Key Insights

The global Automotive Digital Retailing Solutions market is projected for substantial growth, expected to reach $714.43 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 7.4%. This expansion is propelled by the increasing consumer demand for intuitive, online automotive purchasing journeys. Key drivers include the widespread adoption of digital technologies by dealerships to elevate customer engagement, optimize sales workflows, and boost operational effectiveness. The growing consumer preference for online research and purchasing, influenced by evolving lifestyles and the convenience of digital platforms, further stimulates market growth. Moreover, the integration of features such as virtual showrooms, online financing, and digital trade-in valuations is becoming a standard offering, attracting a broad spectrum of businesses, from small and medium-sized enterprises (SMEs) to large automotive corporations.

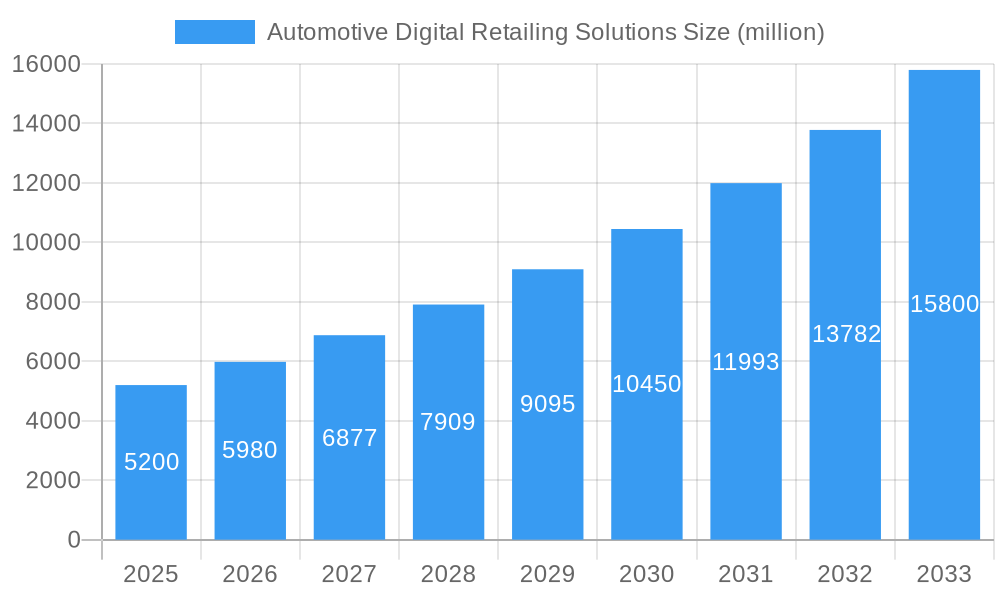

Automotive Digital Retailing Solutions Market Size (In Billion)

The market is anticipated to maintain its robust upward trajectory through 2033, fueled by continuous innovation and evolving consumer expectations. While the shift to digital retailing offers significant opportunities, initial technology implementation costs and the requirement for comprehensive staff training pose potential challenges. Nevertheless, the prospective gains in sales volume, enhanced customer satisfaction, and strengthened brand loyalty are expected to surpass these hurdles. Cloud-based solutions are poised for market dominance owing to their inherent scalability, flexibility, and cost-effectiveness compared to on-premises systems, adeptly serving the varied requirements of both SMEs and large enterprises aiming to modernize their sales operations.

Automotive Digital Retailing Solutions Company Market Share

Automotive Digital Retailing Solutions Market Structure & Competitive Dynamics

The Automotive Digital Retailing Solutions market is characterized by a dynamic and evolving competitive landscape, with key players striving for market consolidation and innovation. Market concentration varies across different segments, with some areas dominated by a few large enterprises and others fostering a more fragmented ecosystem of SMEs. The innovation ecosystem is fueled by constant technological advancements, particularly in cloud-based solutions, AI-powered personalization, and seamless online-to-offline customer journeys. Regulatory frameworks are gradually adapting to digital transactions, though regional disparities exist, influencing market entry and operational strategies. Product substitutes are emerging, ranging from traditional dealership models with limited digital integration to more advanced, fully online purchasing platforms. End-user trends are overwhelmingly leaning towards digital convenience, demanding transparent pricing, virtual test drives, and simplified financing options. Mergers and acquisitions (M&A) are a significant driver of market structure, with deal values often exceeding several hundred million dollars as larger companies acquire innovative startups to enhance their digital capabilities. For instance, Cox Automotive's strategic acquisitions have consistently aimed to bolster their digital offerings, while smaller players like AutoFi and Gubagoo are actively expanding their market share through strategic partnerships and feature enhancements. The market share of leading providers is continually shifting as new entrants and established players adapt their strategies to meet evolving consumer expectations for a frictionless automotive purchase experience.

Automotive Digital Retailing Solutions Industry Trends & Insights

The Automotive Digital Retailing Solutions industry is experiencing robust growth, driven by a confluence of technological advancements, shifting consumer preferences, and strategic investments. The market penetration of digital retailing solutions is projected to reach over 70% within the forecast period. A significant market growth driver is the increasing consumer demand for a convenient, transparent, and personalized car buying experience, mirroring trends seen in other e-commerce sectors. This necessitates the adoption of end-to-end digital platforms that facilitate everything from initial research and vehicle configuration to financing, trade-in valuations, and even delivery. Technological disruptions, including the widespread adoption of Artificial Intelligence (AI) for personalized recommendations and chatbots for instant customer support, are revolutionizing customer engagement. Blockchain technology is also emerging as a potential disruptor, offering enhanced security and transparency in vehicle history and ownership transfers. The rise of electric vehicles (EVs) and connected car technologies further fuels the need for integrated digital ecosystems that can manage sales, service, and ownership seamlessly. Competitive dynamics are intensifying, with established automotive giants investing heavily in their digital infrastructure, while agile startups are carving out niches with specialized solutions. Companies like Upstart Auto Retail and Digital Motors Corporation are at the forefront, offering comprehensive suites of digital tools designed to streamline the entire vehicle acquisition process. The projected Compound Annual Growth Rate (CAGR) for the Automotive Digital Retailing Solutions market is estimated to be approximately 15% over the forecast period (2025–2033), with the global market size expected to surpass several hundred million dollars by the end of the study period. This growth is supported by significant investments in R&D and the continuous development of user-friendly interfaces that cater to a digitally native customer base. The evolution from traditional dealership models to hybrid and fully digital retail experiences is a defining trend, promising to reshape the automotive sales landscape significantly.

Dominant Markets & Segments in Automotive Digital Retailing Solutions

The Automotive Digital Retailing Solutions market exhibits distinct regional dominance and segmentation patterns, largely influenced by economic policies, infrastructure development, and consumer digital adoption rates. North America, particularly the United States, currently stands as the dominant market, driven by high internet penetration, a mature automotive industry, and a consumer base that readily embraces technological innovation in purchasing. The region's robust economic policies supporting technological advancements and significant investments in digital infrastructure have created a fertile ground for digital retailing solutions.

Leading Region: North America, with an estimated market share of over 40% in 2025.

- Key Drivers: High consumer acceptance of online transactions, strong regulatory support for digital commerce, and the presence of major automotive manufacturers and technology providers investing heavily in digital transformation.

- Infrastructure: Advanced internet connectivity and a well-established logistics network facilitate seamless online car purchases and deliveries.

Dominant Application Segment: Large Enterprises: Large enterprises, including major automotive manufacturers and large dealership groups, currently hold a significant market share. Their capacity for substantial investment in sophisticated digital platforms, integration with existing systems, and broader reach makes them early adopters and key drivers of market adoption. The comprehensive nature of their operations necessitates robust and scalable solutions that can manage vast inventories and complex sales processes.

- Key Drivers: Need for brand consistency across dealerships, ability to invest in custom solutions, and the requirement for integrated CRM and inventory management systems.

- Market Size: Estimated to be several hundred million dollars in 2025, with strong growth potential as they further digitize their operations.

Dominant Type Segment: Cloud Based: Cloud-based solutions are the preferred type across all segments due to their scalability, flexibility, accessibility, and cost-effectiveness. This model allows businesses of all sizes to leverage advanced digital retailing capabilities without significant upfront infrastructure investments. The ability to access and update software remotely ensures continuous improvement and adaptation to evolving market demands.

- Key Drivers: Lower total cost of ownership, rapid deployment, seamless integration capabilities, and automatic updates providing access to the latest features and security patches.

- Market Size: Expected to represent over 80% of the market in 2025 and continue its dominance throughout the forecast period.

While SMEs are a growing segment, their adoption is often driven by more agile and cost-effective solutions, with many leveraging cloud-based platforms tailored to their specific needs. On-premises solutions, while still present, are gradually declining in favor of the flexibility and scalability offered by cloud alternatives. The competitive dynamics within these dominant segments involve a race to offer the most comprehensive, user-friendly, and integrated digital retail experience, encompassing virtual showrooms, online financing, and contactless delivery options.

Automotive Digital Retailing Solutions Product Innovations

Automotive Digital Retailing Solutions are witnessing rapid product innovation focused on enhancing the customer journey and dealership efficiency. Key developments include AI-powered personalized vehicle recommendations, virtual reality (VR) showrooms offering immersive product experiences, and integrated financing platforms that provide instant loan approvals. Solutions like those offered by AutoFi and CarNow are leading in streamlining the online purchase process, while Gubagoo is innovating with conversational AI for lead generation and customer support. These innovations aim to replicate and improve upon the traditional dealership experience digitally, offering competitive advantages through increased transparency, reduced transaction times, and improved customer satisfaction. Market fit is achieved by addressing the core consumer desire for convenience and control in vehicle acquisition.

Report Segmentation & Scope

This report segments the Automotive Digital Retailing Solutions market by application and type. The application segmentation includes Small and Medium-sized Enterprises (SMEs) and Large Enterprises. SMEs are characterized by their need for agile, cost-effective solutions, while Large Enterprises require scalable, fully integrated platforms. The market size for SMEs is projected to grow at a CAGR of approximately 18% from 2025 to 2033, reaching several million dollars. Large Enterprises, representing a larger market share initially, are expected to grow at a CAGR of around 14%, also reaching several hundred million dollars.

The market is also segmented by type: Cloud Based and On Premises. Cloud-based solutions are dominant, accounting for over 80% of the market in 2025 and projected to maintain this lead due to their inherent flexibility and scalability. The market size for cloud-based solutions is estimated to be in the hundreds of millions of dollars, with strong growth projected. On-premises solutions, while still relevant for some specific use cases, represent a smaller and declining segment of the market.

Key Drivers of Automotive Digital Retailing Solutions Growth

The growth of the Automotive Digital Retailing Solutions market is propelled by several critical factors. Firstly, the escalating consumer demand for convenient, transparent, and personalized car buying experiences, akin to other e-commerce sectors, is a primary driver. Secondly, rapid technological advancements, including AI for personalization, VR for virtual showrooms, and advanced analytics for customer insights, are revolutionizing the industry. Thirdly, the increasing adoption of digital payment gateways and online financing solutions simplifies the transaction process. Finally, favorable government initiatives and evolving regulatory frameworks that support digital commerce and data privacy also contribute significantly to market expansion. The shift towards an omni-channel retail approach, seamlessly integrating online and offline touchpoints, is another crucial accelerator.

Challenges in the Automotive Digital Retailing Solutions Sector

Despite the robust growth, the Automotive Digital Retailing Solutions sector faces several challenges. One significant barrier is the perceived complexity of integrating new digital systems with existing legacy dealership infrastructure, leading to potential implementation hurdles. Consumer trust and data security concerns remain paramount, requiring robust cybersecurity measures and transparent data handling policies. Furthermore, the initial investment in advanced digital retailing platforms can be substantial, posing a challenge for smaller dealerships. Regulatory complexities and varying compliance requirements across different regions can also impede widespread adoption. Lastly, the need for continuous training and adaptation of dealership staff to new digital workflows presents an ongoing operational challenge.

Leading Players in the Automotive Digital Retailing Solutions Market

The Automotive Digital Retailing Solutions market is populated by a diverse range of companies, each contributing to the evolving digital landscape. Key players include:

- Upstart Auto Retail

- Driverama

- Cox Automotive

- OTIONE

- Gubagoo

- AnantaTek

- AutoFi

- CarNow

- Keyloop

- Superior Integrated Solutions

- FUSE Autotech

- TotalLoop

- Slashdot (Note: Slashdot is primarily a technology news website, not a direct provider of automotive digital retailing solutions. Its inclusion may be for broader technology ecosystem relevance.)

- Digital Motors Corporation

- Epicor

- Intice

- Market Scan Information Systems

- Modal

- PureCars

Key Developments in Automotive Digital Retailing Solutions Sector

- 2023: Cox Automotive significantly expanded its digital retail offerings with new integrations to streamline the online car buying process, impacting several hundred thousand transactions.

- 2023: AutoFi secured significant funding to further develop its end-to-end digital financing platform, aiming to process millions in loan applications annually.

- 2022: Gubagoo launched new AI-powered conversational tools, enhancing lead generation and customer engagement for dealerships, leading to an estimated 20% increase in conversion rates for early adopters.

- 2022: Digital Motors Corporation partnered with several major automotive groups to implement its comprehensive digital retailing suite, impacting thousands of dealerships and millions of potential customers.

- 2021: CarNow integrated its virtual retail solutions with leading inventory management systems, processing millions of online customer interactions.

- 2020: Upstart Auto Retail introduced enhanced virtual showroom capabilities, allowing dealerships to showcase their inventory to millions of online browsers.

- 2019: The foundational shift towards cloud-based solutions began to accelerate, with many providers reporting a substantial increase in subscription-based revenue, reaching several hundred million dollars globally.

Strategic Automotive Digital Retailing Solutions Market Outlook

The strategic outlook for the Automotive Digital Retailing Solutions market is exceptionally positive, fueled by ongoing digital transformation initiatives and evolving consumer behaviors. The continued development and integration of AI, VR, and data analytics will unlock new avenues for personalization and operational efficiency, potentially impacting billions in revenue. Strategic opportunities lie in forging deeper partnerships between technology providers and traditional automotive stakeholders to create seamless, customer-centric ecosystems. Focus on enhancing the post-purchase digital experience, including service scheduling and ownership management, will also be a key growth accelerator. The market is poised for sustained expansion, with companies that prioritize user experience, data security, and flexible, scalable solutions set to capture significant market share and drive industry innovation. The projected growth trajectory suggests a market that will continue to evolve and redefine automotive sales for millions of consumers worldwide.

Automotive Digital Retailing Solutions Segmentation

-

1. Application

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. Types

- 2.1. Cloud Based

- 2.2. On Premises

Automotive Digital Retailing Solutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Digital Retailing Solutions Regional Market Share

Geographic Coverage of Automotive Digital Retailing Solutions

Automotive Digital Retailing Solutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud Based

- 5.2.2. On Premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud Based

- 6.2.2. On Premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud Based

- 7.2.2. On Premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud Based

- 8.2.2. On Premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud Based

- 9.2.2. On Premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Digital Retailing Solutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud Based

- 10.2.2. On Premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Upstart Auto Retail

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Driverama

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cox Automotive

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 OTIONE

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Gubagoo

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AnantaTek

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AutoFi

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CarNow

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Keyloop

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Superior Integrated Solutions

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 FUSE Autotech

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 TotalLoop

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Slashdot

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Digital Motors Corporation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Epicor

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Intice

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Market Scan Information Systems

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Modal

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 PureCars

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 Upstart Auto Retail

List of Figures

- Figure 1: Global Automotive Digital Retailing Solutions Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Digital Retailing Solutions Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Digital Retailing Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Digital Retailing Solutions Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive Digital Retailing Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Digital Retailing Solutions Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Digital Retailing Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Digital Retailing Solutions Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Digital Retailing Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Digital Retailing Solutions Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive Digital Retailing Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Digital Retailing Solutions Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Digital Retailing Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Digital Retailing Solutions Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Digital Retailing Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Digital Retailing Solutions Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive Digital Retailing Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Digital Retailing Solutions Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Digital Retailing Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Digital Retailing Solutions Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Digital Retailing Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Digital Retailing Solutions Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Digital Retailing Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Digital Retailing Solutions Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Digital Retailing Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Digital Retailing Solutions Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Digital Retailing Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Digital Retailing Solutions Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Digital Retailing Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Digital Retailing Solutions Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Digital Retailing Solutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Digital Retailing Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Digital Retailing Solutions Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Digital Retailing Solutions?

The projected CAGR is approximately 7.4%.

2. Which companies are prominent players in the Automotive Digital Retailing Solutions?

Key companies in the market include Upstart Auto Retail, Driverama, Cox Automotive, OTIONE, Gubagoo, AnantaTek, AutoFi, CarNow, Keyloop, Superior Integrated Solutions, FUSE Autotech, TotalLoop, Slashdot, Digital Motors Corporation, Epicor, Intice, Market Scan Information Systems, Modal, PureCars.

3. What are the main segments of the Automotive Digital Retailing Solutions?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 714.43 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Digital Retailing Solutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Digital Retailing Solutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Digital Retailing Solutions?

To stay informed about further developments, trends, and reports in the Automotive Digital Retailing Solutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence