Key Insights

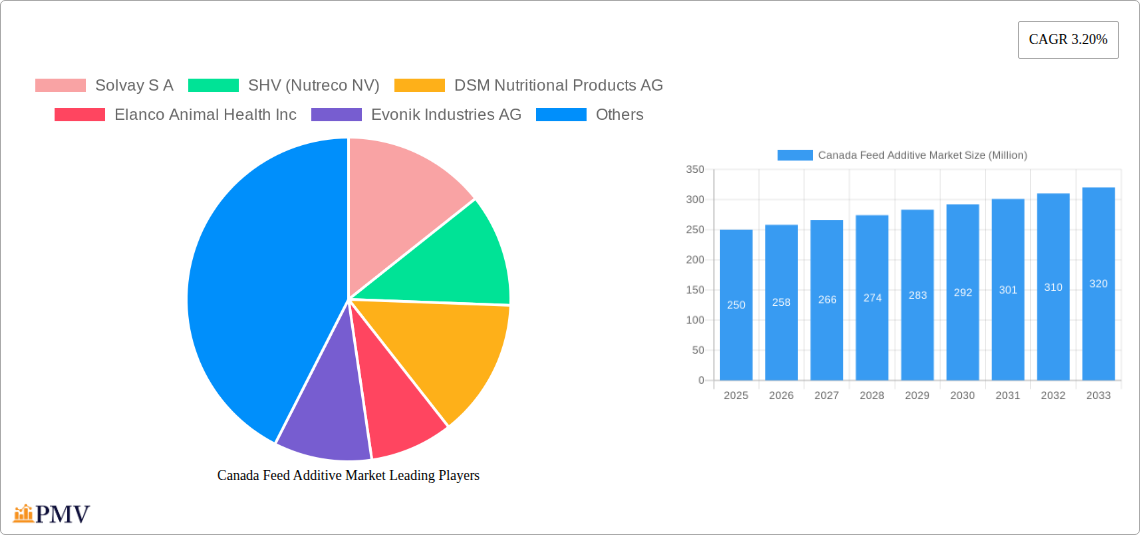

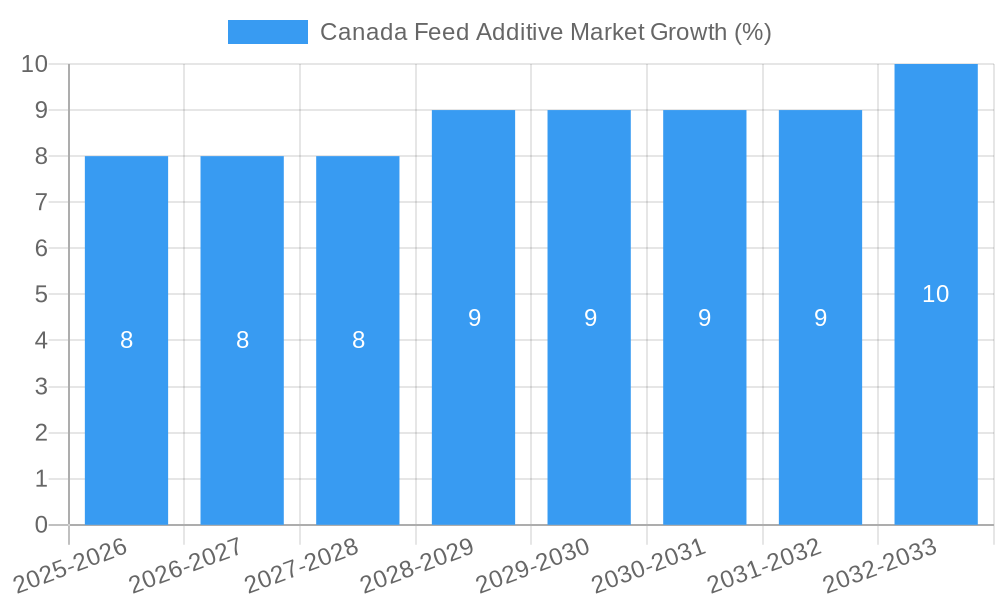

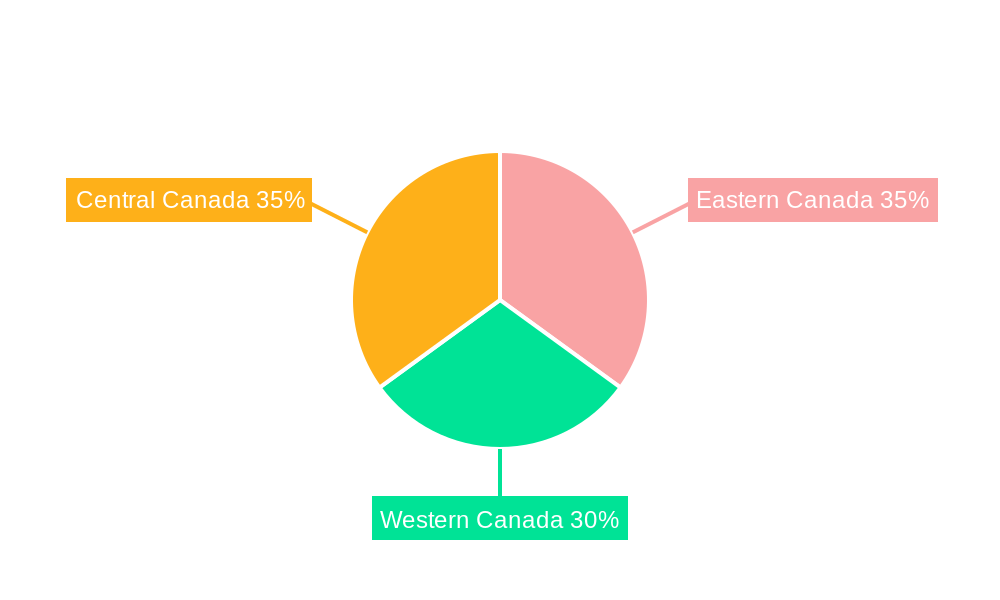

The Canadian feed additive market, valued at approximately $XXX million in 2025, is projected to experience steady growth, driven by factors such as increasing demand for animal protein, a focus on improving animal health and productivity, and the rising adoption of sustainable farming practices. The 3.20% CAGR (Compound Annual Growth Rate) from 2019-2033 suggests a robust market expansion over the forecast period (2025-2033). Key segments within the market include acidifiers, which are experiencing significant growth due to their ability to improve gut health and feed efficiency. Other significant segments are additives for other ruminants (cattle, sheep, goats), swine, and aquaculture. The increasing prevalence of animal diseases and the need for effective disease prevention and treatment are bolstering the demand for various feed additives. Competition among major players like Solvay, Nutreco, DSM, Elanco, Evonik, ADM, BASF, Alltech, Cargill, and IFF is intense, with companies focusing on innovation, product diversification, and strategic partnerships to gain market share. The regional distribution shows considerable market presence across Eastern, Western, and Central Canada, with potential for growth in all regions driven by the ongoing expansion of the livestock and aquaculture industries.

The Canadian market’s growth is influenced by government regulations regarding feed safety and animal welfare. Further expansion will depend on factors like the fluctuating prices of raw materials, evolving consumer preferences for sustainably produced animal products, and technological advancements in feed additive formulations. The aquaculture segment is anticipated to demonstrate strong growth fueled by the rising global demand for seafood and increasing investments in sustainable aquaculture practices. Swine feed additives are also projected to expand alongside the increasing domestic consumption of pork. Companies are focusing on developing specialized feed additives targeting specific animal species and addressing specific nutritional needs. This segmenting strategy, along with the continued emphasis on enhancing animal health and welfare, positions the Canadian feed additive market for sustained growth in the coming years.

Canada Feed Additive Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Canada Feed Additive Market, offering valuable insights for industry stakeholders, investors, and researchers. Covering the period from 2019 to 2033, with a focus on 2025, this report unveils market dynamics, growth drivers, and challenges, ultimately providing a strategic outlook for future market expansion. The report is meticulously structured to offer actionable intelligence, utilizing data-driven analysis and incorporating key market developments. The total market size is estimated at xx Million in 2025.

Canada Feed Additive Market Market Structure & Competitive Dynamics

The Canadian feed additive market exhibits a moderately concentrated structure, with several multinational corporations holding significant market share. Key players such as Solvay S.A., SHV (Nutreco NV), DSM Nutritional Products AG, Elanco Animal Health Inc., Evonik Industries AG, Archer Daniel Midland Co., BASF SE, Alltech Inc, Cargill Inc., and IFF (Danisco Animal Nutrition) compete intensely, driving innovation and impacting market pricing.

Market concentration is further influenced by the regulatory framework governing feed additives in Canada, which emphasizes product safety and efficacy. The presence of strong substitute products, particularly those based on natural ingredients and sustainable sourcing, exerts competitive pressure. End-user trends, including a growing demand for higher-quality animal protein and sustainable livestock farming practices, are shaping the market.

Mergers and acquisitions (M&A) have played a crucial role in shaping the market landscape. While specific deal values are not publicly available for all transactions, recent years have witnessed significant M&A activity. For instance, the partnership between Evonik and BASF (as detailed in the Key Developments section) showcases the strategic importance of collaborations. The combined market share of the top five players in 2025 is estimated to be around xx%. Innovation ecosystems are characterized by collaborations between feed additive manufacturers, research institutions, and agricultural technology companies, leading to the development of novel products and technologies.

Canada Feed Additive Market Industry Trends & Insights

The Canada Feed Additive Market is projected to experience substantial growth during the forecast period (2025-2033), driven by several key factors. The rising demand for animal protein, coupled with the increasing adoption of intensive livestock farming practices, fuels the need for efficient and effective feed additives. Technological advancements, such as the development of precision feed formulations and the application of data analytics in livestock management, further propel market expansion. Consumer preferences for sustainably produced animal products are also a significant driver. The market has witnessed an increasing emphasis on the use of natural and organic feed additives. The market is expected to grow at a CAGR of xx% during the forecast period. Market penetration of advanced feed additives is increasing, particularly in the swine and poultry segments. Competitive dynamics are characterized by continuous product innovation, strategic partnerships, and mergers and acquisitions, ensuring dynamic growth and market evolution.

Dominant Markets & Segments in Canada Feed Additive Market

The Canadian feed additive market is segmented by animal type (Swine, Other Ruminants, Other Animals, Aquaculture) and additive type (Acidifiers, etc.). The Swine segment is currently the dominant market segment, driven by the high demand for pork in Canada and intensive pig farming practices.

Key Drivers for Swine Segment Dominance:

- High Pork Consumption: Canada has a significant domestic demand for pork, leading to a large and growing swine industry.

- Intensive Farming Practices: The widespread adoption of intensive farming methods requires efficient feed additives to optimize animal health and productivity.

- Government Support: Government policies and initiatives supporting the swine industry provide favorable market conditions.

Other Ruminants: This segment is also experiencing growth due to the presence of a significant dairy and beef cattle industry. However, the swine segment currently holds a larger market share due to the higher concentration of intensive farming operations.

Other Animals and Aquaculture: These segments are experiencing moderate growth, driven by factors such as increasing poultry consumption and the expansion of the aquaculture industry in certain provinces.

Additive: Acidifiers: This is a leading additive type due to their importance in animal gut health and feed efficiency.

Canada Feed Additive Market Product Innovations

Recent years have witnessed significant product innovation in the Canadian feed additive market, primarily focusing on enhancing animal health, improving feed efficiency, and reducing environmental impact. The development of novel feed additives using advanced technologies such as precision fermentation and biotechnology is a prominent trend. These innovations aim to address growing consumer concerns regarding animal welfare and sustainability, enabling producers to meet evolving market demands. The market has also seen growth in the adoption of phytogenic feed additives, which offer natural alternatives to synthetic additives.

Report Segmentation & Scope

The report segments the Canadian feed additive market based on animal type (Swine, Other Ruminants, Other Animals, Aquaculture) and additive type (Acidifiers and others). Each segment's growth projection, market size (in Million), and competitive dynamics are analyzed in detail. For example, the Swine segment is projected to account for a significant portion of the overall market, driven by high demand and intensive farming practices. Similarly, the Acidifiers segment is expected to witness robust growth due to its efficacy in improving gut health and feed efficiency. Growth projections for each segment are provided for the forecast period (2025-2033).

Key Drivers of Canada Feed Additive Market Growth

Several factors are driving the growth of the Canada Feed Additive Market. These include the increasing demand for animal protein, leading to the expansion of the livestock industry. Advancements in feed additive technology, such as the development of novel, more efficient, and sustainable additives, are also significant drivers. Furthermore, supportive government policies and initiatives promoting sustainable livestock farming practices contribute to market expansion. Finally, the growing consumer awareness of animal health and welfare is driving adoption of high-quality feed additives.

Challenges in the Canada Feed Additive Market Sector

The Canada Feed Additive Market faces challenges such as stringent regulatory requirements for feed additive approval, leading to increased costs and time-to-market delays for new products. Supply chain disruptions, particularly during periods of global uncertainty, can impact the availability and cost of raw materials used in feed additive manufacturing. Finally, intense competition among established and emerging players in the market puts pressure on margins. These factors create a complex and dynamic market environment.

Leading Players in the Canada Feed Additive Market Market

- Solvay S A

- SHV (Nutreco NV)

- DSM Nutritional Products AG

- Elanco Animal Health Inc

- Evonik Industries AG

- Archer Daniel Midland Co

- BASF SE

- Alltech Inc

- Cargill Inc

- IFF(Danisco Animal Nutrition)

Key Developments in Canada Feed Additive Market Sector

- April 2022: Elanco and Royal DSM partnered for Bovaer, a methane-reducing feed additive for cattle, signifying a move towards sustainable livestock farming.

- June 2022: Delacon and Cargill collaborated to create a global plant-based phytogenic feed additives business, reflecting the growing demand for natural alternatives.

- October 2022: Evonik and BASF's partnership for OpteinicsTM, a digital solution for the animal protein and feed industries, highlights the integration of technology in improving efficiency and sustainability.

Strategic Canada Feed Additive Market Market Outlook

The Canada Feed Additive Market presents significant growth opportunities in the coming years. The increasing demand for animal protein, coupled with the focus on sustainable and efficient livestock production, will continue to drive market expansion. Strategic partnerships, mergers and acquisitions, and continuous product innovation will shape the future market landscape. Companies focusing on developing innovative, sustainable, and cost-effective feed additives will be well-positioned to capitalize on the market's growth potential. The market is poised for significant expansion driven by technological innovation and evolving consumer preferences.

Canada Feed Additive Market Segmentation

-

1. Additive

-

1.1. Acidifiers

-

1.1.1. By Sub Additive

- 1.1.1.1. Fumaric Acid

- 1.1.1.2. Lactic Acid

- 1.1.1.3. Propionic Acid

- 1.1.1.4. Other Acidifiers

-

1.1.1. By Sub Additive

-

1.2. Amino Acids

- 1.2.1. Lysine

- 1.2.2. Methionine

- 1.2.3. Threonine

- 1.2.4. Tryptophan

- 1.2.5. Other Amino Acids

-

1.3. Antibiotics

- 1.3.1. Bacitracin

- 1.3.2. Penicillins

- 1.3.3. Tetracyclines

- 1.3.4. Tylosin

- 1.3.5. Other Antibiotics

-

1.4. Antioxidants

- 1.4.1. Butylated Hydroxyanisole (BHA)

- 1.4.2. Butylated Hydroxytoluene (BHT)

- 1.4.3. Citric Acid

- 1.4.4. Ethoxyquin

- 1.4.5. Propyl Gallate

- 1.4.6. Tocopherols

- 1.4.7. Other Antioxidants

-

1.5. Binders

- 1.5.1. Natural Binders

- 1.5.2. Synthetic Binders

-

1.6. Enzymes

- 1.6.1. Carbohydrases

- 1.6.2. Phytases

- 1.6.3. Other Enzymes

- 1.7. Flavors & Sweeteners

-

1.8. Minerals

- 1.8.1. Macrominerals

- 1.8.2. Microminerals

-

1.9. Mycotoxin Detoxifiers

- 1.9.1. Biotransformers

-

1.10. Phytogenics

- 1.10.1. Essential Oil

- 1.10.2. Herbs & Spices

- 1.10.3. Other Phytogenics

-

1.11. Pigments

- 1.11.1. Carotenoids

- 1.11.2. Curcumin & Spirulina

-

1.12. Prebiotics

- 1.12.1. Fructo Oligosaccharides

- 1.12.2. Galacto Oligosaccharides

- 1.12.3. Inulin

- 1.12.4. Lactulose

- 1.12.5. Mannan Oligosaccharides

- 1.12.6. Xylo Oligosaccharides

- 1.12.7. Other Prebiotics

-

1.13. Probiotics

- 1.13.1. Bifidobacteria

- 1.13.2. Enterococcus

- 1.13.3. Lactobacilli

- 1.13.4. Pediococcus

- 1.13.5. Streptococcus

- 1.13.6. Other Probiotics

-

1.14. Vitamins

- 1.14.1. Vitamin A

- 1.14.2. Vitamin B

- 1.14.3. Vitamin C

- 1.14.4. Vitamin E

- 1.14.5. Other Vitamins

-

1.15. Yeast

- 1.15.1. Live Yeast

- 1.15.2. Selenium Yeast

- 1.15.3. Spent Yeast

- 1.15.4. Torula Dried Yeast

- 1.15.5. Whey Yeast

- 1.15.6. Yeast Derivatives

-

1.1. Acidifiers

-

2. Animal

-

2.1. Aquaculture

-

2.1.1. By Sub Animal

- 2.1.1.1. Fish

- 2.1.1.2. Shrimp

- 2.1.1.3. Other Aquaculture Species

-

2.1.1. By Sub Animal

-

2.2. Poultry

- 2.2.1. Broiler

- 2.2.2. Layer

- 2.2.3. Other Poultry Birds

-

2.3. Ruminants

- 2.3.1. Beef Cattle

- 2.3.2. Dairy Cattle

- 2.3.3. Other Ruminants

- 2.4. Swine

- 2.5. Other Animals

-

2.1. Aquaculture

Canada Feed Additive Market Segmentation By Geography

- 1. Canada

Canada Feed Additive Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Fish Consumption; Rise in Export-oriented Aquaculture

- 3.3. Market Restrains

- 3.3.1. Fluctuating Global Prices of Raw Materials; Increasing Disease Epidemics in Major Markets

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Feed Additive Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Additive

- 5.1.1. Acidifiers

- 5.1.1.1. By Sub Additive

- 5.1.1.1.1. Fumaric Acid

- 5.1.1.1.2. Lactic Acid

- 5.1.1.1.3. Propionic Acid

- 5.1.1.1.4. Other Acidifiers

- 5.1.1.1. By Sub Additive

- 5.1.2. Amino Acids

- 5.1.2.1. Lysine

- 5.1.2.2. Methionine

- 5.1.2.3. Threonine

- 5.1.2.4. Tryptophan

- 5.1.2.5. Other Amino Acids

- 5.1.3. Antibiotics

- 5.1.3.1. Bacitracin

- 5.1.3.2. Penicillins

- 5.1.3.3. Tetracyclines

- 5.1.3.4. Tylosin

- 5.1.3.5. Other Antibiotics

- 5.1.4. Antioxidants

- 5.1.4.1. Butylated Hydroxyanisole (BHA)

- 5.1.4.2. Butylated Hydroxytoluene (BHT)

- 5.1.4.3. Citric Acid

- 5.1.4.4. Ethoxyquin

- 5.1.4.5. Propyl Gallate

- 5.1.4.6. Tocopherols

- 5.1.4.7. Other Antioxidants

- 5.1.5. Binders

- 5.1.5.1. Natural Binders

- 5.1.5.2. Synthetic Binders

- 5.1.6. Enzymes

- 5.1.6.1. Carbohydrases

- 5.1.6.2. Phytases

- 5.1.6.3. Other Enzymes

- 5.1.7. Flavors & Sweeteners

- 5.1.8. Minerals

- 5.1.8.1. Macrominerals

- 5.1.8.2. Microminerals

- 5.1.9. Mycotoxin Detoxifiers

- 5.1.9.1. Biotransformers

- 5.1.10. Phytogenics

- 5.1.10.1. Essential Oil

- 5.1.10.2. Herbs & Spices

- 5.1.10.3. Other Phytogenics

- 5.1.11. Pigments

- 5.1.11.1. Carotenoids

- 5.1.11.2. Curcumin & Spirulina

- 5.1.12. Prebiotics

- 5.1.12.1. Fructo Oligosaccharides

- 5.1.12.2. Galacto Oligosaccharides

- 5.1.12.3. Inulin

- 5.1.12.4. Lactulose

- 5.1.12.5. Mannan Oligosaccharides

- 5.1.12.6. Xylo Oligosaccharides

- 5.1.12.7. Other Prebiotics

- 5.1.13. Probiotics

- 5.1.13.1. Bifidobacteria

- 5.1.13.2. Enterococcus

- 5.1.13.3. Lactobacilli

- 5.1.13.4. Pediococcus

- 5.1.13.5. Streptococcus

- 5.1.13.6. Other Probiotics

- 5.1.14. Vitamins

- 5.1.14.1. Vitamin A

- 5.1.14.2. Vitamin B

- 5.1.14.3. Vitamin C

- 5.1.14.4. Vitamin E

- 5.1.14.5. Other Vitamins

- 5.1.15. Yeast

- 5.1.15.1. Live Yeast

- 5.1.15.2. Selenium Yeast

- 5.1.15.3. Spent Yeast

- 5.1.15.4. Torula Dried Yeast

- 5.1.15.5. Whey Yeast

- 5.1.15.6. Yeast Derivatives

- 5.1.1. Acidifiers

- 5.2. Market Analysis, Insights and Forecast - by Animal

- 5.2.1. Aquaculture

- 5.2.1.1. By Sub Animal

- 5.2.1.1.1. Fish

- 5.2.1.1.2. Shrimp

- 5.2.1.1.3. Other Aquaculture Species

- 5.2.1.1. By Sub Animal

- 5.2.2. Poultry

- 5.2.2.1. Broiler

- 5.2.2.2. Layer

- 5.2.2.3. Other Poultry Birds

- 5.2.3. Ruminants

- 5.2.3.1. Beef Cattle

- 5.2.3.2. Dairy Cattle

- 5.2.3.3. Other Ruminants

- 5.2.4. Swine

- 5.2.5. Other Animals

- 5.2.1. Aquaculture

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Additive

- 6. Eastern Canada Canada Feed Additive Market Analysis, Insights and Forecast, 2019-2031

- 7. Western Canada Canada Feed Additive Market Analysis, Insights and Forecast, 2019-2031

- 8. Central Canada Canada Feed Additive Market Analysis, Insights and Forecast, 2019-2031

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Solvay S A

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 SHV (Nutreco NV)

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 DSM Nutritional Products AG

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Elanco Animal Health Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Evonik Industries AG

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Archer Daniel Midland Co

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 BASF SE

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Alltech Inc

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Cargill Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 IFF(Danisco Animal Nutrition)

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.1 Solvay S A

List of Figures

- Figure 1: Canada Feed Additive Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Canada Feed Additive Market Share (%) by Company 2024

List of Tables

- Table 1: Canada Feed Additive Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Canada Feed Additive Market Revenue Million Forecast, by Additive 2019 & 2032

- Table 3: Canada Feed Additive Market Revenue Million Forecast, by Animal 2019 & 2032

- Table 4: Canada Feed Additive Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Canada Feed Additive Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Eastern Canada Canada Feed Additive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Western Canada Canada Feed Additive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Central Canada Canada Feed Additive Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada Feed Additive Market Revenue Million Forecast, by Additive 2019 & 2032

- Table 10: Canada Feed Additive Market Revenue Million Forecast, by Animal 2019 & 2032

- Table 11: Canada Feed Additive Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Feed Additive Market?

The projected CAGR is approximately 3.20%.

2. Which companies are prominent players in the Canada Feed Additive Market?

Key companies in the market include Solvay S A, SHV (Nutreco NV), DSM Nutritional Products AG, Elanco Animal Health Inc, Evonik Industries AG, Archer Daniel Midland Co, BASF SE, Alltech Inc, Cargill Inc, IFF(Danisco Animal Nutrition).

3. What are the main segments of the Canada Feed Additive Market?

The market segments include Additive, Animal.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Fish Consumption; Rise in Export-oriented Aquaculture.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Fluctuating Global Prices of Raw Materials; Increasing Disease Epidemics in Major Markets.

8. Can you provide examples of recent developments in the market?

October 2022: The partnership between Evonik and BASF allowed Evonik certain non-exclusive licensing rights to OpteinicsTM, a digital solution to improve comprehension and reduce the environmental impact of the animal protein and feed industries.June 2022: Delacon and Cargill collaborated to establish a global plant-based phytogenic feed additives business for enhanced animal nutrition. The partnership has helped in extensive feed additives expertise as well as an increase in the global presence.April 2022: A strategic partnership has been made between Elanco and Royal DSM for Bovaer, an innovative, methane-reducing feed additive for cattle.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Feed Additive Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Feed Additive Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Feed Additive Market?

To stay informed about further developments, trends, and reports in the Canada Feed Additive Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence