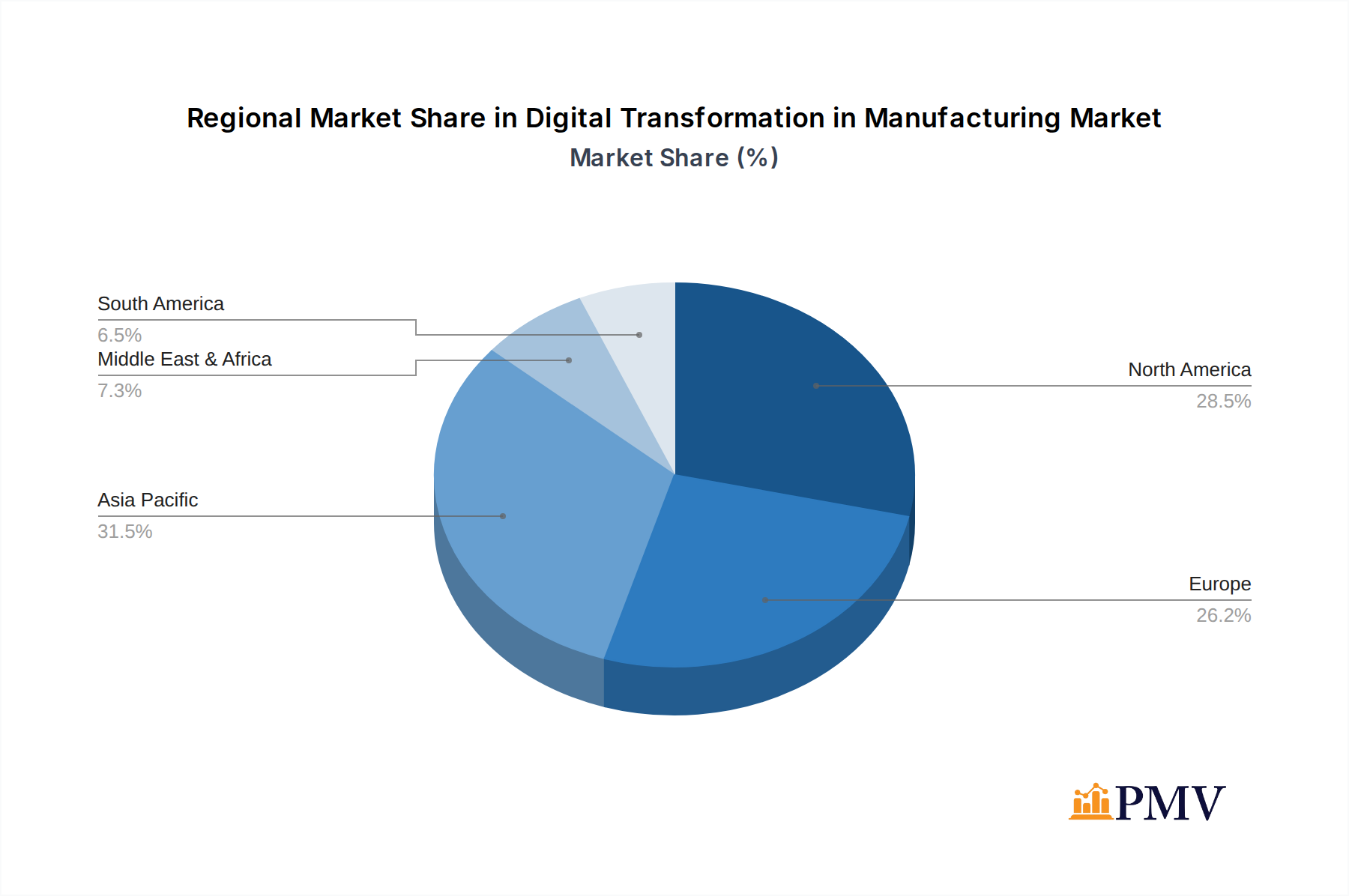

The North America region stands as a dominant market in the digital transformation of manufacturing, driven by substantial investments in advanced manufacturing technologies and a strong presence of leading technology providers. Within North America, the United States spearheads this digital revolution, supported by robust economic policies that encourage innovation, significant government funding for research and development, and a highly developed industrial infrastructure.

Application:

- Upstream: While traditionally lagging in digital adoption compared to downstream, the upstream sector is rapidly embracing digital solutions for exploration, drilling, and extraction optimization, driven by the need for cost reduction and enhanced safety.

- Midstream: This segment benefits significantly from digital transformation through optimized logistics, pipeline monitoring, and supply chain management, leading to improved efficiency and reduced environmental risks.

- Downstream: The downstream sector, encompassing refining and petrochemicals, is a major adopter of digital technologies for process automation, predictive maintenance, and quality control, leading to enhanced profitability and operational excellence.

Types:

- Robotics: The adoption of advanced robotic systems, including industrial robots and collaborative robots, is a key driver across all manufacturing types, enhancing productivity and precision.

- IoT (Industrial IoT): IIoT platforms are foundational to smart manufacturing, enabling real-time data insights, remote monitoring, and predictive analytics, significantly impacting operational efficiency.

- 3D Printing and Additive Manufacturing: This segment is witnessing exponential growth in prototyping and specialized part production, offering unparalleled design freedom and customization capabilities across various industries.

- Cybersecurity: As manufacturing processes become increasingly digitized and interconnected, robust cybersecurity solutions are paramount, driving significant investment to protect critical infrastructure and intellectual property.

- Other: This broad category includes AI, machine learning, cloud computing, and augmented reality, all of which are integral components of the digital transformation journey, enabling advanced analytics, intelligent automation, and enhanced workforce capabilities.

Digital Transformation in Manufacturing Product Innovations

Product innovations in digital transformation for manufacturing are characterized by the convergence of AI, IoT, and advanced analytics. Companies are developing intelligent automation solutions that offer predictive maintenance capabilities, significantly reducing unexpected downtime and optimizing asset utilization. Siemens AG is a frontrunner with its integrated digital enterprise portfolio, while Microsoft Corporation continues to enhance its Azure IoT platform for industrial applications. Intel Corporation is focusing on edge computing solutions that empower real-time data processing on factory floors. These innovations provide manufacturers with enhanced operational visibility, improved decision-making, and a competitive edge through increased efficiency and agility.

Report Segmentation & Scope

This report segments the digital transformation in manufacturing market by Application and Type. The Application segments include Upstream, Midstream, and Downstream industries, each with distinct digital adoption drivers and market sizes projected to reach billions by 2033. The Type segments encompass Robotics, IoT, 3D Printing and Additive Manufacturing, Cybersecurity, and Other enabling technologies like AI and cloud computing. Each segment's growth projections, market sizes, and competitive dynamics are meticulously analyzed, offering a granular view of market opportunities.

Key Drivers of Digital Transformation in Manufacturing Growth

The growth of the digital transformation in manufacturing sector is propelled by several key drivers. Technologically, the increasing sophistication and decreasing cost of Industrial IoT (IIoT) devices, coupled with advancements in AI and machine learning for data analytics, are fundamental. Economically, the relentless pursuit of operational efficiency, cost reduction, and enhanced productivity incentivizes substantial investment. Regulatory factors, while sometimes presenting challenges, also drive adoption, particularly concerning cybersecurity standards and environmental compliance. For example, government initiatives promoting smart manufacturing and Industry 4.0 adoption in countries like Germany and the United States act as significant accelerators.

Challenges in the Digital Transformation in Manufacturing Sector

Despite its immense potential, the digital transformation in manufacturing sector faces significant challenges. Cybersecurity threats remain a paramount concern, with sophisticated attacks capable of disrupting operations and compromising sensitive data, costing billions annually. High initial investment costs for new technologies and infrastructure upgrades can be a barrier for small and medium-sized enterprises (SMEs). Lack of skilled workforce to operate and maintain advanced digital systems is another considerable restraint, impacting implementation timelines and effectiveness. Furthermore, data integration and interoperability issues across legacy systems and new digital platforms can lead to inefficiencies and hinder seamless operations.

Leading Players in the Digital Transformation in Manufacturing Market

- Cisco Systems Inc.

- Microsoft Corporation

- Intel Corporation

- IBM Corporation

- Siemens AG

- SAP SE

- Symantec Corporation

- Oracle Corporation

- Schneider Electric SE

- Mitsubishi Electric Corporation

- General Electric Co.

- ABB Ltd

Key Developments in Digital Transformation in Manufacturing Sector

- January 2024: Siemens AG announced a strategic partnership with an AI solutions provider to integrate advanced AI capabilities into its manufacturing automation platforms, enhancing predictive maintenance and anomaly detection.

- December 2023: Microsoft Corporation unveiled new IIoT solutions for the manufacturing sector, focusing on edge computing and enhanced cloud connectivity, targeting a market value of billions.

- November 2023: Intel Corporation launched a new generation of processors optimized for industrial AI and edge computing, supporting the growing demand for real-time data processing in smart factories.

- October 2023: IBM Corporation expanded its cybersecurity offerings for the manufacturing industry, providing comprehensive solutions to combat evolving threats and secure critical operational technology (OT) environments.

- September 2023: Schneider Electric SE acquired a leading provider of industrial automation software, strengthening its portfolio in digital twins and simulation for manufacturing processes.

- August 2023: ABB Ltd introduced a new range of collaborative robots designed for enhanced flexibility and safety in diverse manufacturing environments, with market adoption projected to reach billions.

- July 2023: General Electric Co. showcased its latest advancements in digital industrial solutions, emphasizing enhanced fleet management and predictive analytics for heavy machinery.

- June 2023: Oracle Corporation launched new cloud-based solutions tailored for the manufacturing industry, focusing on supply chain optimization and production planning, with a target market of billions.

- May 2023: SAP SE announced enhanced integration of its IoT and analytics solutions with its enterprise resource planning (ERP) systems, aiming to provide a unified view of manufacturing operations.

- April 2023: Mitsubishi Electric Corporation expanded its factory automation product line, incorporating advanced AI features for quality inspection and process optimization.

Strategic Digital Transformation in Manufacturing Market Outlook

The strategic outlook for the digital transformation in manufacturing market is exceptionally positive, driven by ongoing technological advancements and an increasing imperative for operational resilience and competitiveness. Growth accelerators include the pervasive adoption of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics, autonomous decision-making, and process optimization, which are projected to add billions to the market value. The continued expansion of 5G connectivity will further enable real-time data flow and low-latency communication essential for IIoT applications. Investments in sustainable manufacturing practices, powered by digital solutions, will also present significant strategic opportunities. The market is anticipated to witness further consolidation through strategic M&A activities as companies aim to expand their technological capabilities and market reach.

Digital Transformation in Manufacturing Segmentation

-

1. Application

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

-

2. Types

- 2.1. Robotics

- 2.2. IoT

- 2.3. 3D Printing and Additive Manufacturing

- 2.4. Cybersecurity

- 2.5. Other

Digital Transformation in Manufacturing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Transformation in Manufacturing Regional Market Share

Geographic Coverage of Digital Transformation in Manufacturing

Digital Transformation in Manufacturing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.36% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Robotics

- 5.2.2. IoT

- 5.2.3. 3D Printing and Additive Manufacturing

- 5.2.4. Cybersecurity

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Upstream

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Robotics

- 6.2.2. IoT

- 6.2.3. 3D Printing and Additive Manufacturing

- 6.2.4. Cybersecurity

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Upstream

- 7.1.2. Midstream

- 7.1.3. Downstream

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Robotics

- 7.2.2. IoT

- 7.2.3. 3D Printing and Additive Manufacturing

- 7.2.4. Cybersecurity

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Upstream

- 8.1.2. Midstream

- 8.1.3. Downstream

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Robotics

- 8.2.2. IoT

- 8.2.3. 3D Printing and Additive Manufacturing

- 8.2.4. Cybersecurity

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Upstream

- 9.1.2. Midstream

- 9.1.3. Downstream

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Robotics

- 9.2.2. IoT

- 9.2.3. 3D Printing and Additive Manufacturing

- 9.2.4. Cybersecurity

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Digital Transformation in Manufacturing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Upstream

- 10.1.2. Midstream

- 10.1.3. Downstream

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Robotics

- 10.2.2. IoT

- 10.2.3. 3D Printing and Additive Manufacturing

- 10.2.4. Cybersecurity

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Cisco Systems Inc.

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Microsoft Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Intel Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IBM Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Siemens AG

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SAP SE

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Symantec Corporation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Oracle Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Schneider Electric SE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Mitsubishi Electric Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 General Electric Co.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ABB Ltd

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Cisco Systems Inc.

List of Figures

- Figure 1: Global Digital Transformation in Manufacturing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Digital Transformation in Manufacturing Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Digital Transformation in Manufacturing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Transformation in Manufacturing Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Digital Transformation in Manufacturing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Digital Transformation in Manufacturing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Digital Transformation in Manufacturing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Transformation in Manufacturing Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Digital Transformation in Manufacturing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Transformation in Manufacturing Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Digital Transformation in Manufacturing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Digital Transformation in Manufacturing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Digital Transformation in Manufacturing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Transformation in Manufacturing Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Digital Transformation in Manufacturing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Transformation in Manufacturing Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Digital Transformation in Manufacturing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Digital Transformation in Manufacturing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Digital Transformation in Manufacturing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Transformation in Manufacturing Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Transformation in Manufacturing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Transformation in Manufacturing Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Digital Transformation in Manufacturing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Digital Transformation in Manufacturing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Transformation in Manufacturing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Transformation in Manufacturing Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Transformation in Manufacturing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Transformation in Manufacturing Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Digital Transformation in Manufacturing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Digital Transformation in Manufacturing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Transformation in Manufacturing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Digital Transformation in Manufacturing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Transformation in Manufacturing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Transformation in Manufacturing?

The projected CAGR is approximately 9.36%.

2. Which companies are prominent players in the Digital Transformation in Manufacturing?

Key companies in the market include Cisco Systems Inc., Microsoft Corporation, Intel Corporation, IBM Corporation, Siemens AG, SAP SE, Symantec Corporation, Oracle Corporation, Schneider Electric SE, Mitsubishi Electric Corporation, General Electric Co., ABB Ltd.

3. What are the main segments of the Digital Transformation in Manufacturing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Transformation in Manufacturing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Transformation in Manufacturing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Transformation in Manufacturing?

To stay informed about further developments, trends, and reports in the Digital Transformation in Manufacturing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence