Key Insights

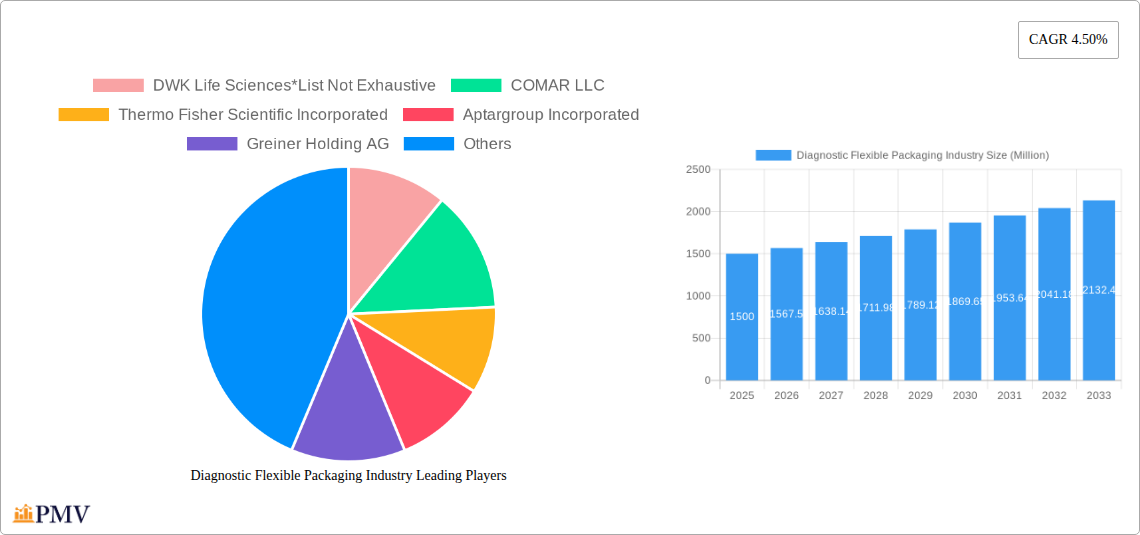

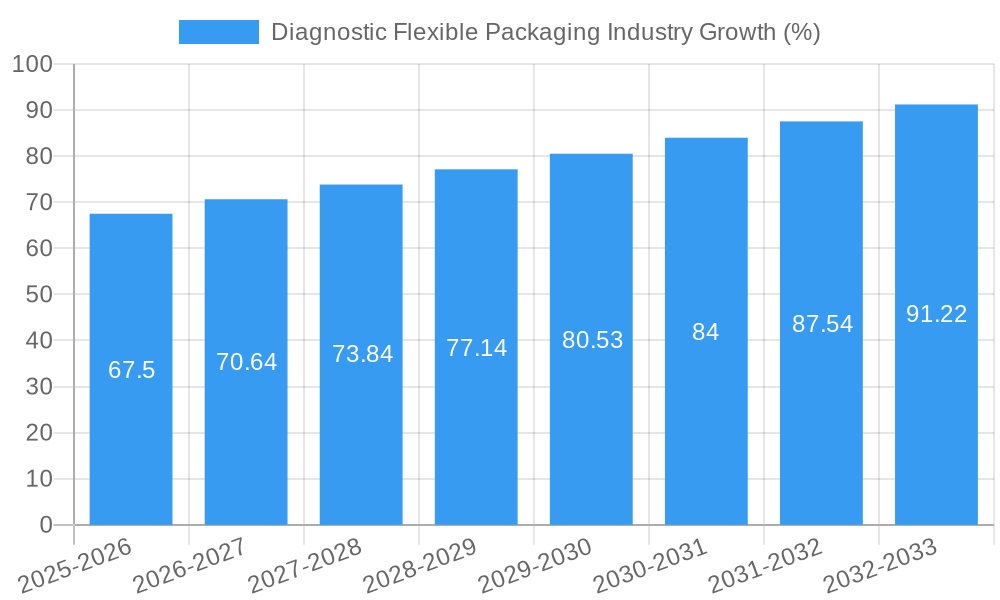

The diagnostic flexible packaging market, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) of 4.50% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing prevalence of chronic diseases globally necessitates more frequent diagnostic testing, boosting demand for packaging solutions. Technological advancements in diagnostic techniques, such as point-of-care testing and personalized medicine, also contribute significantly to market growth. Furthermore, stringent regulatory requirements for sample integrity and safety drive the adoption of high-quality, reliable flexible packaging materials. Growth is segmented across various end-users, with hospitals and laboratories constituting major consumers, followed by academic institutions and other end-users. Product-wise, bottles, vials, and tubes dominate the market, reflecting the diverse needs of diagnostic procedures. While the North American and European markets currently hold significant shares, the Asia-Pacific region is poised for substantial growth due to rising healthcare expenditure and increasing awareness of preventive healthcare. However, factors such as price fluctuations in raw materials and potential environmental concerns associated with certain packaging types may pose challenges to market expansion. The competitive landscape is marked by the presence of both established multinational corporations and specialized regional players, leading to continuous innovation and a focus on providing tailored solutions to meet the evolving demands of the diagnostic industry.

The competitive landscape is highly dynamic, with companies like DWK Life Sciences, COMAR LLC, Thermo Fisher Scientific, AptarGroup, Greiner Holding AG, WS Packaging Group, Amcor Limited, and Corning Incorporated vying for market share. These companies are actively engaged in research and development, focusing on developing innovative packaging solutions that improve sample integrity, enhance convenience, and reduce environmental impact. Strategic partnerships and acquisitions are also becoming prevalent, driving consolidation within the industry. The market is expected to witness further fragmentation in the coming years, with specialized players entering niche segments and offering customized solutions. Future growth will likely be driven by the adoption of sustainable packaging materials and the integration of advanced technologies such as smart packaging solutions that provide real-time monitoring of sample conditions. Furthermore, the increasing demand for at-home diagnostic testing kits will significantly influence packaging requirements, creating opportunities for manufacturers to develop innovative and user-friendly packaging solutions.

Diagnostic Flexible Packaging Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Diagnostic Flexible Packaging industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. The report covers the period 2019-2033, with a focus on the 2025-2033 forecast period. The base year for the analysis is 2025. The market is segmented by end-user (hospitals, laboratories, academic institutes, and other end-users) and product type (bottles, vials, tubes, closures, and other product types). The report analyzes market size (in Millions), growth drivers, challenges, and competitive landscape, offering actionable strategies for success.

Diagnostic Flexible Packaging Industry Market Structure & Competitive Dynamics

The diagnostic flexible packaging market exhibits a moderately concentrated structure, with several major players holding significant market share. The estimated total market size in 2025 is $XX Million. Key players such as Amcor Limited, Thermo Fisher Scientific Incorporated, and Aptargroup Incorporated compete intensely, driving innovation and impacting market dynamics. Market share is predominantly influenced by technological capabilities, product diversification, and global reach. The industry is characterized by a robust innovation ecosystem focused on enhancing packaging materials, improving sterility, and optimizing supply chain efficiency. Regulatory frameworks, particularly those concerning material safety and biocompatibility, play a significant role in shaping market practices. The emergence of sustainable and eco-friendly packaging solutions is driving significant changes within the industry. Mergers and acquisitions (M&A) activity is moderate, with deal values averaging $XX Million in recent years, reflecting strategic consolidation efforts among key players.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately XX% market share in 2025.

- Innovation Ecosystem: Strong focus on sustainable materials, improved sterility, and automation.

- Regulatory Framework: Stringent regulations concerning material safety and biocompatibility.

- Product Substitutes: Limited direct substitutes, but pressure from alternative packaging solutions.

- M&A Activity: Moderate activity with average deal values around $XX Million. Examples include [Insert example M&A deals if available].

Diagnostic Flexible Packaging Industry Industry Trends & Insights

The diagnostic flexible packaging market is experiencing robust growth, driven by factors such as the increasing prevalence of infectious diseases, rising demand for point-of-care diagnostics, and technological advancements in medical packaging. The market is projected to witness a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). Technological disruptions, particularly the adoption of advanced materials like bio-based polymers and smart packaging, are significantly impacting the industry. Consumer preferences are shifting towards sustainable and environmentally friendly packaging solutions, pushing manufacturers to adopt eco-friendly practices. The competitive landscape remains highly dynamic, with leading players constantly innovating and expanding their product portfolios to meet evolving customer needs. Market penetration of advanced packaging technologies is expected to reach XX% by 2033, showcasing the significant adoption rate of innovative solutions.

Dominant Markets & Segments in Diagnostic Flexible Packaging Industry

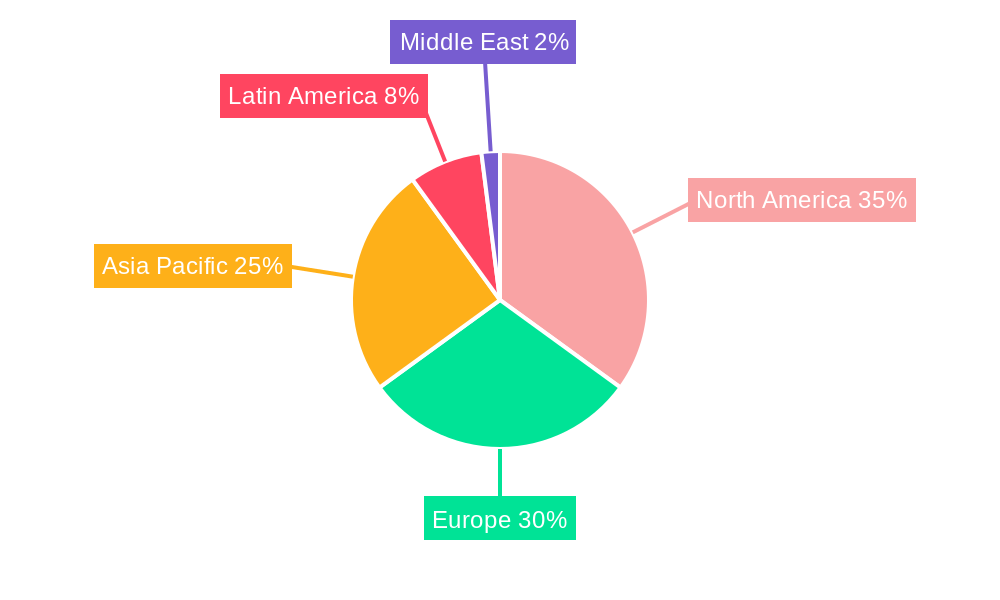

North America currently holds the largest market share within the diagnostic flexible packaging industry, driven primarily by robust healthcare infrastructure, substantial R&D investments, and high adoption rates of advanced diagnostic technologies. Within the end-user segment, hospitals and laboratories represent the major consumers of diagnostic flexible packaging due to high volumes of diagnostic tests and procedures conducted.

Key Drivers by Segment:

- Hospitals: High volumes of diagnostic tests, stringent regulations, and focus on patient safety.

- Laboratories: Growing demand for specialized diagnostic testing and outsourcing of laboratory services.

- Academic Institutes: Growing research activities, focus on new diagnostic methodologies, and need for specialized packaging.

- Other End-Users: Increasing demand for home healthcare and decentralized diagnostic solutions.

- Bottles: High demand for liquid sample storage and transportation.

- Vials: Widely used for storing small volumes of samples or reagents.

- Tubes: Essential for collecting and transporting various samples.

- Closures: Critical for maintaining sample integrity and preventing contamination.

- Other Product Types: Growing use of specialized containers and pouches for various applications.

Dominance Analysis: The dominance of North America is projected to continue throughout the forecast period, although significant growth potential exists in emerging markets like Asia-Pacific due to rising healthcare expenditure and growing diagnostic testing capabilities.

Diagnostic Flexible Packaging Industry Product Innovations

Recent innovations in diagnostic flexible packaging include the development of tamper-evident closures, improved barrier materials that enhance sample stability, and the integration of smart packaging technologies enabling real-time tracking and monitoring of samples. These advancements are crucial for maintaining sample integrity, reducing contamination risks, and improving overall efficiency in diagnostic workflows. The development of bio-based and biodegradable materials aligns with the industry's growing focus on sustainability. These innovations are gaining wider market acceptance, fueled by increasing healthcare expenditure and a heightened focus on infection control.

Report Segmentation & Scope

This report segments the diagnostic flexible packaging market comprehensively by both end-user and product type. Each segment is thoroughly analyzed for market size, growth projections, and competitive dynamics.

By End User:

- Hospitals: This segment is expected to experience a CAGR of XX% due to [reasons].

- Laboratories: Growth is projected at XX% due to [reasons].

- Academic Institutes: Anticipated growth of XX% due to [reasons].

- Other End Users: Projected CAGR of XX% due to [reasons].

By Product Type:

- Bottles: Market size in 2025 is $XX Million, with a projected CAGR of XX% driven by [reasons].

- Vials: The market is projected to grow at a CAGR of XX% reaching $XX Million in 2033.

- Tubes: This segment is expected to grow at a CAGR of XX% reaching $XX Million by 2033.

- Closures: Market size projected to be $XX Million in 2025, with a CAGR of XX%.

- Other Product Types: This segment is poised for growth at a CAGR of XX%, driven by innovation in specialized packaging solutions.

Key Drivers of Diagnostic Flexible Packaging Industry Growth

Several factors contribute to the growth of the diagnostic flexible packaging industry. These include the increasing prevalence of chronic diseases necessitating more diagnostic tests, stringent regulatory requirements driving the adoption of improved packaging solutions, technological advancements enabling efficient and cost-effective packaging, and rising healthcare expenditure globally. The growing adoption of point-of-care diagnostics also plays a vital role, requiring specialized packaging solutions. Furthermore, the rising focus on sustainability promotes the development and adoption of eco-friendly packaging materials.

Challenges in the Diagnostic Flexible Packaging Industry Sector

The diagnostic flexible packaging industry faces challenges such as fluctuating raw material prices, stringent regulatory compliance requirements impacting manufacturing costs, and intense competition among existing players. Supply chain disruptions can significantly impact production and delivery timelines, creating uncertainties for manufacturers. Maintaining consistent product quality and sterility is crucial, while the need to meet ever-evolving environmental regulations and consumer preferences for sustainable packaging poses further challenges for manufacturers to overcome.

Leading Players in the Diagnostic Flexible Packaging Industry Market

- DWK Life Sciences

- COMAR LLC

- Thermo Fisher Scientific Incorporated

- Aptargroup Incorporated

- Greiner Holding AG

- WS Packaging Group

- Amcor Limited

- Corning Incorporated

Key Developments in Diagnostic Flexible Packaging Industry Sector

- January 2023: Amcor launched a new range of sustainable flexible packaging solutions for diagnostic applications.

- July 2022: Aptargroup acquired a smaller packaging company specializing in sterile packaging solutions for diagnostics. (Hypothetical example)

- October 2021: Thermo Fisher Scientific introduced a new automated packaging system for improved efficiency in diagnostic laboratories. (Hypothetical example)

Strategic Diagnostic Flexible Packaging Industry Market Outlook

The diagnostic flexible packaging market holds significant future potential, driven by continuous technological advancements, growing demand for advanced diagnostic solutions, and increasing healthcare spending. Strategic opportunities exist for manufacturers who can focus on developing sustainable and innovative packaging solutions that meet the evolving needs of the healthcare industry. Companies that invest in R&D, prioritize sustainability, and establish robust supply chains are well-positioned for success in this rapidly growing market.

Diagnostic Flexible Packaging Industry Segmentation

-

1. Product

- 1.1. Bottles

- 1.2. Vials

- 1.3. Tubes

- 1.4. Closures

- 1.5. Other Product Types

-

2. End User

- 2.1. Hospitals

- 2.2. Laboratories

- 2.3. Academic Institutes

- 2.4. Other End Users

Diagnostic Flexible Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

Diagnostic Flexible Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Growing Demand for Tubes; Increasing Number of Point-of-care Tests

- 3.3. Market Restrains

- 3.3.1. ; Environmental Concerns Related to Raw Materials for Packaging

- 3.4. Market Trends

- 3.4.1. Laboratories Segment to Witness High Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Bottles

- 5.1.2. Vials

- 5.1.3. Tubes

- 5.1.4. Closures

- 5.1.5. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Laboratories

- 5.2.3. Academic Institutes

- 5.2.4. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Bottles

- 6.1.2. Vials

- 6.1.3. Tubes

- 6.1.4. Closures

- 6.1.5. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Laboratories

- 6.2.3. Academic Institutes

- 6.2.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Europe Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Bottles

- 7.1.2. Vials

- 7.1.3. Tubes

- 7.1.4. Closures

- 7.1.5. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Laboratories

- 7.2.3. Academic Institutes

- 7.2.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Asia Pacific Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Bottles

- 8.1.2. Vials

- 8.1.3. Tubes

- 8.1.4. Closures

- 8.1.5. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Laboratories

- 8.2.3. Academic Institutes

- 8.2.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Latin America Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Bottles

- 9.1.2. Vials

- 9.1.3. Tubes

- 9.1.4. Closures

- 9.1.5. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals

- 9.2.2. Laboratories

- 9.2.3. Academic Institutes

- 9.2.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Bottles

- 10.1.2. Vials

- 10.1.3. Tubes

- 10.1.4. Closures

- 10.1.5. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals

- 10.2.2. Laboratories

- 10.2.3. Academic Institutes

- 10.2.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. North America Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East Diagnostic Flexible Packaging Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 DWK Life Sciences*List Not Exhaustive

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 COMAR LLC

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Thermo Fisher Scientific Incorporated

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Aptargroup Incorporated

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Greiner Holding AG

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 WS Packaging Group

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Amcor Limited

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Corning Incorporated

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.1 DWK Life Sciences*List Not Exhaustive

List of Figures

- Figure 1: Global Diagnostic Flexible Packaging Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Diagnostic Flexible Packaging Industry Revenue (Million), by Product 2024 & 2032

- Figure 13: North America Diagnostic Flexible Packaging Industry Revenue Share (%), by Product 2024 & 2032

- Figure 14: North America Diagnostic Flexible Packaging Industry Revenue (Million), by End User 2024 & 2032

- Figure 15: North America Diagnostic Flexible Packaging Industry Revenue Share (%), by End User 2024 & 2032

- Figure 16: North America Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Diagnostic Flexible Packaging Industry Revenue (Million), by Product 2024 & 2032

- Figure 19: Europe Diagnostic Flexible Packaging Industry Revenue Share (%), by Product 2024 & 2032

- Figure 20: Europe Diagnostic Flexible Packaging Industry Revenue (Million), by End User 2024 & 2032

- Figure 21: Europe Diagnostic Flexible Packaging Industry Revenue Share (%), by End User 2024 & 2032

- Figure 22: Europe Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Diagnostic Flexible Packaging Industry Revenue (Million), by Product 2024 & 2032

- Figure 25: Asia Pacific Diagnostic Flexible Packaging Industry Revenue Share (%), by Product 2024 & 2032

- Figure 26: Asia Pacific Diagnostic Flexible Packaging Industry Revenue (Million), by End User 2024 & 2032

- Figure 27: Asia Pacific Diagnostic Flexible Packaging Industry Revenue Share (%), by End User 2024 & 2032

- Figure 28: Asia Pacific Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Latin America Diagnostic Flexible Packaging Industry Revenue (Million), by Product 2024 & 2032

- Figure 31: Latin America Diagnostic Flexible Packaging Industry Revenue Share (%), by Product 2024 & 2032

- Figure 32: Latin America Diagnostic Flexible Packaging Industry Revenue (Million), by End User 2024 & 2032

- Figure 33: Latin America Diagnostic Flexible Packaging Industry Revenue Share (%), by End User 2024 & 2032

- Figure 34: Latin America Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Latin America Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East Diagnostic Flexible Packaging Industry Revenue (Million), by Product 2024 & 2032

- Figure 37: Middle East Diagnostic Flexible Packaging Industry Revenue Share (%), by Product 2024 & 2032

- Figure 38: Middle East Diagnostic Flexible Packaging Industry Revenue (Million), by End User 2024 & 2032

- Figure 39: Middle East Diagnostic Flexible Packaging Industry Revenue Share (%), by End User 2024 & 2032

- Figure 40: Middle East Diagnostic Flexible Packaging Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East Diagnostic Flexible Packaging Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 3: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 4: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Diagnostic Flexible Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Diagnostic Flexible Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Diagnostic Flexible Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Diagnostic Flexible Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Diagnostic Flexible Packaging Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 16: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 17: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 19: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 20: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 22: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 23: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 25: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 26: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 28: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 29: Global Diagnostic Flexible Packaging Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diagnostic Flexible Packaging Industry?

The projected CAGR is approximately 4.50%.

2. Which companies are prominent players in the Diagnostic Flexible Packaging Industry?

Key companies in the market include DWK Life Sciences*List Not Exhaustive, COMAR LLC, Thermo Fisher Scientific Incorporated, Aptargroup Incorporated, Greiner Holding AG, WS Packaging Group, Amcor Limited, Corning Incorporated.

3. What are the main segments of the Diagnostic Flexible Packaging Industry?

The market segments include Product, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Growing Demand for Tubes; Increasing Number of Point-of-care Tests.

6. What are the notable trends driving market growth?

Laboratories Segment to Witness High Growth.

7. Are there any restraints impacting market growth?

; Environmental Concerns Related to Raw Materials for Packaging.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diagnostic Flexible Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diagnostic Flexible Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diagnostic Flexible Packaging Industry?

To stay informed about further developments, trends, and reports in the Diagnostic Flexible Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence