Key Insights

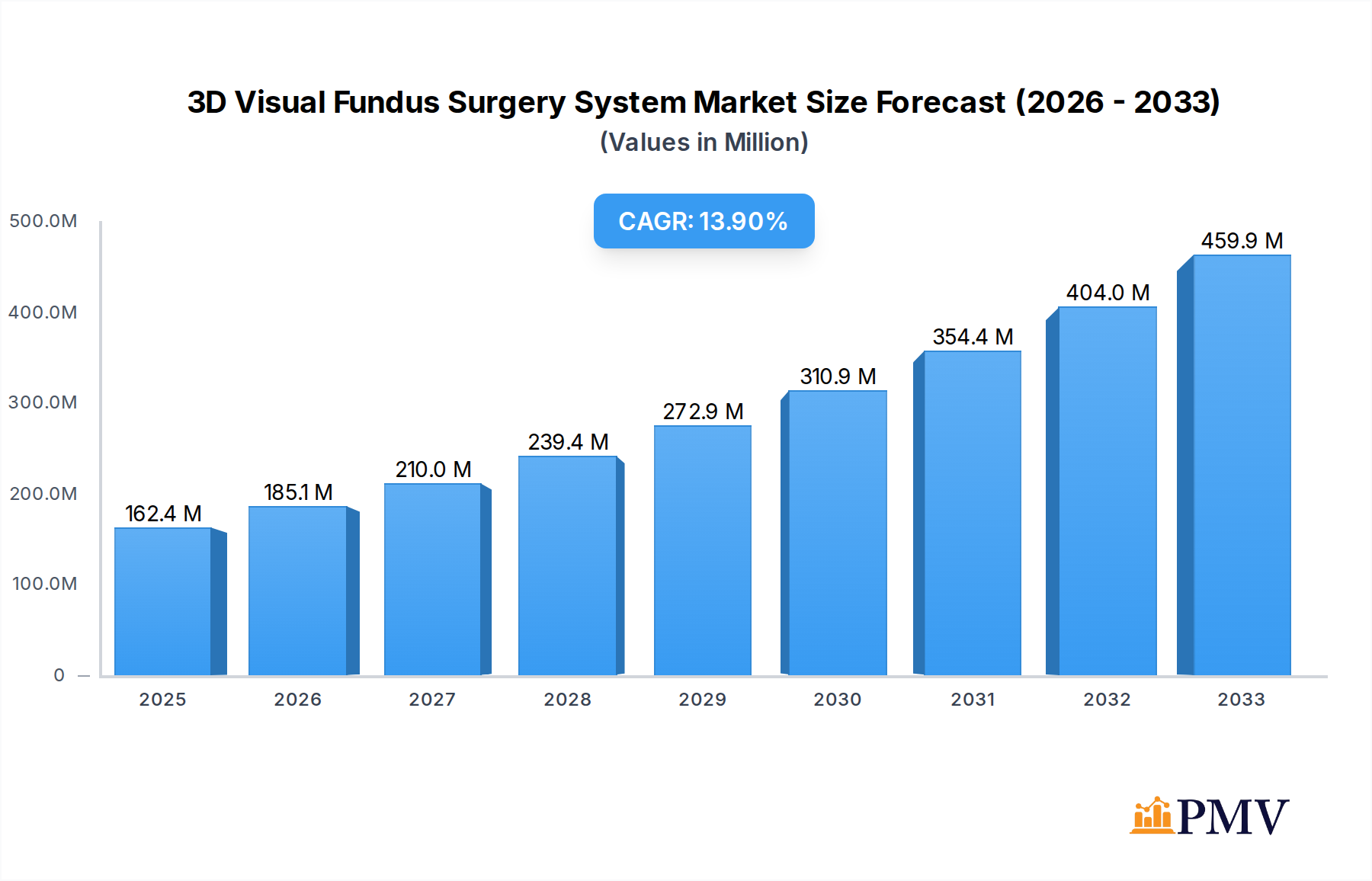

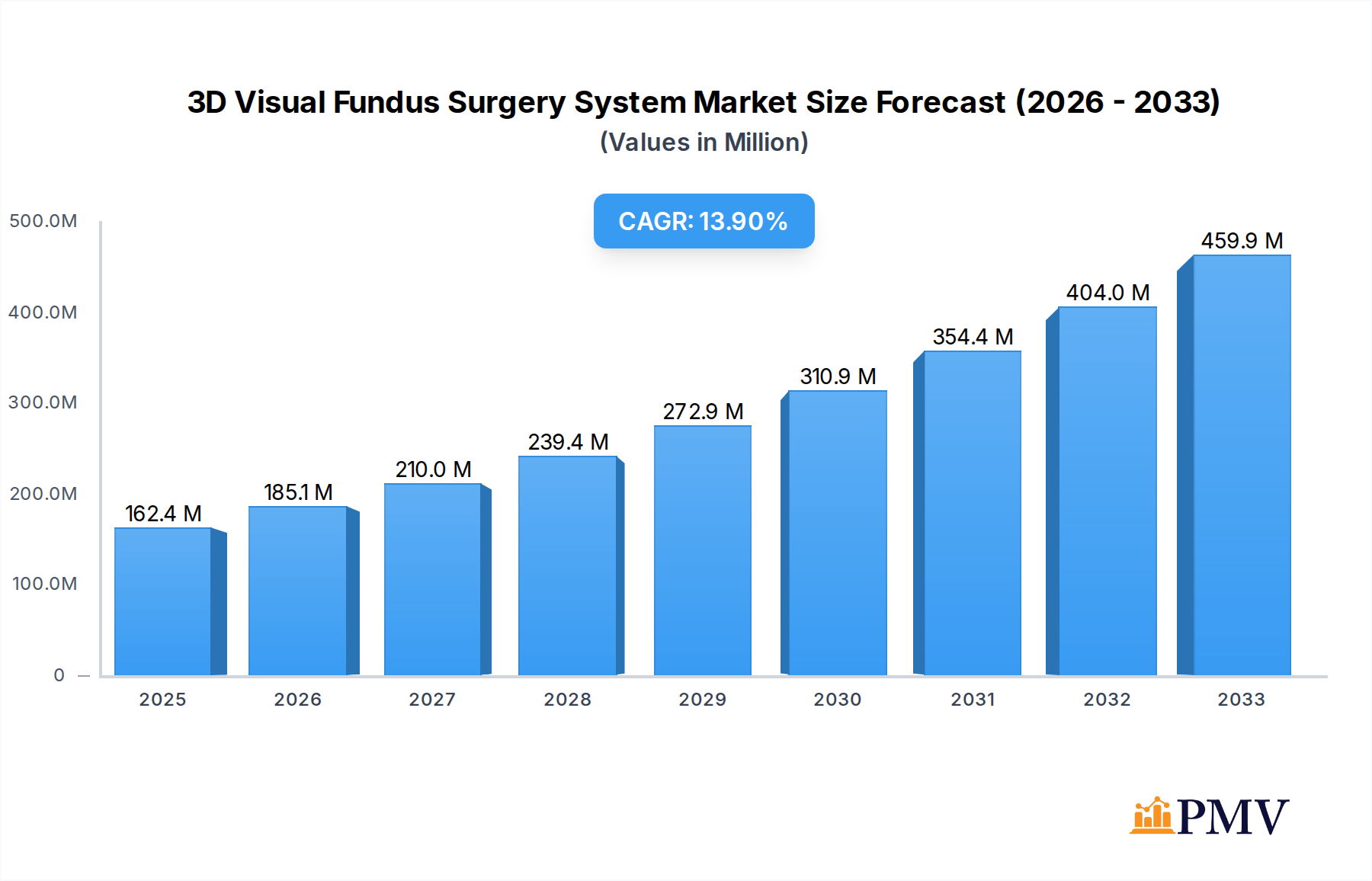

The global 3D Visual Fundus Surgery System market is poised for substantial expansion, reaching an estimated $162.4 million by 2025. This growth is propelled by a compelling CAGR of 14% over the forecast period (2025-2033), indicating robust demand for advanced ophthalmic surgical solutions. The increasing prevalence of eye diseases, coupled with a rising global geriatric population, are significant drivers fueling this market trajectory. Furthermore, technological advancements in visualization, imaging, and surgical robotics are enhancing the precision and efficacy of fundus surgeries, making these systems increasingly indispensable in hospital and clinic settings. The shift towards minimally invasive procedures and the growing adoption of advanced medical devices in ophthalmology are also contributing to this optimistic outlook.

3D Visual Fundus Surgery System Market Size (In Million)

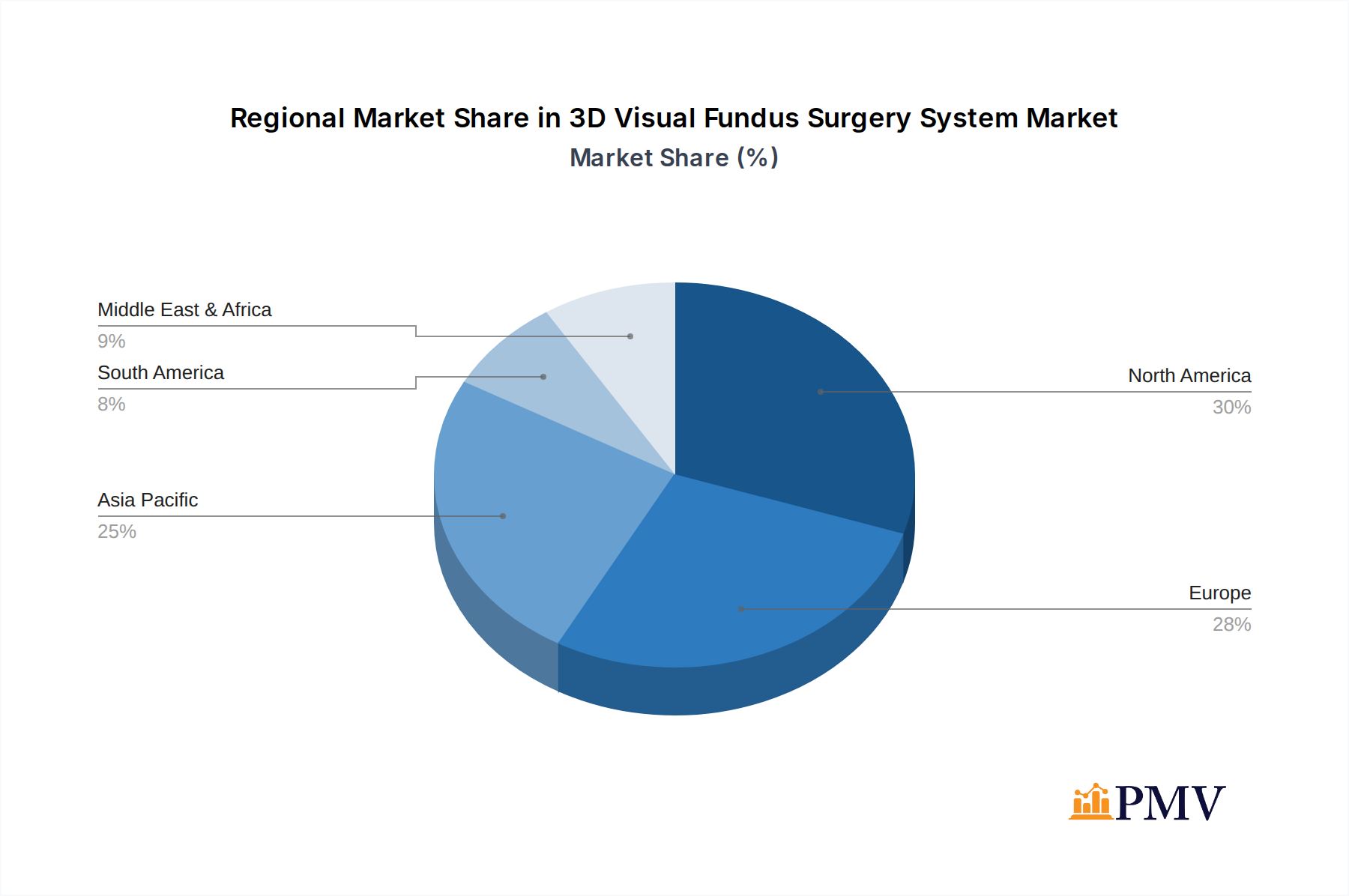

The market is segmented by application into Hospitals, Clinics, and Others, with Hospitals likely dominating due to the comprehensive infrastructure and higher patient volumes they accommodate. By type, the market encompasses Manual, Semi-Automatic, and Fully Automatic systems, with a clear trend towards the adoption of fully automatic solutions owing to their enhanced precision, reduced surgeon fatigue, and improved patient outcomes. Key players like Alcon, Medtronic, GE, Nanjing Tianao Medical Instrument Manufacturing, and Beijing Zhilin Yicheng Technology are actively innovating and expanding their product portfolios to capture a significant share of this burgeoning market. Regional analysis indicates a strong presence in North America and Europe, with significant growth potential anticipated in the Asia Pacific region, driven by increasing healthcare expenditure and a growing awareness of advanced ophthalmic treatments.

3D Visual Fundus Surgery System Company Market Share

Here is the SEO-optimized, detailed report description for the 3D Visual Fundus Surgery System Market:

3D Visual Fundus Surgery System Market Structure & Competitive Dynamics

The 3D Visual Fundus Surgery System market is characterized by a moderate to high level of concentration, with key players like Alcon, Medtronic, and emerging innovators from China such as Nanjing Tianao Medical Instrument Manufacturing and Beijing Zhilin Yicheng Technology holding significant influence. The innovation ecosystem thrives on advancements in surgical visualization, miniaturization, and artificial intelligence integration, driving a competitive landscape where early adopters and those with strong R&D capabilities gain market share. Regulatory frameworks, while essential for patient safety, can present hurdles for new market entrants but also create barriers to entry that benefit established players. Product substitutes, though not directly equivalent, include traditional fundus cameras and less immersive 3D visualization systems, influencing adoption rates. End-user trends indicate a growing demand for minimally invasive procedures and enhanced surgical precision, pushing the adoption of sophisticated 3D systems. Mergers and acquisitions (M&A) are anticipated to play a role in market consolidation, with potential deal values in the tens to hundreds of millions. For instance, strategic acquisitions of smaller technology firms by larger medical device manufacturers can rapidly expand product portfolios and market reach, influencing overall market share dynamics estimated at over $2,000 million in the base year.

3D Visual Fundus Surgery System Industry Trends & Insights

The 3D Visual Fundus Surgery System industry is poised for robust growth, driven by an escalating global prevalence of ophthalmic diseases and a corresponding surge in demand for advanced surgical solutions. The market penetration of these sophisticated systems is steadily increasing as healthcare providers recognize their inherent benefits: enhanced visualization, improved surgical accuracy, reduced patient trauma, and shorter recovery times. Technological disruptions are at the forefront of this evolution, with significant investments in AI-powered image analysis, real-time intraoperative guidance, and the integration of augmented reality overlays. These innovations are not merely incremental improvements but are fundamentally reshaping the surgical workflow, enabling surgeons to perform more complex procedures with greater confidence and precision. The compound annual growth rate (CAGR) for the 3D Visual Fundus Surgery System market is projected to be between 10% and 15% over the forecast period of 2025–2033, reflecting a strong upward trajectory.

Consumer preferences, primarily driven by medical professionals and hospital administrators, are increasingly leaning towards systems that offer superior ergonomics, intuitive user interfaces, and seamless integration with existing hospital IT infrastructure. The competitive dynamics are intensifying, with established global players like Alcon and Medtronic leveraging their extensive market presence and R&D capabilities. Simultaneously, innovative Chinese manufacturers, including Nanjing Tianao Medical Instrument Manufacturing and Beijing Zhilin Yicheng Technology, are rapidly gaining traction by offering cost-effective yet technologically advanced solutions, disrupting traditional market hierarchies.

The market is witnessing a trend towards greater adoption in both established and emerging economies. In developed nations, the focus is on upgrading existing surgical suites with cutting-edge 3D visualization technology to maintain a competitive edge and improve patient outcomes. In developing regions, the introduction of these systems, often through strategic partnerships and government initiatives, is crucial for expanding access to advanced ophthalmic care. The market size in the base year of 2025 is estimated to be over $2,000 million, with projections indicating it could exceed $5,000 million by 2033. The ongoing research into remote surgical training and telementoring using 3D fundus surgery systems further underscores the industry's commitment to innovation and accessibility.

Dominant Markets & Segments in 3D Visual Fundus Surgery System

The 3D Visual Fundus Surgery System market exhibits distinct regional dominance and segment leadership, driven by a confluence of economic policies, healthcare infrastructure development, and the prevalence of ophthalmic conditions. North America and Europe currently represent the leading geographical markets, owing to high healthcare spending, advanced technological adoption rates, and a robust regulatory framework that encourages innovation and patient safety. The United States, in particular, stands out as a dominant country within these regions, supported by a vast network of specialized eye clinics and hospitals equipped with cutting-edge medical technology.

Within the Application segment, Hospitals emerge as the dominant end-user. This is attributed to several key drivers:

- Higher Volume of Complex Procedures: Hospitals typically handle a greater volume and complexity of ophthalmic surgeries, including retinal detachments, macular degeneration treatments, and complex cataract surgeries, which benefit most from 3D visualization.

- Investment Capacity: Hospitals, particularly large medical centers, possess the financial resources and infrastructure to invest in high-cost, advanced surgical equipment like 3D Visual Fundus Surgery Systems.

- Integrated Surgical Suites: The trend towards integrated surgical suites in hospitals facilitates the seamless incorporation of advanced visualization technologies.

- Research and Training Hubs: Hospitals often serve as centers for ophthalmic research and surgical training, further accelerating the adoption of innovative technologies.

In the Types segment, the Fully Automatic systems are rapidly gaining prominence, though Semi-Automatic systems currently hold a significant market share. The dominance of fully automatic systems is driven by:

- Enhanced Efficiency and Precision: Fully automatic systems offer unparalleled precision and reduced surgical time by automating critical aspects of the surgical procedure, minimizing the potential for human error.

- Advanced AI Integration: The integration of artificial intelligence algorithms in fully automatic systems allows for predictive analytics and real-time adjustments, leading to superior surgical outcomes.

- Cost-Effectiveness in the Long Run: While initial investment may be higher, the long-term benefits of increased efficiency, reduced complications, and faster patient recovery can make fully automatic systems more cost-effective.

- Surgeon Preference for Simplicity: As these systems become more sophisticated, they often offer simplified user interfaces, reducing the learning curve and allowing surgeons to focus on the critical aspects of the procedure.

Emerging economies, particularly in Asia-Pacific, are showing substantial growth potential, driven by increasing healthcare investments, a growing middle class with greater access to healthcare, and a rising burden of ophthalmic diseases. Countries like China and India are becoming significant markets, fueled by both domestic manufacturing capabilities and a rising demand for advanced medical devices. Economic policies that support medical device import and local manufacturing, coupled with significant investments in healthcare infrastructure, are key accelerators in these regions. The market size within these dominant segments is substantial, with hospitals accounting for over 80% of the total revenue from the application perspective. Fully automatic systems, while still an evolving segment, are projected to capture over 60% of the market share by 2033 due to their superior capabilities and increasing affordability.

3D Visual Fundus Surgery System Product Innovations

Recent product innovations in the 3D Visual Fundus Surgery System market are centered around enhancing surgical precision, improving visualization clarity, and integrating intelligent guidance systems. Companies are focusing on developing lighter, more maneuverable surgical instruments and higher-resolution 3D displays that offer unparalleled depth perception. Key advancements include AI-powered surgical analytics for real-time feedback, automated instrument tracking, and augmented reality overlays that project critical patient data directly into the surgeon's field of view. These innovations provide a distinct competitive advantage by enabling surgeons to perform more complex procedures with greater confidence and a reduced risk of complications, ultimately leading to better patient outcomes and shorter recovery periods.

Report Segmentation & Scope

This report provides a comprehensive analysis of the 3D Visual Fundus Surgery System market, segmented across key application and type categories.

Application: The market is segmented into Hospital, Clinic, and Others. The Hospital segment, projected to account for over $4,000 million by 2033, is the largest due to higher procedure volumes and investment capacity. Clinics are showing steady growth, driven by specialized ophthalmic practices, with market sizes estimated to reach over $800 million by 2033. The 'Others' segment, encompassing research institutions and specialized surgical centers, is projected to grow at a CAGR of xx%, reaching approximately $200 million.

Types: The market is further divided into Manual, Semi-Automatic, and Fully Automatic systems. The Fully Automatic segment is the fastest-growing, with projections exceeding $3,000 million by 2033, driven by advanced automation and AI integration. Semi-Automatic systems, currently holding a substantial market share estimated at over $1,500 million, will continue to be a significant part of the market. Manual systems, while representing the smallest segment, are expected to maintain a niche market, with projected revenues of around $100 million by 2033. The scope includes market size, growth projections, competitive landscape, and key trends for each of these segments.

Key Drivers of 3D Visual Fundus Surgery System Growth

The growth of the 3D Visual Fundus Surgery System market is propelled by several interconnected factors. Technologically, advancements in surgical robotics, high-definition imaging, and artificial intelligence are making these systems more precise, intuitive, and capable of handling complex procedures. Economically, increasing global healthcare expenditures, coupled with a rising disposable income in emerging economies, are expanding access to advanced medical technologies. Regulatory bodies are also playing a role by establishing clear guidelines for the approval of innovative ophthalmic surgical devices, fostering a conducive environment for market expansion. Furthermore, the increasing prevalence of age-related macular degeneration, diabetic retinopathy, and other vision-impairing conditions globally necessitates more sophisticated and minimally invasive surgical interventions, directly driving demand for 3D fundus surgery systems.

Challenges in the 3D Visual Fundus Surgery System Sector

Despite its promising growth, the 3D Visual Fundus Surgery System sector faces several challenges. High initial acquisition costs for advanced 3D systems can be a significant barrier for smaller clinics and healthcare facilities, particularly in price-sensitive markets. Regulatory hurdles for market approval of new technologies can lead to prolonged development cycles and increased expenses. Supply chain disruptions, as evidenced in recent global events, can impact the availability of critical components and increase manufacturing costs. Furthermore, a shortage of skilled ophthalmic surgeons trained to operate these sophisticated systems can limit widespread adoption. Intense competition from established players and the emergence of new entrants also exerts pressure on pricing and profit margins, with potential impacts on market growth rates estimated to slow down by xx% in case of severe disruptions.

Leading Players in the 3D Visual Fundus Surgery System Market

- Alcon

- Medtronic

- GE

- Nanjing Tianao Medical Instrument Manufacturing

- Beijing Zhilin Yicheng Technology

Key Developments in 3D Visual Fundus Surgery System Sector

- 2023/07: Alcon launches its next-generation 3D visualization system for cataract surgery, featuring enhanced optical clarity and integrated AI analytics, boosting its market share by an estimated 3% in the quarter.

- 2023/10: Medtronic announces strategic partnership with a leading AI research firm to integrate advanced predictive algorithms into its fundus surgery platforms, aiming to reduce surgical complications by 5%.

- 2024/01: Nanjing Tianao Medical Instrument Manufacturing unveils a new cost-effective 3D fundus surgery system targeted at emerging markets, projecting a significant increase in unit sales by xx million in the first year.

- 2024/03: Beijing Zhilin Yicheng Technology receives FDA clearance for its innovative robotic-assisted fundus surgery system, expanding its operational scope and competitive positioning.

- 2024/05: GE announces a significant investment of $50 million in R&D for advanced surgical imaging technologies, including 3D visualization, aiming to capture a larger segment of the market by 2028.

Strategic 3D Visual Fundus Surgery System Market Outlook

The strategic outlook for the 3D Visual Fundus Surgery System market is exceptionally positive, driven by sustained technological innovation and a growing global demand for advanced ophthalmic care. Key growth accelerators include the increasing integration of artificial intelligence for enhanced surgical precision and workflow optimization, the development of more compact and affordable systems to broaden market access, and strategic partnerships between established medical device giants and agile technology startups. Furthermore, the expanding healthcare infrastructure in emerging economies presents a substantial opportunity for market penetration. The continued focus on minimally invasive techniques and the drive to improve patient outcomes will ensure a robust demand for these sophisticated visualization solutions, positioning the market for continued expansion and value creation, with an estimated market growth of over $3,000 million in revenue by 2033.

3D Visual Fundus Surgery System Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Others

-

2. Types

- 2.1. Manual

- 2.2. Semi-Automatic

- 2.3. Fully Automatic

3D Visual Fundus Surgery System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

3D Visual Fundus Surgery System Regional Market Share

Geographic Coverage of 3D Visual Fundus Surgery System

3D Visual Fundus Surgery System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Manual

- 5.2.2. Semi-Automatic

- 5.2.3. Fully Automatic

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Manual

- 6.2.2. Semi-Automatic

- 6.2.3. Fully Automatic

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Manual

- 7.2.2. Semi-Automatic

- 7.2.3. Fully Automatic

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Manual

- 8.2.2. Semi-Automatic

- 8.2.3. Fully Automatic

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Manual

- 9.2.2. Semi-Automatic

- 9.2.3. Fully Automatic

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific 3D Visual Fundus Surgery System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Manual

- 10.2.2. Semi-Automatic

- 10.2.3. Fully Automatic

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Alcon

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Medtronic

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 GE

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nanjing Tianao Medical Instrument Manufacturing

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Beijing Zhilin Yicheng Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.1 Alcon

List of Figures

- Figure 1: Global 3D Visual Fundus Surgery System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America 3D Visual Fundus Surgery System Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America 3D Visual Fundus Surgery System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America 3D Visual Fundus Surgery System Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America 3D Visual Fundus Surgery System Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America 3D Visual Fundus Surgery System Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America 3D Visual Fundus Surgery System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America 3D Visual Fundus Surgery System Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America 3D Visual Fundus Surgery System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America 3D Visual Fundus Surgery System Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America 3D Visual Fundus Surgery System Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America 3D Visual Fundus Surgery System Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America 3D Visual Fundus Surgery System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe 3D Visual Fundus Surgery System Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe 3D Visual Fundus Surgery System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe 3D Visual Fundus Surgery System Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe 3D Visual Fundus Surgery System Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe 3D Visual Fundus Surgery System Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe 3D Visual Fundus Surgery System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa 3D Visual Fundus Surgery System Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa 3D Visual Fundus Surgery System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa 3D Visual Fundus Surgery System Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa 3D Visual Fundus Surgery System Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa 3D Visual Fundus Surgery System Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa 3D Visual Fundus Surgery System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific 3D Visual Fundus Surgery System Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific 3D Visual Fundus Surgery System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific 3D Visual Fundus Surgery System Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific 3D Visual Fundus Surgery System Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific 3D Visual Fundus Surgery System Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific 3D Visual Fundus Surgery System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global 3D Visual Fundus Surgery System Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific 3D Visual Fundus Surgery System Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Visual Fundus Surgery System?

The projected CAGR is approximately 14%.

2. Which companies are prominent players in the 3D Visual Fundus Surgery System?

Key companies in the market include Alcon, Medtronic, GE, Nanjing Tianao Medical Instrument Manufacturing, Beijing Zhilin Yicheng Technology.

3. What are the main segments of the 3D Visual Fundus Surgery System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3D Visual Fundus Surgery System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3D Visual Fundus Surgery System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3D Visual Fundus Surgery System?

To stay informed about further developments, trends, and reports in the 3D Visual Fundus Surgery System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence