Key Insights

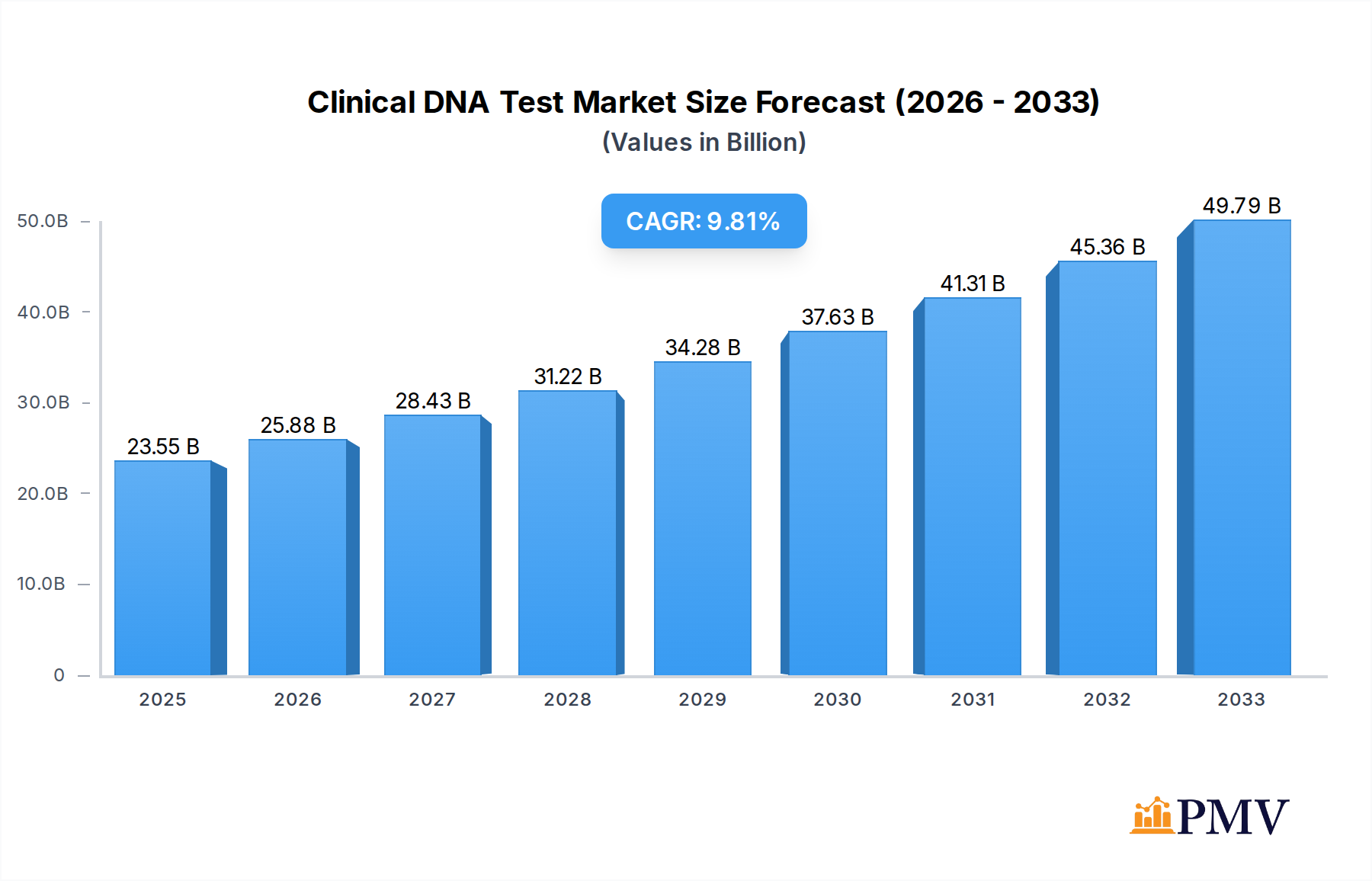

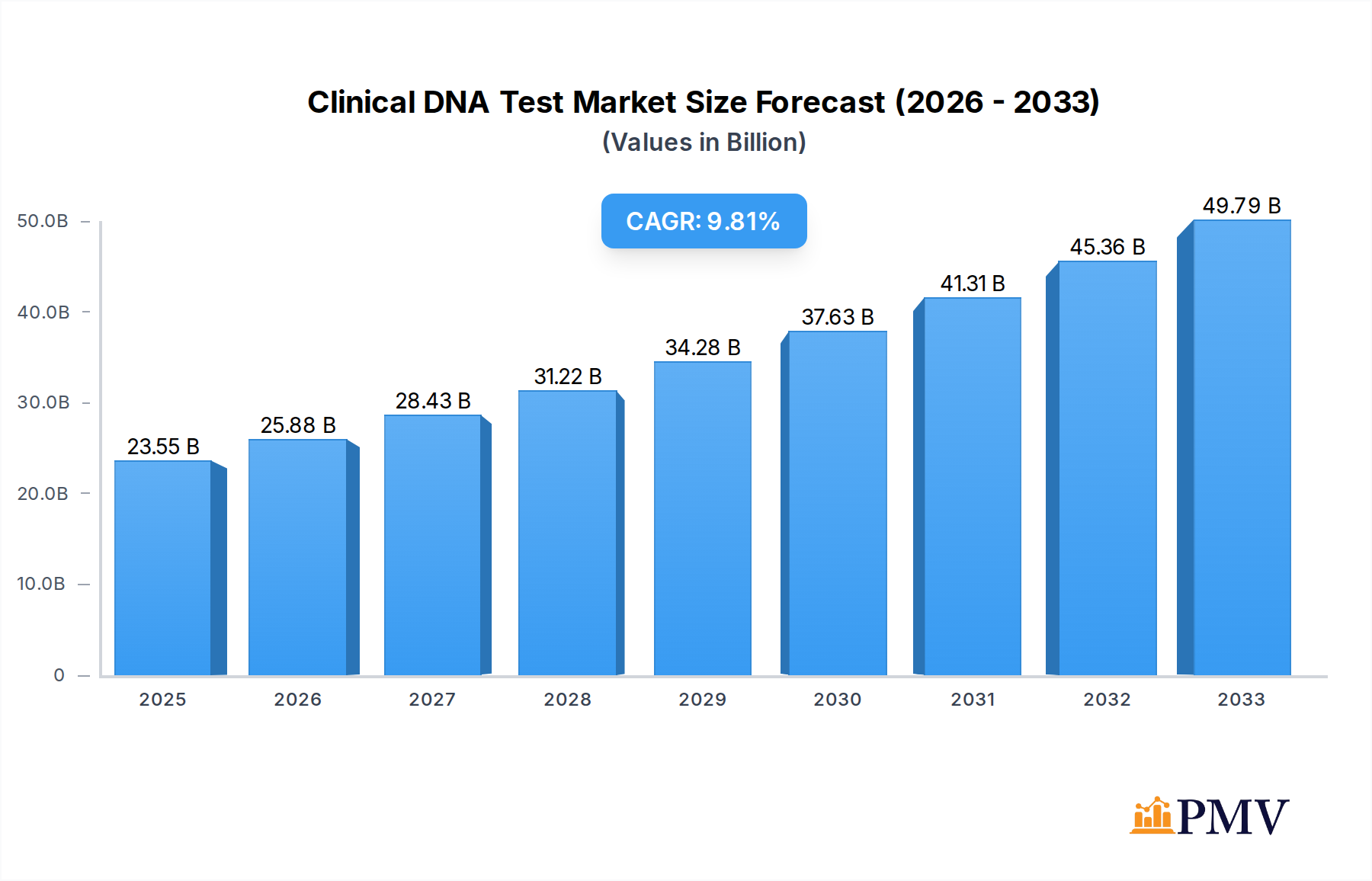

The Clinical DNA Test market is poised for significant expansion, projected to reach an estimated $23.55 billion in 2025. This robust growth is fueled by an impressive Compound Annual Growth Rate (CAGR) of 9.79% throughout the forecast period. Several key drivers are propelling this upward trajectory. Increasing awareness among healthcare professionals and the general public regarding the benefits of genetic testing for early disease detection and personalized treatment is a primary catalyst. Advances in DNA sequencing technologies, leading to reduced costs and increased accuracy, are making these tests more accessible. Furthermore, the growing prevalence of genetic disorders and chronic diseases, such as cancer, cardiovascular conditions, and inherited diseases, is creating a sustained demand for diagnostic solutions. The expanding applications within prenatal screening, full cycle cancer screening, and microbial detection further solidify the market's expansive potential, enabling more targeted and effective healthcare interventions.

Clinical DNA Test Market Size (In Billion)

The market's dynamic nature is further shaped by evolving trends and critical restraints. The increasing integration of genetic testing into routine clinical practice and the rising adoption of next-generation sequencing (NGS) technologies are significant trends. The growing focus on precision medicine and the development of companion diagnostics for targeted therapies are also key growth enablers. However, challenges such as stringent regulatory frameworks, concerns regarding data privacy and security, and the high cost of advanced genetic testing for certain applications remain as important restraints. Despite these hurdles, the expanding healthcare infrastructure, particularly in emerging economies, and increased research and development activities by leading companies like Illumina, BGI Genomics, and Agilent Technologies, are expected to drive continued market penetration and innovation. The segmentation of the market into various applications and types, along with a wide geographical reach, indicates a diverse and competitive landscape.

Clinical DNA Test Company Market Share

This in-depth report provides a definitive analysis of the global Clinical DNA Test market, offering critical insights for stakeholders seeking to navigate this rapidly evolving landscape. Spanning the historical period of 2019–2024, the base year of 2025, and extending to a forecast period through 2033, this report leverages extensive data to project market trajectories, identify growth drivers, and pinpoint emerging opportunities. With a projected market size in the billions, this study is essential for understanding the technological advancements, application expansions, and competitive strategies shaping the future of clinical diagnostics.

Clinical DNA Test Market Structure & Competitive Dynamics

The Clinical DNA Test market exhibits a moderately consolidated structure, characterized by the presence of established global players and emerging regional innovators. Key players like Illumina, BGI Genomics Co., Ltd., and Agilent Technologies command significant market share, driven by extensive R&D investment and robust product portfolios. The innovation ecosystem thrives on collaborations between academic institutions, diagnostic laboratories, and technology providers, fostering a dynamic environment for developing next-generation sequencing (NGS) and other DNA analysis technologies. Regulatory frameworks, while varied across regions, are increasingly focused on ensuring data privacy, test accuracy, and ethical applications, influencing market entry and product approval processes. Potential product substitutes, though limited in direct clinical application, include traditional diagnostic methods; however, the precision and comprehensiveness of DNA testing offer distinct advantages. End-user trends reveal a growing demand for personalized medicine, proactive health management, and early disease detection, propelling the adoption of clinical DNA tests in diverse healthcare settings. Mergers and acquisitions (M&A) activities, valued in the billions, continue to reshape the competitive landscape, as larger entities seek to acquire innovative technologies and expand their market reach. For instance, strategic acquisitions have historically accounted for over $50 billion in deal values, indicating a strong trend towards consolidation and synergistic growth. The market share distribution sees major players holding approximately 70% of the global market.

Clinical DNA Test Industry Trends & Insights

The Clinical DNA Test industry is experiencing robust growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 15% over the forecast period (2025–2033). This expansion is fueled by a confluence of factors, including increasing awareness of genetic predispositions to diseases, a rising prevalence of chronic and rare genetic disorders, and the escalating demand for personalized treatment strategies. Technological disruptions are at the forefront, with advancements in next-generation sequencing (NGS) technologies dramatically reducing costs and turnaround times, making DNA testing more accessible. The development of liquid biopsy techniques, for example, has revolutionized cancer screening and monitoring, offering non-invasive alternatives to traditional biopsies and contributing to a market penetration rate that has surpassed 40% in developed nations for specific applications. Consumer preferences are shifting towards proactive health management, with individuals increasingly seeking genetic information to understand their health risks and make informed lifestyle choices. This trend is evidenced by the substantial growth in direct-to-consumer (DTC) genetic testing, which often serves as a gateway to clinical applications. Competitive dynamics are intensifying, characterized by strategic partnerships, product differentiation, and aggressive market penetration strategies by leading companies. The increasing integration of artificial intelligence (AI) and machine learning (ML) in data analysis is further enhancing the diagnostic accuracy and predictive capabilities of clinical DNA tests, creating new avenues for market expansion. The total addressable market is estimated to reach over $100 billion by 2033.

Dominant Markets & Segments in Clinical DNA Test

The Hospital application segment is the undisputed leader in the Clinical DNA Test market, commanding an estimated market share of 60% in 2025. This dominance is driven by the critical role hospitals play in patient diagnosis, treatment, and management, where DNA testing is increasingly integrated into routine clinical practice. Key drivers for this segment include favorable reimbursement policies for diagnostic procedures, the growing complexity of patient cases requiring precise genetic information, and the continuous adoption of advanced laboratory infrastructure within hospital settings. Economically, governments and healthcare providers are investing billions in genomic medicine initiatives, further bolstering hospital-based testing.

Within the Types segmentation, Diagnosis and Treatment represents the largest and fastest-growing segment, projected to account for over 40% of the market by 2033. This segment encompasses a broad spectrum of applications, including the identification of genetic mutations for targeted therapies, pharmacogenomics to optimize drug efficacy, and the diagnosis of inherited disorders. The increasing precision of genetic diagnostics allows for tailored treatment plans, leading to improved patient outcomes and significant cost savings in the long run.

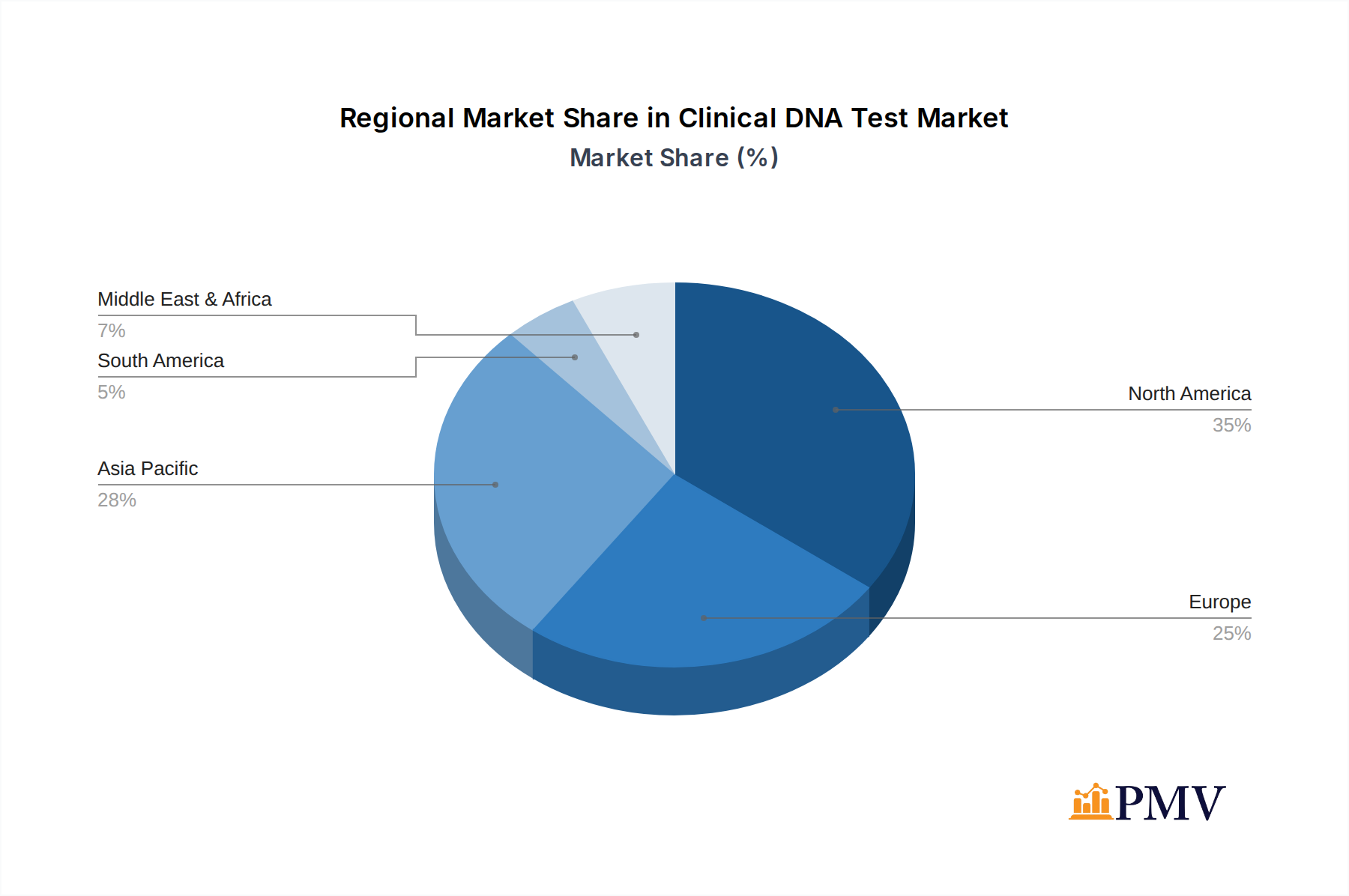

Geographically, North America currently holds the dominant market position, largely due to its advanced healthcare infrastructure, high R&D spending, and strong regulatory support for genomic research and clinical applications. The United States, in particular, is a hub for innovation and adoption, with substantial investments in personalized medicine and genetic screening programs. Economic policies promoting healthcare innovation and a well-established network of research institutions and biotechnology companies contribute to this regional leadership.

Clinical DNA Test Product Innovations

Product innovations in the Clinical DNA Test market are primarily focused on enhancing accuracy, reducing turnaround times, and expanding the scope of diagnostic capabilities. Advancements in microfluidics and digital PCR technologies are enabling more sensitive and specific detection of genetic markers, particularly in areas like prenatal screening and early cancer detection. The development of comprehensive genomic profiling platforms allows for the simultaneous analysis of multiple genes, providing a holistic view of a patient's genetic landscape. These innovations offer significant competitive advantages by enabling earlier and more precise diagnoses, thereby improving treatment efficacy and patient prognosis, with a projected market adoption rate of over 30% for novel assay types within five years.

Report Segmentation & Scope

The Clinical DNA Test market is comprehensively segmented across key applications and test types. The Hospital segment is projected to generate over $60 billion in revenue by 2033, driven by its central role in diagnostic pathways. The Centers for Disease Control and Prevention segment, though smaller, is crucial for public health surveillance and outbreak investigations, with expected growth driven by infectious disease monitoring. The Other segment, encompassing research institutions and private diagnostic labs, will also see steady growth.

In terms of test types, Prenatal Screening is a mature yet consistently growing segment, estimated at $15 billion by 2033, driven by the demand for non-invasive prenatal testing (NIPT). Full Cycle Cancer Screening is experiencing rapid expansion, fueled by advancements in early detection technologies and personalized oncology, expected to reach over $25 billion by 2033. Diagnosis and Treatment applications are the largest, as detailed previously, projected to exceed $40 billion. Genetic Disease Screening remains a fundamental area with stable growth, and Microbial Detection is gaining traction due to its applications in infectious disease diagnostics and microbiome research, with a projected market size of $10 billion.

Key Drivers of Clinical DNA Test Growth

The growth of the Clinical DNA Test market is propelled by several interconnected factors. Technological advancements, particularly in next-generation sequencing (NGS) and CRISPR gene editing, have dramatically improved test accuracy and affordability, enabling wider clinical adoption. The increasing prevalence of genetic and chronic diseases globally creates a sustained demand for diagnostic and therapeutic solutions. Growing awareness and acceptance of personalized medicine among patients and healthcare providers are driving the uptake of DNA-based health assessments. Furthermore, supportive government initiatives and funding for genomic research and healthcare innovation, coupled with evolving reimbursement policies, are creating a conducive environment for market expansion, with billions invested annually in genomic infrastructure.

Challenges in the Clinical DNA Test Sector

Despite the robust growth, the Clinical DNA Test sector faces several challenges. High initial investment costs for sophisticated laboratory equipment and skilled personnel can be a barrier, particularly for smaller institutions. Regulatory hurdles and complexities in obtaining approvals for novel diagnostic tests across different jurisdictions can lead to significant delays and increased expenses, impacting market entry timelines. Data interpretation and privacy concerns remain critical issues, requiring robust ethical guidelines and secure data management systems. Additionally, the shortage of trained bioinformatics professionals capable of analyzing and interpreting complex genomic data poses a challenge to scalability. Competitive pressures from numerous market players can also lead to pricing pressures, impacting profit margins, with some segments experiencing over 30% price erosion for established tests.

Leading Players in the Clinical DNA Test Market

- Illumina

- BGI Genomics Co., Ltd.

- Agilent Technologies

- Macrogen

- Pacific Biosciences

- 10x Genomics

- QIAGEN

- GEEWIZ

- WeGene

- 23andMe

- Mega Genomics

- Berry Genomics

- CapitalBio Corp.

- Annaroad Gene Technology(Beijing)Co.,Ltd.

Key Developments in Clinical DNA Test Sector

- 2023 September: Illumina launched NovaSeq X Plus, a new sequencing platform offering unprecedented throughput and reduced cost per genome.

- 2023 August: BGI Genomics announced a strategic partnership with a leading European diagnostic network to expand its NGS testing services across the continent.

- 2023 July: Agilent Technologies acquired a specialized bioinformatics company to enhance its data analysis capabilities for clinical genomics.

- 2023 June: Pacific Biosciences received FDA clearance for a novel long-read sequencing assay for rare disease diagnosis.

- 2023 May: 10x Genomics introduced a new spatial multi-omics solution, enabling simultaneous analysis of DNA, RNA, and protein in tissue samples.

- 2023 April: QIAGEN expanded its portfolio of companion diagnostics with the launch of a new assay for lung cancer treatment selection.

- 2022 December: 23andMe announced a significant expansion of its research partnership with a major pharmaceutical company for drug discovery using its aggregated genetic data.

- 2022 November: Macrogen established a new clinical genomics laboratory in Southeast Asia to cater to the growing demand in the region.

Strategic Clinical DNA Test Market Outlook

The strategic outlook for the Clinical DNA Test market is overwhelmingly positive, characterized by sustained innovation and expanding applications. Growth accelerators include the increasing integration of artificial intelligence for advanced data analytics and diagnostic support, and the growing demand for liquid biopsy technologies in oncology and prenatal testing. The expansion of pharmacogenomics to personalize drug prescriptions will unlock significant value. Emerging markets in Asia-Pacific and Latin America present substantial untapped potential, driven by improving healthcare infrastructure and increasing disposable incomes. Strategic opportunities lie in developing cost-effective, point-of-care diagnostic solutions and forging deeper collaborations across the healthcare ecosystem to ensure seamless integration of genomic insights into patient care pathways, projecting a market expansion by over 70% in the next decade.

Clinical DNA Test Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Centers for Disease Control and Prevention

- 1.3. Other

-

2. Types

- 2.1. Prenatal Screening

- 2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 2.3. Genetic Disease Screening

- 2.4. Microbial Detection

Clinical DNA Test Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Clinical DNA Test Regional Market Share

Geographic Coverage of Clinical DNA Test

Clinical DNA Test REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Centers for Disease Control and Prevention

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Prenatal Screening

- 5.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 5.2.3. Genetic Disease Screening

- 5.2.4. Microbial Detection

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Centers for Disease Control and Prevention

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Prenatal Screening

- 6.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 6.2.3. Genetic Disease Screening

- 6.2.4. Microbial Detection

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Centers for Disease Control and Prevention

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Prenatal Screening

- 7.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 7.2.3. Genetic Disease Screening

- 7.2.4. Microbial Detection

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Centers for Disease Control and Prevention

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Prenatal Screening

- 8.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 8.2.3. Genetic Disease Screening

- 8.2.4. Microbial Detection

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Centers for Disease Control and Prevention

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Prenatal Screening

- 9.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 9.2.3. Genetic Disease Screening

- 9.2.4. Microbial Detection

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Clinical DNA Test Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Centers for Disease Control and Prevention

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Prenatal Screening

- 10.2.2. Full Cycle Cancer Screening, Diagnosis and Treatment

- 10.2.3. Genetic Disease Screening

- 10.2.4. Microbial Detection

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Illumina

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BGI Genomics Co.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ltd.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Agilent Technologies

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Macrogen

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Pacific Biosciences

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 10x Genomics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 QIAGEN

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 GEEWIZ

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 WeGene

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 23andMe

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Mega Genomics

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Berry Genomics

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CapitalBio Corp.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Annaroad Gene Technology(Beijing)Co.

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Ltd.

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Illumina

List of Figures

- Figure 1: Global Clinical DNA Test Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Clinical DNA Test Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Clinical DNA Test Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Clinical DNA Test Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Clinical DNA Test Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Clinical DNA Test Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Clinical DNA Test Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Clinical DNA Test Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Clinical DNA Test Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Clinical DNA Test Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Clinical DNA Test Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Clinical DNA Test Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Clinical DNA Test Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Clinical DNA Test Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Clinical DNA Test Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Clinical DNA Test Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Clinical DNA Test Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Clinical DNA Test Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Clinical DNA Test Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Clinical DNA Test Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Clinical DNA Test Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Clinical DNA Test Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Clinical DNA Test Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Clinical DNA Test Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Clinical DNA Test Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Clinical DNA Test Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Clinical DNA Test Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Clinical DNA Test Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Clinical DNA Test Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Clinical DNA Test Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Clinical DNA Test Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Clinical DNA Test Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Clinical DNA Test Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Clinical DNA Test Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Clinical DNA Test Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Clinical DNA Test Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Clinical DNA Test Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Clinical DNA Test Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Clinical DNA Test Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Clinical DNA Test Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Clinical DNA Test?

The projected CAGR is approximately 14.25%.

2. Which companies are prominent players in the Clinical DNA Test?

Key companies in the market include Illumina, BGI Genomics Co., Ltd., Agilent Technologies, Macrogen, Pacific Biosciences, 10x Genomics, QIAGEN, GEEWIZ, WeGene, 23andMe, Mega Genomics, Berry Genomics, CapitalBio Corp., Annaroad Gene Technology(Beijing)Co., Ltd..

3. What are the main segments of the Clinical DNA Test?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Clinical DNA Test," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Clinical DNA Test report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Clinical DNA Test?

To stay informed about further developments, trends, and reports in the Clinical DNA Test, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence