Key Insights

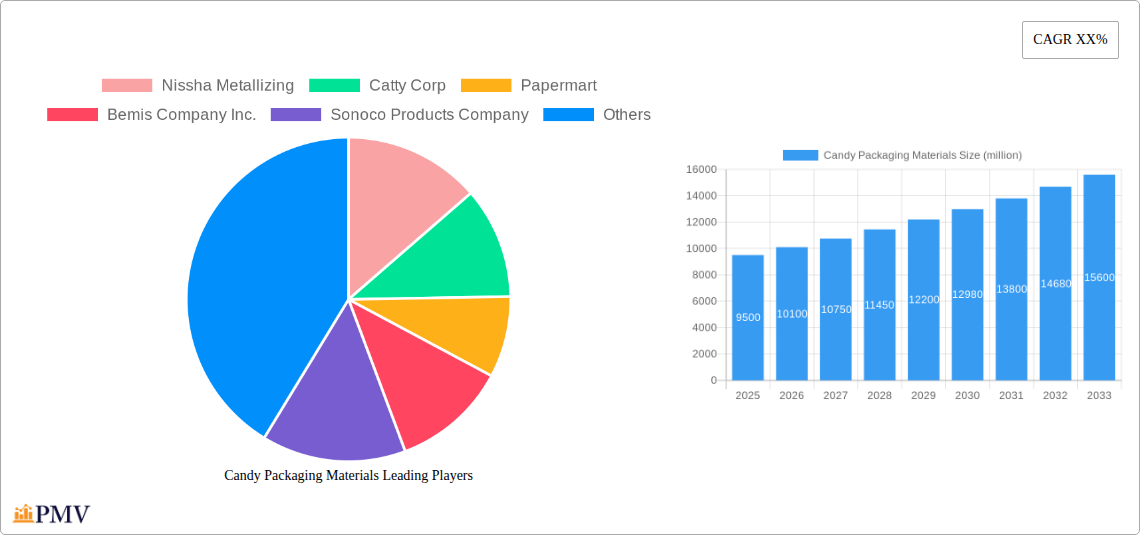

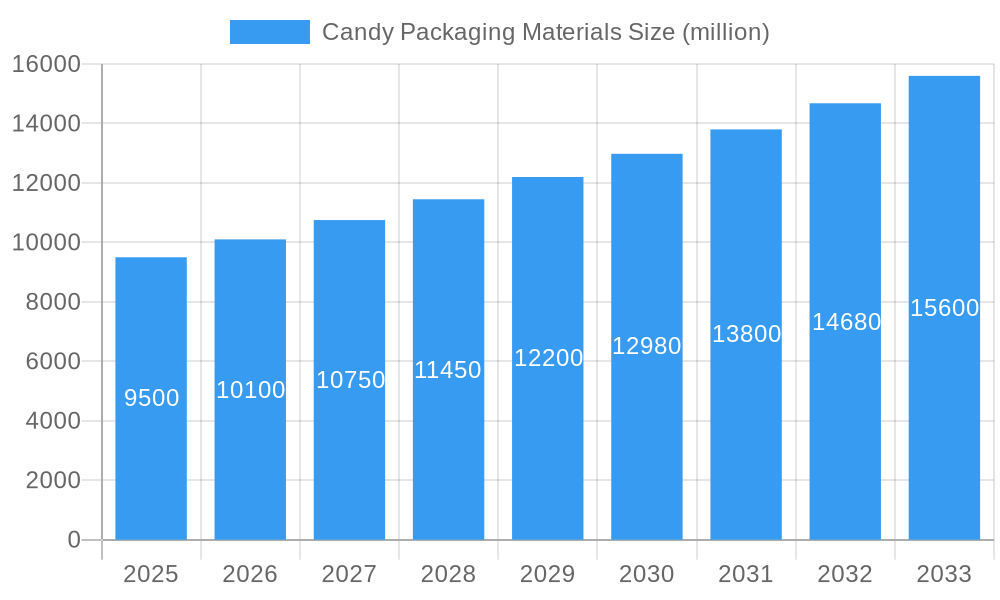

The global candy packaging materials market is poised for robust growth, projected to reach a substantial market size of approximately $9,500 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of around 6.5% during the forecast period of 2025-2033. This expansion is primarily fueled by the ever-increasing global demand for confectionery products, driven by impulse purchases, gifting occasions, and a growing consumer appetite for diverse and innovative candy options. The convenience and aesthetic appeal offered by advanced packaging materials play a crucial role in consumer choices, further bolstering market expansion. Key applications within this market include candy making, where specialized materials ensure product freshness and integrity, and food packaging, a broad segment encompassing everything from individual candy wrappers to larger promotional packaging. The "Others" segment is expected to encompass innovative and sustainable packaging solutions emerging in the market.

Candy Packaging Materials Market Size (In Billion)

The market is experiencing a dynamic shift influenced by evolving consumer preferences and technological advancements. Paper wrapping paper, valued for its eco-friendliness and premium feel, is gaining traction, especially for artisanal and premium confectionery. Plastic wrapping paper continues to dominate due to its cost-effectiveness, durability, and versatility in protecting candies. Aluminum foil wrapping paper remains essential for its excellent barrier properties, crucial for preserving the taste and texture of chocolates and other sensitive candies. Leading companies such as Amcor Limited, Bemis Company Inc., and WestRock Co. Inc. are at the forefront, investing in research and development to offer sustainable, functional, and visually appealing packaging solutions. While market growth is strong, potential restraints include rising raw material costs and increasing environmental regulations on single-use plastics, pushing manufacturers towards biodegradable and recyclable alternatives. The Asia Pacific region, particularly China and India, is expected to emerge as a significant growth engine due to a burgeoning middle class and high consumption rates of confectionery.

Candy Packaging Materials Company Market Share

Here is an SEO-optimized, detailed report description for Candy Packaging Materials, crafted without placeholders and ready for immediate use:

Candy Packaging Materials Market Structure & Competitive Dynamics

The global Candy Packaging Materials market is characterized by a moderate to high degree of concentration, with key players such as Amcor Limited, Sonoco Products Company, and Westrock co Inc. commanding significant market share. The innovation ecosystem is robust, driven by a continuous quest for sustainable solutions, enhanced shelf appeal, and improved product protection. Regulatory frameworks, particularly concerning food safety and environmental impact, play a crucial role in shaping market strategies and product development. The presence of readily available product substitutes, such as generic food wrapping, presents a constant challenge. End-user trends favor visually appealing, convenient, and eco-friendly packaging options. Mergers and acquisitions (M&A) are strategic tools for expansion and consolidation, with recent M&A deal values reaching several hundred million dollars. For instance, a hypothetical M&A deal involving a major plastic wrapping paper manufacturer and a paper wrapping paper producer might have a valuation in the range of $500 million to $1 billion. The market share distribution reveals that plastic wrapping paper and paper wrapping paper collectively hold over 80% of the market, with aluminum foil wrapping paper and other specialized materials making up the remainder. Companies are actively investing in R&D to develop biodegradable and compostable packaging solutions, aiming to capture a larger share of the eco-conscious consumer market.

Candy Packaging Materials Industry Trends & Insights

The Candy Packaging Materials industry is poised for significant growth, driven by a confluence of factors including rising disposable incomes, an expanding global confectionery market, and evolving consumer preferences. The projected Compound Annual Growth Rate (CAGR) for the forecast period (2025–2033) is estimated at 5.8%. Market penetration is increasing, especially in emerging economies where the demand for premium and convenience-oriented confectionery products is on the rise. Technological disruptions are transforming the landscape, with advancements in material science leading to the development of advanced barrier properties, enhanced printability, and smart packaging solutions that offer traceability and tamper-evidence. Consumer preferences are increasingly leaning towards sustainable and ethically sourced packaging. This trend is fueling the demand for recyclable, compostable, and biodegradable materials, forcing manufacturers to innovate and adapt their product portfolios. Companies are investing heavily in research and development to create packaging that not only protects the candy but also minimizes its environmental footprint. The visual appeal of candy packaging remains paramount, with manufacturers leveraging advanced printing techniques and innovative designs to capture consumer attention at the point of sale. The "clean label" movement also extends to packaging, with consumers seeking transparent and easily understandable material compositions. Furthermore, the growth of e-commerce has necessitated specialized packaging solutions that ensure product integrity during transit, leading to a surge in demand for robust and protective candy packaging materials. The industry is also witnessing a greater emphasis on personalized packaging, allowing brands to connect with consumers on a more individual level. This personalized approach, coupled with the increasing popularity of artisanal and premium confectionery, is creating new opportunities for specialized packaging material suppliers. The influence of social media trends and influencer marketing further amplifies the importance of visually striking and shareable packaging designs, contributing to overall market expansion.

Dominant Markets & Segments in Candy Packaging Materials

The Food Packaging application segment is currently the dominant force within the Candy Packaging Materials market, driven by the sheer volume of confectionery produced globally. Within this segment, Plastic Wrapping Paper holds the largest market share due to its versatility, cost-effectiveness, and excellent barrier properties, crucial for preserving candy freshness and extending shelf life.

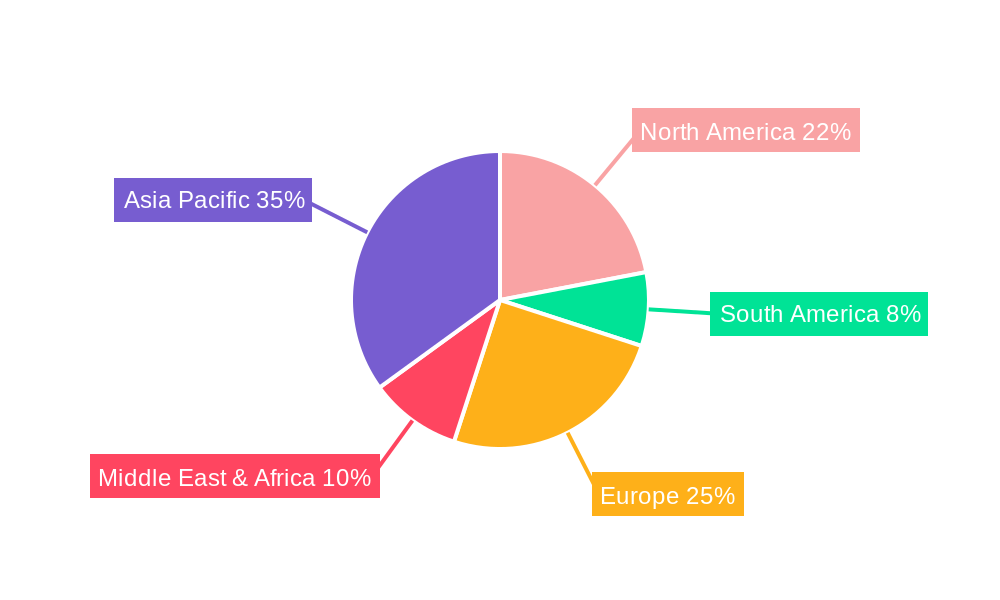

- Leading Region: North America is a dominant region, owing to its mature confectionery market, high disposable incomes, and strong consumer demand for premium and innovative candy products.

- Dominant Country: The United States leads in consumption and production of candy packaging materials, supported by a robust food manufacturing industry and a large consumer base.

- Dominant Application: Food Packaging accounts for an estimated 70% of the total market demand, with Candy Making a significant sub-segment within it.

- Dominant Type: Plastic Wrapping Paper, encompassing various polymers like polyethylene (PE) and polypropylene (PP), dominates due to its superior moisture barrier and flexibility, essential for diverse candy formats. The market share for plastic wrapping paper is approximately 55%.

- Key Drivers for Dominance:

- Economic Policies: Favorable trade policies and industrial growth initiatives in key regions stimulate manufacturing and consumption.

- Infrastructure: Well-developed logistics and supply chain networks ensure efficient distribution of raw materials and finished goods.

- Consumer Preferences: A strong demand for convenient, visually appealing, and shelf-stable confectionery products.

- Technological Advancements: Continuous innovation in plastic extrusion and film manufacturing enhances performance and sustainability.

The Candy Making application segment is a significant contributor, with an estimated market share of 25%, directly influenced by confectionery production volumes. Paper Wrapping Paper and Aluminum Foil Wrapping Paper are crucial for specific product types, offering distinct aesthetic and functional benefits. Paper wrapping paper, valued for its printability and eco-friendly perception, holds an estimated 25% market share, while aluminum foil wrapping paper, known for its exceptional barrier properties against light and moisture, captures approximately 15% of the market. The "Others" category, encompassing specialty films and coatings, represents the remaining market share, driven by niche applications and product innovations.

Candy Packaging Materials Product Innovations

Recent product innovations in candy packaging materials focus on enhancing sustainability, functionality, and consumer engagement. Development of biodegradable and compostable plastic alternatives, such as PLA (Polylactic Acid) films, is gaining traction, offering a reduced environmental footprint. Advancements in multi-layer film technology allow for improved oxygen and moisture barriers, extending shelf life for sensitive confectionery. Smart packaging solutions incorporating QR codes for product traceability and interactive consumer experiences are also emerging. These innovations provide competitive advantages by meeting evolving consumer demands for eco-conscious and engaging packaging.

Report Segmentation & Scope

This report segments the Candy Packaging Materials market based on Application and Type. The Application segments include Candy Making, Food Packaging, and Others. The Type segments are Paper Wrapping Paper, Plastic Wrapping Paper, Aluminum Foil Wrapping Paper, and Others. The Candy Making segment is projected to grow at a CAGR of 5.2% from 2025 to 2033, with an estimated market size of $4.5 billion in 2025. Food Packaging, as the dominant segment, is expected to reach $9.2 billion by 2025, growing at a CAGR of 6.1%. The Others application segment is projected to grow at 4.8% CAGR. For Types, Plastic Wrapping Paper is forecast to dominate with a market size of $7.8 billion in 2025 and a CAGR of 5.9%. Paper Wrapping Paper is estimated at $3.2 billion in 2025 with a 5.5% CAGR. Aluminum Foil Wrapping Paper is projected at $2.1 billion with a 4.9% CAGR. The Others type segment is expected to grow at 4.5% CAGR.

Key Drivers of Candy Packaging Materials Growth

The candy packaging materials market is propelled by several key drivers. Rising global demand for confectionery, fueled by growing middle-class populations and evolving consumer lifestyles, directly translates to increased packaging needs. Technological advancements in material science are enabling the creation of more sustainable, functional, and visually appealing packaging solutions, such as compostable films and high-barrier coatings. The growing consumer preference for premium and indulgence products necessitates packaging that enhances shelf appeal and brand perception. Furthermore, increasing regulatory pressures favoring eco-friendly and recyclable materials are spurring innovation and adoption of sustainable packaging alternatives.

Challenges in the Candy Packaging Materials Sector

Despite robust growth, the candy packaging materials sector faces several challenges. Fluctuations in the prices of raw materials, particularly polymers and paper pulp, can impact profit margins. Intense competition among a large number of manufacturers, including established giants like Amcor Limited and Bemis Company Inc., and emerging players, can lead to price wars and pressure on profitability. Stringent regulations regarding food contact materials and environmental sustainability require continuous investment in compliance and R&D for eco-friendly alternatives. Supply chain disruptions, exacerbated by geopolitical events and logistics bottlenecks, can lead to production delays and increased costs.

Leading Players in the Candy Packaging Materials Market

- Nissha Metallizing

- Catty Corp

- Papermart

- Bemis Company Inc.

- Sonoco Products Company

- Amcor Limited

- Silgan Holdings Inc.

- Westrock co Inc.

- Aptar Group

- Graham Packaging Company

Key Developments in Candy Packaging Materials Sector

- 2023 Q4: Amcor Limited launches a new line of fully recyclable flexible packaging for confectionery, enhancing sustainability.

- 2023 Q3: Sonoco Products Company invests in advanced recycling technology to increase the use of recycled content in their paperboard packaging.

- 2023 Q2: Bemis Company Inc. announces a strategic partnership to develop biodegradable films for snack and candy packaging.

- 2023 Q1: Westrock co Inc. expands its sustainable paper-based packaging solutions portfolio for the food and beverage industry.

- 2022 Q4: Aptar Group acquires a specialty packaging provider, strengthening its offerings in the confectionery market.

Strategic Candy Packaging Materials Market Outlook

The strategic outlook for the candy packaging materials market is exceptionally positive, driven by increasing demand for sustainable and innovative solutions. Growth accelerators include the rising popularity of artisanal and premium confectionery, which demands sophisticated and visually appealing packaging. The ongoing shift towards e-commerce presents opportunities for specialized, protective, and branded shipping solutions. Continuous innovation in bioplastics and advanced barrier films will cater to environmental consciousness and extended shelf-life requirements. Strategic collaborations and M&A activities are expected to continue as companies seek to expand their market reach, technological capabilities, and product portfolios to capture market share in this dynamic sector, with a projected total market value of over $15 billion by 2025.

Candy Packaging Materials Segmentation

-

1. Application

- 1.1. Candy Making

- 1.2. Food Packaging

- 1.3. Others

-

2. Types

- 2.1. Paper Wrapping Paper

- 2.2. Plastic Wrapping Paper

- 2.3. Aluminum Foil Wrapping Paper

- 2.4. Others

Candy Packaging Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Candy Packaging Materials Regional Market Share

Geographic Coverage of Candy Packaging Materials

Candy Packaging Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Candy Making

- 5.1.2. Food Packaging

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Paper Wrapping Paper

- 5.2.2. Plastic Wrapping Paper

- 5.2.3. Aluminum Foil Wrapping Paper

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Candy Packaging Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Candy Making

- 6.1.2. Food Packaging

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Paper Wrapping Paper

- 6.2.2. Plastic Wrapping Paper

- 6.2.3. Aluminum Foil Wrapping Paper

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Candy Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Candy Making

- 7.1.2. Food Packaging

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Paper Wrapping Paper

- 7.2.2. Plastic Wrapping Paper

- 7.2.3. Aluminum Foil Wrapping Paper

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Candy Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Candy Making

- 8.1.2. Food Packaging

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Paper Wrapping Paper

- 8.2.2. Plastic Wrapping Paper

- 8.2.3. Aluminum Foil Wrapping Paper

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Candy Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Candy Making

- 9.1.2. Food Packaging

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Paper Wrapping Paper

- 9.2.2. Plastic Wrapping Paper

- 9.2.3. Aluminum Foil Wrapping Paper

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Candy Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Candy Making

- 10.1.2. Food Packaging

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Paper Wrapping Paper

- 10.2.2. Plastic Wrapping Paper

- 10.2.3. Aluminum Foil Wrapping Paper

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Candy Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Candy Making

- 11.1.2. Food Packaging

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Paper Wrapping Paper

- 11.2.2. Plastic Wrapping Paper

- 11.2.3. Aluminum Foil Wrapping Paper

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nissha Metallizing

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Catty Corp

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Papermart

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bemis Company Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sonoco Products Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Amcor Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Silgan Holdings Inc.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Westrock co Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Aptar Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Graham Packaging Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Nissha Metallizing

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Candy Packaging Materials Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Candy Packaging Materials Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Candy Packaging Materials Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Candy Packaging Materials Volume (K), by Application 2025 & 2033

- Figure 5: North America Candy Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Candy Packaging Materials Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Candy Packaging Materials Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Candy Packaging Materials Volume (K), by Types 2025 & 2033

- Figure 9: North America Candy Packaging Materials Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Candy Packaging Materials Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Candy Packaging Materials Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Candy Packaging Materials Volume (K), by Country 2025 & 2033

- Figure 13: North America Candy Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Candy Packaging Materials Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Candy Packaging Materials Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Candy Packaging Materials Volume (K), by Application 2025 & 2033

- Figure 17: South America Candy Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Candy Packaging Materials Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Candy Packaging Materials Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Candy Packaging Materials Volume (K), by Types 2025 & 2033

- Figure 21: South America Candy Packaging Materials Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Candy Packaging Materials Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Candy Packaging Materials Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Candy Packaging Materials Volume (K), by Country 2025 & 2033

- Figure 25: South America Candy Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Candy Packaging Materials Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Candy Packaging Materials Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Candy Packaging Materials Volume (K), by Application 2025 & 2033

- Figure 29: Europe Candy Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Candy Packaging Materials Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Candy Packaging Materials Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Candy Packaging Materials Volume (K), by Types 2025 & 2033

- Figure 33: Europe Candy Packaging Materials Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Candy Packaging Materials Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Candy Packaging Materials Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Candy Packaging Materials Volume (K), by Country 2025 & 2033

- Figure 37: Europe Candy Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Candy Packaging Materials Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Candy Packaging Materials Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Candy Packaging Materials Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Candy Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Candy Packaging Materials Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Candy Packaging Materials Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Candy Packaging Materials Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Candy Packaging Materials Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Candy Packaging Materials Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Candy Packaging Materials Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Candy Packaging Materials Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Candy Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Candy Packaging Materials Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Candy Packaging Materials Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Candy Packaging Materials Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Candy Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Candy Packaging Materials Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Candy Packaging Materials Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Candy Packaging Materials Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Candy Packaging Materials Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Candy Packaging Materials Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Candy Packaging Materials Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Candy Packaging Materials Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Candy Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Candy Packaging Materials Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Candy Packaging Materials Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Candy Packaging Materials Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Candy Packaging Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Candy Packaging Materials Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Candy Packaging Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Candy Packaging Materials Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Candy Packaging Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Candy Packaging Materials Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Candy Packaging Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Candy Packaging Materials Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Candy Packaging Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Candy Packaging Materials Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Candy Packaging Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Candy Packaging Materials Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Candy Packaging Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Candy Packaging Materials Volume K Forecast, by Country 2020 & 2033

- Table 79: China Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Candy Packaging Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Candy Packaging Materials Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Candy Packaging Materials?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Candy Packaging Materials?

Key companies in the market include Nissha Metallizing, Catty Corp, Papermart, Bemis Company Inc., Sonoco Products Company, Amcor Limited, Silgan Holdings Inc., Westrock co Inc., Aptar Group, Graham Packaging Company.

3. What are the main segments of the Candy Packaging Materials?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Candy Packaging Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Candy Packaging Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Candy Packaging Materials?

To stay informed about further developments, trends, and reports in the Candy Packaging Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence