Key Insights

The global Cloud Optimization Service market is poised for significant expansion, projected to reach a market size of $20 billion in 2025. This growth is fueled by an impressive CAGR of 15% over the forecast period, indicating robust demand for services that enhance cloud efficiency and cost-effectiveness. As organizations increasingly migrate their operations to the cloud, the complexities of managing cloud infrastructure, optimizing costs, and ensuring optimal performance become paramount. This drives the adoption of specialized cloud optimization services, designed to address these challenges by leveraging advanced tools and expertise. Key segments such as Cloud Cost Optimization and Cloud Architecture Optimization are expected to witness substantial uptake. Industries like BFSI and Telecommunications, with their extensive cloud footprints and critical data management needs, are leading the charge in adopting these services. The escalating need to reduce cloud spend without compromising on performance or security, coupled with the growing adoption of multi-cloud and hybrid cloud strategies, are the primary growth enablers.

Cloud Optimization Service Market Size (In Billion)

The market is further propelled by emerging trends such as the increasing use of AI and machine learning for automated cloud resource management and predictive cost analysis. The continuous evolution of cloud technologies and the demand for scalable, resilient, and cost-efficient cloud solutions underscore the vital role of cloud optimization. While the market exhibits strong growth potential, certain restraints such as the perceived complexity of implementation and a shortage of skilled professionals in cloud optimization might pose minor challenges. However, the overarching benefits of improved operational efficiency, enhanced security postures, and significant cost savings are expected to outweigh these concerns, driving sustained market expansion across major regions like North America, Europe, and Asia Pacific. Leading companies in this space are investing in innovative solutions and strategic partnerships to capture a larger market share.

Cloud Optimization Service Company Market Share

Cloud Optimization Service Market Report: Unlocking Billion-Dollar Opportunities in Cloud Efficiency

This comprehensive report delivers an in-depth analysis of the Cloud Optimization Service market, forecast to reach over $300 billion by 2033. Spanning the study period of 2019–2033, with a base year of 2025 and an estimated year of 2025, this report leverages historical data from 2019–2024 to provide unparalleled insights into market dynamics. Targeted at IT leaders, cloud strategists, finance professionals, and technology investors, this report unpacks the critical factors driving cloud cost optimization and cloud architecture optimization across the BFSI, Telecommunications, and Other industry segments. Discover how leading companies like Amazon CloudWatch, CloudZero, Apptio Cloudability, and Virtana are shaping the future of cloud efficiency.

Cloud Optimization Service Market Structure & Competitive Dynamics

The Cloud Optimization Service market is characterized by a dynamic and evolving structure, showcasing moderate to high market concentration in specific niches, while remaining highly fragmented in others. Innovation ecosystems are flourishing, fueled by the rapid advancement of cloud technologies and the increasing demand for sophisticated cost management and performance tuning solutions. Regulatory frameworks, particularly concerning data privacy and compliance, exert a significant influence, shaping the adoption and deployment of cloud optimization strategies. Product substitutes, while present in the form of in-house development or basic cloud provider tools, often fall short of the comprehensive capabilities offered by specialized cloud optimization services. End-user trends are overwhelmingly skewed towards enhanced efficiency, reduced operational expenditure, and improved application performance, driving substantial market penetration. Mergers and acquisitions (M&A) activities are on the rise, with deal values projected to reach over $70 billion during the forecast period, indicating a strong consolidation trend as larger players acquire innovative startups to expand their service portfolios and market reach. The market share of key players is continuously shifting, with leaders in cloud cost optimization and cloud architecture optimization solidifying their positions.

Cloud Optimization Service Industry Trends & Insights

The Cloud Optimization Service market is experiencing robust growth, driven by an escalating need for efficient cloud resource management and performance enhancement. The compound annual growth rate (CAGR) is projected to be approximately 18% over the forecast period. Key market growth drivers include the massive migration of enterprises to cloud environments, the increasing complexity of multi-cloud and hybrid cloud deployments, and the persistent pressure to control escalating cloud expenditure. Technological disruptions, such as the advent of AI-powered cost anomaly detection and automated rightsizing recommendations, are revolutionizing the way organizations manage their cloud infrastructure. Consumer preferences are shifting towards proactive, intelligent, and integrated cloud management solutions that offer end-to-end visibility and control. Competitive dynamics are intensifying, with a clear distinction emerging between providers offering basic cost reporting and those delivering advanced cloud architecture optimization, performance tuning, and security posture management. Market penetration is rapidly increasing across all sectors, with the BFSI and Telecommunications industries leading the charge due to their substantial cloud investments and stringent operational requirements. The overall market size is expected to exceed $300 billion by 2033.

Dominant Markets & Segments in Cloud Optimization Service

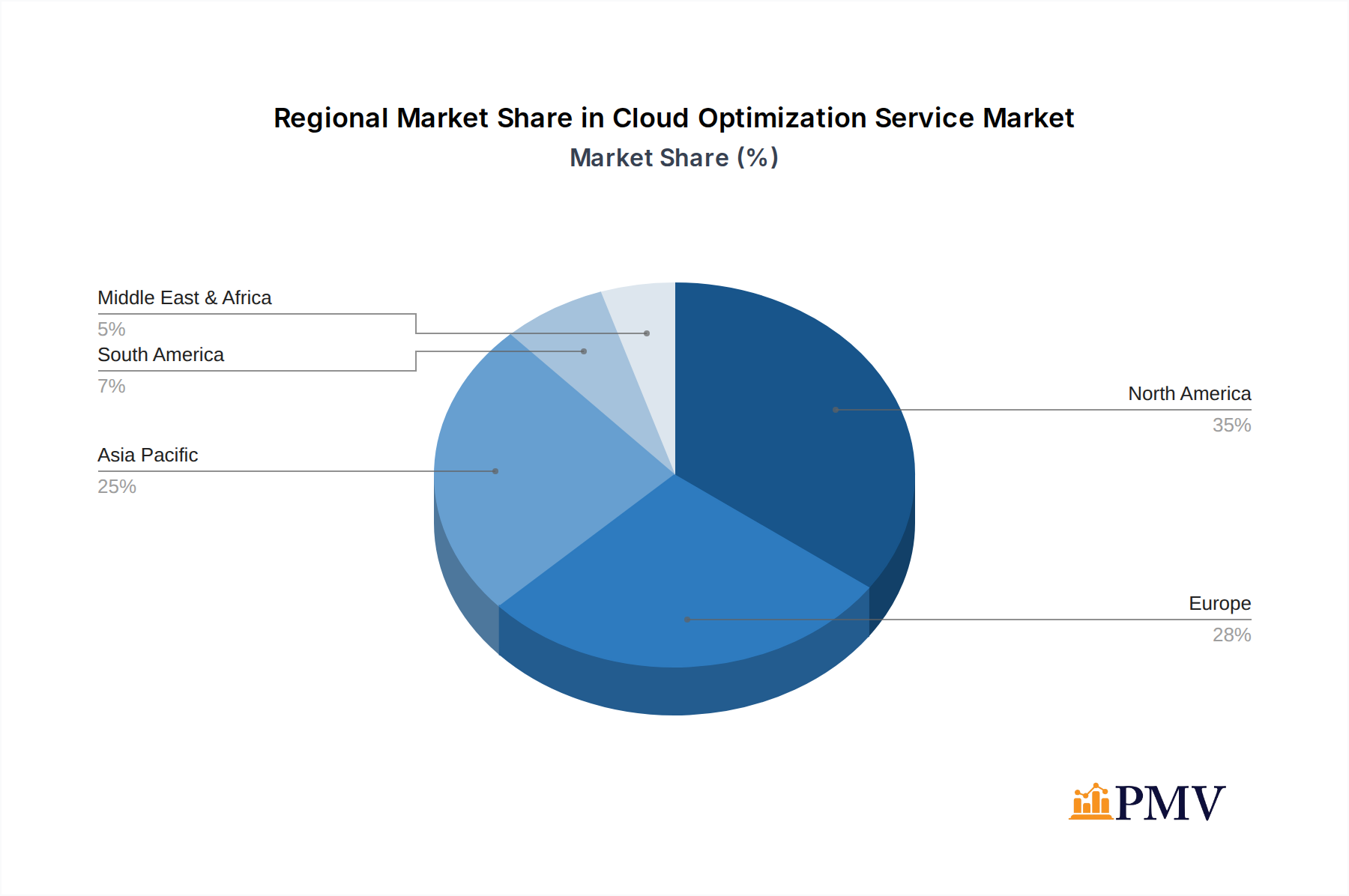

The Cloud Optimization Service market exhibits distinct regional and segmental dominance. North America currently leads in market share, driven by early cloud adoption, a mature technology landscape, and a high concentration of large enterprises in sectors like BFSI and Telecommunications. Economic policies favoring digital transformation and significant investments in cloud infrastructure further bolster this dominance. Asia-Pacific is emerging as a rapidly growing market, fueled by increasing cloud adoption in developing economies and government initiatives promoting digital infrastructure.

Application Segments:

- BFSI: This sector is a primary driver of the Cloud Optimization Service market. High transaction volumes, sensitive data, stringent regulatory compliance (e.g., GDPR, CCPA), and the imperative for high availability and low latency necessitate sophisticated cloud cost optimization and robust cloud architecture optimization. Financial institutions are actively seeking solutions to manage complex IT environments, optimize spending on critical applications, and ensure compliance, driving an estimated market share of over $80 billion in this segment by 2033.

- Telecommunications: The telecommunications industry, with its massive infrastructure and growing reliance on cloud-native architectures for services like 5G and IoT, is another significant contributor. They require advanced cloud architecture optimization to ensure scalability, performance, and cost-effectiveness. The demand for real-time data processing and network function virtualization (NFV) further amplifies the need for expert cloud optimization, contributing an estimated $60 billion to the market by 2033.

- Others: This broad segment encompasses various industries like healthcare, retail, manufacturing, and government. While individually smaller, their collective adoption of cloud services for digital transformation, data analytics, and customer engagement represents a substantial and growing portion of the market, projected to contribute over $160 billion by 2033.

Type Segments:

- Cloud Cost Optimization: This remains the most dominant type of service, addressing the immediate concern of runaway cloud spend. It encompasses FinOps practices, rightsizing, reserved instance management, and anomaly detection, with an estimated market size of over $180 billion by 2033.

- Cloud Architecture Optimization: This segment is gaining significant traction as organizations mature in their cloud journey. It focuses on improving the design, performance, scalability, and resilience of cloud deployments. This includes refactoring applications, optimizing container orchestration, and implementing serverless architectures. This segment is projected to reach over $100 billion by 2033.

- Others: This segment includes services like cloud security optimization, cloud migration optimization, and cloud governance and compliance services, which are increasingly integrated with core optimization strategies.

Cloud Optimization Service Product Innovations

Recent product innovations in the Cloud Optimization Service market are centered on leveraging artificial intelligence and machine learning for predictive cost management and automated performance tuning. Companies are developing advanced dashboards that offer real-time, granular visibility into cloud spend and resource utilization. Furthermore, there's a growing emphasis on self-service capabilities, empowering IT teams to implement optimization recommendations with minimal manual intervention. These advancements enable more precise rightsizing of instances, intelligent scheduling of workloads, and proactive identification of cost-saving opportunities, creating significant competitive advantages for early adopters.

Report Segmentation & Scope

This report provides a granular segmentation of the Cloud Optimization Service market to offer tailored insights. The analysis covers market sizes and growth projections for key application segments: BFSI, Telecommunications, and Others. The BFSI segment is projected to exhibit a CAGR of approximately 17%, with a market size of over $80 billion by 2033, driven by regulatory compliance and data security needs. The Telecommunications segment is expected to grow at a CAGR of over 19%, reaching $60 billion by 2033, due to the demands of 5G and network modernization. The "Others" segment, encompassing a wide array of industries, is projected to grow at a CAGR of around 18%, contributing over $160 billion. In terms of service types, Cloud Cost Optimization is forecast to reach over $180 billion, while Cloud Architecture Optimization is expected to surpass $100 billion by 2033, with "Others" encompassing specialized services.

Key Drivers of Cloud Optimization Service Growth

The explosive growth in the Cloud Optimization Service market is propelled by a confluence of powerful drivers. The pervasive digital transformation initiatives across industries are leading to significant cloud adoption, necessitating effective management of these complex environments. Escalating cloud expenditures, driven by increased usage and evolving service offerings, are creating immense pressure on organizations to control costs. Technological advancements, particularly in AI and ML, are enabling more intelligent and automated optimization solutions. Furthermore, the increasing complexity of multi-cloud and hybrid cloud strategies demands specialized expertise and tools for seamless integration and management. Regulatory compliance mandates in sectors like BFSI also play a crucial role, pushing organizations to ensure their cloud deployments are secure, efficient, and compliant.

Challenges in the Cloud Optimization Service Sector

Despite its strong growth trajectory, the Cloud Optimization Service sector faces several challenges. The sheer complexity of cloud environments, particularly multi-cloud and hybrid setups, can be overwhelming, making it difficult to achieve comprehensive visibility and control. A significant talent gap exists in skilled cloud optimization professionals, hindering organizations' ability to leverage these services effectively. Resistance to change within organizations and the perceived upfront investment required for optimization tools can also act as barriers. Furthermore, the rapid pace of cloud innovation means that optimization strategies must constantly adapt, presenting an ongoing challenge for both service providers and end-users.

Leading Players in the Cloud Optimization Service Market

- Amazon CloudWatch

- CloudZero

- Apptio Cloudability

- BMC Helix ITSM

- Virtana

- Cuelogic

- Logicworks

- IT Outposts

- Avahi Technologies

- CloudHealth by VMware

- Opsani

- Trianz

- TecBrix

- Zesty

Key Developments in Cloud Optimization Service Sector

- 2023 (Q4): Launch of AI-driven anomaly detection tools by several key players, significantly improving proactive cost management capabilities.

- 2024 (Q1): Increased M&A activity, with significant acquisitions aimed at bolstering platform integration and expanding service offerings in cloud architecture optimization.

- 2024 (Q2): Growing emphasis on FinOps frameworks and certifications, driving demand for specialized training and consulting services.

- 2024 (Q3): Introduction of advanced serverless optimization solutions, catering to the rising adoption of event-driven architectures.

- 2024 (Q4): Enhanced focus on sustainability in cloud operations, with optimization services increasingly incorporating carbon footprint reduction metrics.

Strategic Cloud Optimization Service Market Outlook

The strategic outlook for the Cloud Optimization Service market is exceptionally bright. The sustained migration to cloud environments, coupled with the ongoing digital transformation imperative, ensures a continuous and growing demand for efficient cloud management. Future growth accelerators will include the deeper integration of AI and ML for predictive analytics and autonomous optimization, the expansion of specialized services for emerging cloud-native technologies like Kubernetes and microservices, and the increasing adoption of FinOps as a core business practice. The growing awareness of sustainability in cloud computing will also create new opportunities for optimization services that prioritize environmental impact alongside cost and performance. Organizations that proactively invest in robust cloud optimization strategies will gain a significant competitive advantage through reduced operational costs, enhanced agility, and improved overall business performance, positioning the market for continued multi-billion-dollar expansion.

Cloud Optimization Service Segmentation

-

1. Application

- 1.1. BFSI

- 1.2. Telecommunications

- 1.3. Others

-

2. Types

- 2.1. Cloud Cost Optimization

- 2.2. Cloud Architecture Optimization

- 2.3. Others

Cloud Optimization Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Optimization Service Regional Market Share

Geographic Coverage of Cloud Optimization Service

Cloud Optimization Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.73% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. BFSI

- 5.1.2. Telecommunications

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud Cost Optimization

- 5.2.2. Cloud Architecture Optimization

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. BFSI

- 6.1.2. Telecommunications

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud Cost Optimization

- 6.2.2. Cloud Architecture Optimization

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. BFSI

- 7.1.2. Telecommunications

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud Cost Optimization

- 7.2.2. Cloud Architecture Optimization

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. BFSI

- 8.1.2. Telecommunications

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud Cost Optimization

- 8.2.2. Cloud Architecture Optimization

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. BFSI

- 9.1.2. Telecommunications

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud Cost Optimization

- 9.2.2. Cloud Architecture Optimization

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cloud Optimization Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. BFSI

- 10.1.2. Telecommunications

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud Cost Optimization

- 10.2.2. Cloud Architecture Optimization

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Amazon CloudWatch

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 CloudZero

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Apptio Cloudability

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BMC Helix ITSM

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Virtana

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cuelogic

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Logicworks

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 IT Outposts

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Avahi Technologies

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 CloudHealth by Vmware

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Opsani

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Trianz

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 TecBrix

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zesty

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Amazon CloudWatch

List of Figures

- Figure 1: Global Cloud Optimization Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cloud Optimization Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cloud Optimization Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cloud Optimization Service Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Cloud Optimization Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cloud Optimization Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cloud Optimization Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cloud Optimization Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cloud Optimization Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cloud Optimization Service Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Cloud Optimization Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cloud Optimization Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cloud Optimization Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cloud Optimization Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cloud Optimization Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cloud Optimization Service Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Cloud Optimization Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cloud Optimization Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cloud Optimization Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cloud Optimization Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cloud Optimization Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cloud Optimization Service Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cloud Optimization Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cloud Optimization Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cloud Optimization Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cloud Optimization Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cloud Optimization Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cloud Optimization Service Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Cloud Optimization Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cloud Optimization Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cloud Optimization Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Cloud Optimization Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Cloud Optimization Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Cloud Optimization Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Cloud Optimization Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Cloud Optimization Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cloud Optimization Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cloud Optimization Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Cloud Optimization Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cloud Optimization Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud Optimization Service?

The projected CAGR is approximately 23.73%.

2. Which companies are prominent players in the Cloud Optimization Service?

Key companies in the market include Amazon CloudWatch, CloudZero, Apptio Cloudability, BMC Helix ITSM, Virtana, Cuelogic, Logicworks, IT Outposts, Avahi Technologies, CloudHealth by Vmware, Opsani, Trianz, TecBrix, Zesty.

3. What are the main segments of the Cloud Optimization Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud Optimization Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud Optimization Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud Optimization Service?

To stay informed about further developments, trends, and reports in the Cloud Optimization Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence