Key Insights

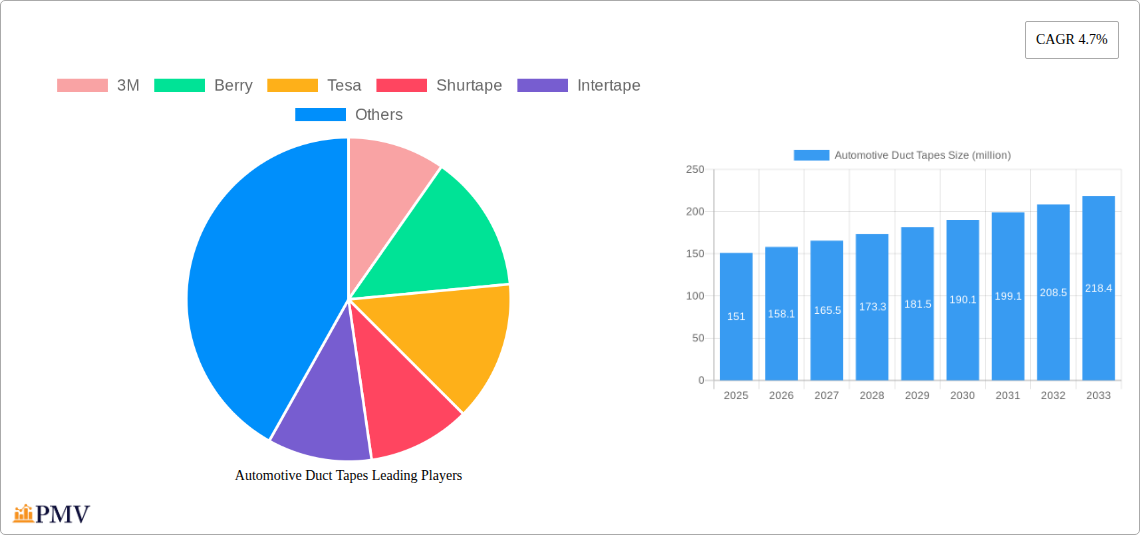

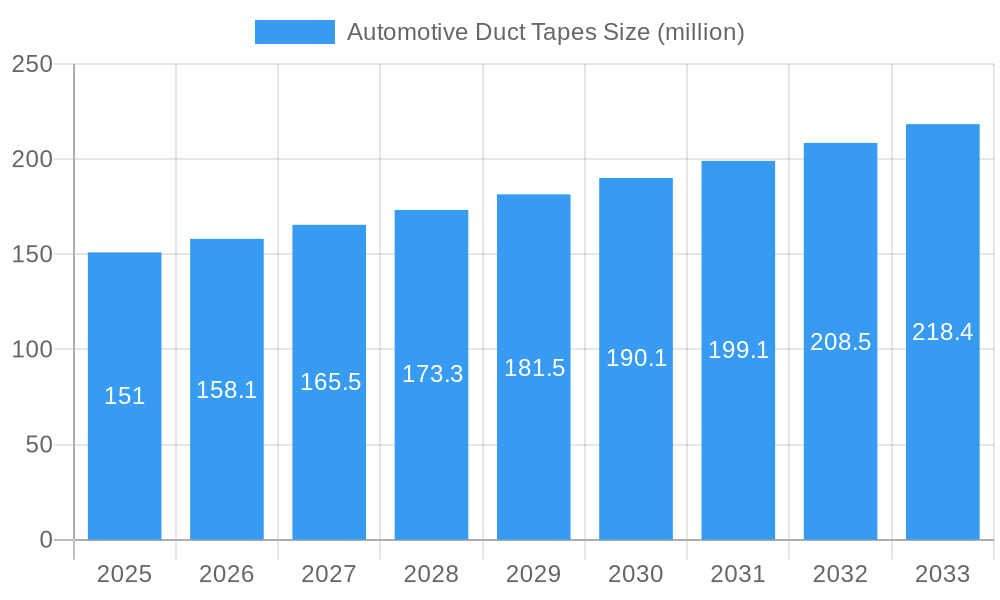

The global Automotive Duct Tape market is poised for robust expansion, projected to reach an estimated USD 151 million by 2025. This growth trajectory is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 4.7% anticipated over the forecast period from 2025 to 2033. The increasing complexity and demand for specialized solutions in both passenger and commercial vehicle manufacturing are primary catalysts for this sustained upward trend. Automotive duct tapes are instrumental in a myriad of applications, from temporary repairs and sealing to specialized bonding and insulation within vehicle assemblies. Their versatility and cost-effectiveness make them indispensable for manufacturers seeking efficient and reliable solutions. The evolving automotive landscape, with its emphasis on lightweighting, noise reduction, and improved durability, further fuels the demand for advanced adhesive tapes that can meet these stringent requirements.

Automotive Duct Tapes Market Size (In Million)

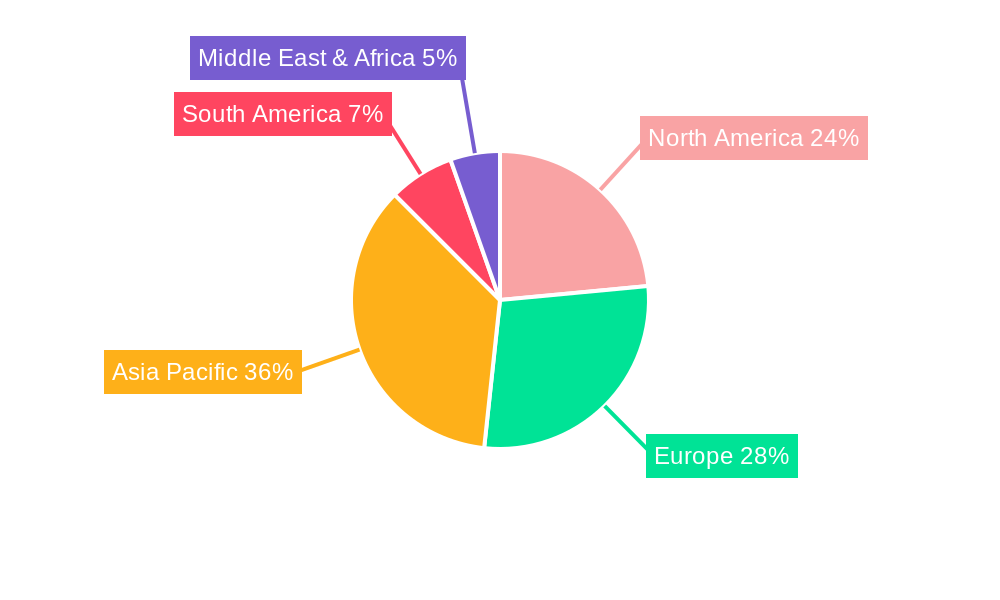

The market's dynamism is further shaped by an interplay of driving forces, emerging trends, and strategic initiatives by key industry players such as 3M, Berry, and Tesa. Innovations in material science, particularly in the development of high-performance rubber, acrylic, and silicone-based duct tapes, are expanding the application spectrum and enhancing product efficacy. For instance, enhanced temperature resistance, superior adhesion to diverse substrates, and improved flexibility are key attributes driving adoption. While the market exhibits strong growth, potential restraints such as fluctuating raw material costs and the emergence of alternative joining technologies necessitate continuous innovation and competitive pricing strategies from manufacturers. Nonetheless, the expanding automotive production globally, coupled with the increasing penetration of electric vehicles (EVs) that often require specialized sealing and insulation solutions, presents significant opportunities for market players to capitalize on. The Asia Pacific region, led by China, is expected to remain a dominant force, driven by its expansive manufacturing base and growing automotive sector.

Automotive Duct Tapes Company Market Share

Automotive Duct Tapes Market: Comprehensive Global Analysis and Forecast (2019-2033)

This in-depth market research report provides a detailed examination of the global Automotive Duct Tapes market, offering strategic insights and actionable intelligence for stakeholders. Spanning a study period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, this report delves into market structure, competitive dynamics, industry trends, dominant segments, product innovations, key growth drivers, challenges, leading players, and crucial developments. It is meticulously crafted for industry professionals seeking to understand current market landscapes and future opportunities in the automotive adhesive solutions sector.

Automotive Duct Tapes Market Structure & Competitive Dynamics

The global Automotive Duct Tapes market exhibits a moderately concentrated structure, with key players like 3M, Berry Global, and Tesa SE holding significant market shares. Innovation ecosystems are thriving, driven by continuous research and development in advanced adhesive formulations and material science, aimed at enhancing durability, temperature resistance, and environmental sustainability of duct tapes for automotive applications. Regulatory frameworks, primarily concerning material safety, emissions, and recyclability, play a crucial role in shaping product development and market entry strategies. The threat of product substitutes, such as liquid sealants and specialized foams, remains a consideration, although duct tapes offer distinct advantages in terms of ease of application and cost-effectiveness for certain automotive repairs and assembly processes. End-user trends are increasingly favoring tapes that contribute to vehicle lightweighting and improved acoustic insulation. Mergers and acquisitions (M&A) activities, with estimated deal values in the tens of millions, are observed as companies seek to expand their product portfolios, geographic reach, and technological capabilities. For instance, a recent M&A deal in the automotive adhesives sector was valued at approximately 15 million. The overall market concentration is estimated to be around 60% among the top five players.

Automotive Duct Tapes Industry Trends & Insights

The Automotive Duct Tapes industry is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.8% over the forecast period (2025-2033). This expansion is primarily fueled by the burgeoning automotive production globally, particularly in emerging economies. Technological disruptions are central to this growth, with manufacturers investing heavily in the development of advanced duct tapes that offer superior adhesion, enhanced weather resistance, and improved thermal management capabilities. These innovations are critical for meeting the evolving demands of the automotive sector, including the increasing complexity of vehicle designs and the integration of new materials. Consumer preferences are shifting towards tapes that are not only highly functional but also environmentally friendly, with a growing demand for solvent-free and recyclable adhesive solutions. The competitive landscape is characterized by intense price competition and a continuous drive for product differentiation through superior performance characteristics. Market penetration is steadily increasing across both passenger car and commercial vehicle segments as manufacturers recognize the versatility and cost-effectiveness of duct tapes in various assembly, repair, and interior/exterior finishing applications. The global market penetration rate for specialized automotive duct tapes is estimated to be around 45% and is expected to reach 65% by 2033. Emerging trends include the development of smart tapes with integrated sensors for monitoring and diagnostic purposes, although these are still in their nascent stages of adoption.

Dominant Markets & Segments in Automotive Duct Tapes

The Passenger Car segment is currently the dominant market within the Automotive Duct Tapes industry, accounting for an estimated 70% of the total market revenue. This dominance is driven by the sheer volume of passenger vehicle production worldwide and the widespread application of duct tapes in interior trim, wire harnessing, temporary repairs, and noise reduction solutions. Key drivers for this segment's growth include rising disposable incomes in developing nations leading to increased car ownership, government initiatives promoting automotive manufacturing, and the growing demand for personalized vehicle interiors and accessories.

- Application: Passenger Car: This segment's dominance is further bolstered by the extensive use of duct tapes in sound dampening applications within vehicle cabins, contributing to a more comfortable driving experience. The need for reliable and durable tapes for securing interior components and protecting surfaces during assembly also significantly contributes to its market share.

- Types: Rubber Duct Tape: Within the product types, Rubber Duct Tapes represent a significant portion of the market due to their excellent adhesion, flexibility, and water-resistant properties, making them ideal for sealing and temporary repairs in automotive environments. The market share for Rubber Duct Tapes is estimated to be around 40%.

- Types: Acrylic Duct Tape: Acrylic Duct Tapes are gaining traction due to their superior UV resistance and long-term durability, crucial for exterior applications and under-the-hood uses where exposure to harsh elements is common. The market share of Acrylic Duct Tapes is approximately 35%.

- Types: Silicone Duct Tape: Silicone Duct Tapes are emerging as a niche but high-value segment, prized for their extreme temperature resistance and flexibility, making them suitable for specialized automotive applications like exhaust system repairs and high-temperature engine bay applications. Their market share is currently around 15%.

- Types: Others: This category includes specialized tapes like fabric-backed or foil-backed duct tapes, catering to specific performance requirements and contributing approximately 10% to the market.

The Asia-Pacific region, particularly China, India, and Southeast Asian countries, emerges as the leading geographical market, driven by its position as a global automotive manufacturing hub and a rapidly expanding consumer base. Economic policies supporting manufacturing and infrastructure development, coupled with a large, cost-sensitive market, further solidify its dominance.

Automotive Duct Tapes Product Innovations

Product innovations in the Automotive Duct Tapes market are primarily focused on enhancing performance and sustainability. Manufacturers are developing high-strength, temperature-resistant duct tapes capable of withstanding extreme under-the-hood conditions and offering superior adhesion to diverse automotive substrates, including plastics, metals, and composites. Innovations also include the development of low-VOC (Volatile Organic Compound) and solvent-free adhesive formulations to meet stringent environmental regulations and consumer demand for greener products. Furthermore, advancements in tape backing materials are leading to improved tear resistance, conformability, and reduced weight, contributing to vehicle lightweighting initiatives. These innovations aim to provide automotive manufacturers with reliable, efficient, and eco-conscious solutions for assembly, repair, and finishing processes.

Report Segmentation & Scope

This report segments the global Automotive Duct Tapes market across key dimensions to provide granular insights.

- Application: The market is analyzed based on its application in Passenger Cars and Commercial Vehicles. The Passenger Car segment is projected to hold a significant market share due to higher production volumes and diverse application needs, with an estimated market size of 1,200 million in 2025. The Commercial Vehicle segment, while smaller, is expected to exhibit steady growth driven by fleet maintenance and repair needs, with a projected market size of 500 million in 2025.

- Types: The report further categorizes the market by product type: Rubber Duct Tape, Acrylic Duct Tape, Silicone Duct Tape, and Others. Rubber Duct Tapes are anticipated to lead in terms of market share due to their versatility and cost-effectiveness, estimated at 480 million in 2025. Acrylic Duct Tapes are expected to grow due to their durability, with a projected market size of 420 million in 2025. Silicone Duct Tapes, though a niche, are forecast for significant percentage growth due to their specialized high-performance applications, with a market size of 180 million in 2025. The "Others" category, encompassing specialized tapes, is estimated at 120 million in 2025.

Key Drivers of Automotive Duct Tapes Growth

The Automotive Duct Tapes market is propelled by several key drivers. The sustained growth in global automotive production, particularly in emerging economies, directly translates to increased demand for automotive tapes. Technological advancements in adhesive formulations, leading to tapes with improved thermal resistance, enhanced durability, and better adhesion to new composite materials, are crucial for meeting evolving vehicle design requirements. Furthermore, the increasing emphasis on vehicle lightweighting initiatives to improve fuel efficiency and reduce emissions is creating opportunities for specialized, high-strength, and lightweight duct tapes. Regulatory mandates promoting the use of eco-friendly and low-VOC adhesives also contribute to market expansion, pushing innovation towards sustainable solutions. The growing aftermarket for vehicle repairs and customizations also fuels demand for reliable and easy-to-use duct tape solutions, valued at approximately 800 million in aftermarket sales.

Challenges in the Automotive Duct Tapes Sector

Despite robust growth prospects, the Automotive Duct Tapes sector faces several challenges. Intense price competition among manufacturers, especially in emerging markets, can compress profit margins. The increasing complexity of vehicle interiors and the integration of sophisticated electronic components necessitate highly specialized tapes, posing a challenge for manufacturers to keep pace with rapid technological evolution. The stringent and evolving regulatory landscape regarding material safety, emissions, and end-of-life vehicle recycling can also create compliance hurdles and necessitate significant R&D investments. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production costs and lead times, creating uncertainty for both manufacturers and end-users. Competitive pressures from alternative sealing and bonding solutions, such as advanced adhesives and mechanical fasteners, also necessitate continuous innovation and value proposition reinforcement. The global supply chain for key raw materials is valued at approximately 600 million and is subject to fluctuations.

Leading Players in the Automotive Duct Tapes Market

- 3M

- Berry Global

- Tesa SE

- Shurtape Technologies

- Intertape Polymer Group (IPG)

- PPM Industries

- Scapa Group

- Bolex (Shenzhen) Adhesive Co., Ltd.

- Vibac Group

- Coroplast

- Pro Tapes & Specialties

- Yong Yi Adhesive (Zhongshan) Co., Ltd.

- Egret Group

- Ningbo Anda Anticorrosive Material Co., Ltd.

- Render Tape

Key Developments in Automotive Duct Tapes Sector

- 2023 September: 3M launched a new line of high-temperature resistant duct tapes designed for under-the-hood automotive applications, improving engine bay durability.

- 2023 July: Berry Global announced an expansion of its automotive adhesive production capacity, anticipating increased demand for specialized tapes.

- 2022 December: Tesa SE introduced a new eco-friendly automotive duct tape with a significant portion of its formulation derived from renewable resources, aligning with sustainability trends.

- 2022 April: Shurtape Technologies acquired a smaller competitor, expanding its product portfolio and market reach in the automotive segment, with a deal value estimated at 10 million.

- 2021 November: Intertape Polymer Group (IPG) invested in advanced R&D for lightweighting tapes, focusing on composite material adhesion for the automotive industry.

Strategic Automotive Duct Tapes Market Outlook

The strategic outlook for the Automotive Duct Tapes market remains highly positive, driven by consistent demand from the global automotive industry and ongoing technological advancements. Key growth accelerators include the increasing adoption of electric vehicles (EVs), which present unique opportunities for specialized thermal management and battery pack sealing tapes. The growing emphasis on vehicle customization and repair in the aftermarket segment also provides a stable revenue stream. Furthermore, the continuous pursuit of lightweighting and improved acoustic performance in vehicles will drive demand for innovative and high-performance duct tape solutions. Strategic opportunities lie in developing sustainable, bio-based, and recyclable adhesive products to cater to evolving environmental regulations and consumer preferences, alongside expanding geographic presence in rapidly growing automotive manufacturing hubs. The overall market potential is estimated to reach approximately 2,500 million by 2033.

Automotive Duct Tapes Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Rubber Duct Tape

- 2.2. Acrylic Duct Tape

- 2.3. Silicone Duct Tape

- 2.4. Others

Automotive Duct Tapes Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Duct Tapes Regional Market Share

Geographic Coverage of Automotive Duct Tapes

Automotive Duct Tapes REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Rubber Duct Tape

- 5.2.2. Acrylic Duct Tape

- 5.2.3. Silicone Duct Tape

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Rubber Duct Tape

- 6.2.2. Acrylic Duct Tape

- 6.2.3. Silicone Duct Tape

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Rubber Duct Tape

- 7.2.2. Acrylic Duct Tape

- 7.2.3. Silicone Duct Tape

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Rubber Duct Tape

- 8.2.2. Acrylic Duct Tape

- 8.2.3. Silicone Duct Tape

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Rubber Duct Tape

- 9.2.2. Acrylic Duct Tape

- 9.2.3. Silicone Duct Tape

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Duct Tapes Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Rubber Duct Tape

- 10.2.2. Acrylic Duct Tape

- 10.2.3. Silicone Duct Tape

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 3M

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Berry

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Tesa

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Shurtape

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Intertape

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 PPM

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Scapa

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bolex (Shenzhen) Adhesive

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Vibac

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Coroplast

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Pro Tapes & Specialties

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Yong Yi Adhesive (Zhongshan)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Egret Group

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ningbo Anda Anticorrosive Material

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Render Tape

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 3M

List of Figures

- Figure 1: Global Automotive Duct Tapes Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Duct Tapes Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Duct Tapes Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Duct Tapes Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Duct Tapes Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Duct Tapes Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Duct Tapes Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Duct Tapes Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Duct Tapes Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Duct Tapes Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Duct Tapes Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Duct Tapes Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Duct Tapes Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Duct Tapes Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Duct Tapes Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Duct Tapes Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Duct Tapes Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Duct Tapes Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Duct Tapes Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Duct Tapes Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Duct Tapes Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Duct Tapes Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Duct Tapes Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Duct Tapes Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Duct Tapes Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Duct Tapes Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Duct Tapes Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Duct Tapes Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Duct Tapes Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Duct Tapes Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Duct Tapes Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Duct Tapes Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Duct Tapes Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Duct Tapes Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Duct Tapes Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Duct Tapes Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Duct Tapes Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Duct Tapes Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Duct Tapes Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Duct Tapes Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Duct Tapes?

The projected CAGR is approximately 4.7%.

2. Which companies are prominent players in the Automotive Duct Tapes?

Key companies in the market include 3M, Berry, Tesa, Shurtape, Intertape, PPM, Scapa, Bolex (Shenzhen) Adhesive, Vibac, Coroplast, Pro Tapes & Specialties, Yong Yi Adhesive (Zhongshan), Egret Group, Ningbo Anda Anticorrosive Material, Render Tape.

3. What are the main segments of the Automotive Duct Tapes?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 151 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Duct Tapes," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Duct Tapes report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Duct Tapes?

To stay informed about further developments, trends, and reports in the Automotive Duct Tapes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence